Image © Adobe Images

The Pound could be set for further losses against the Australian Dollar, although Thursday's Bank of England decision could prove supportive.

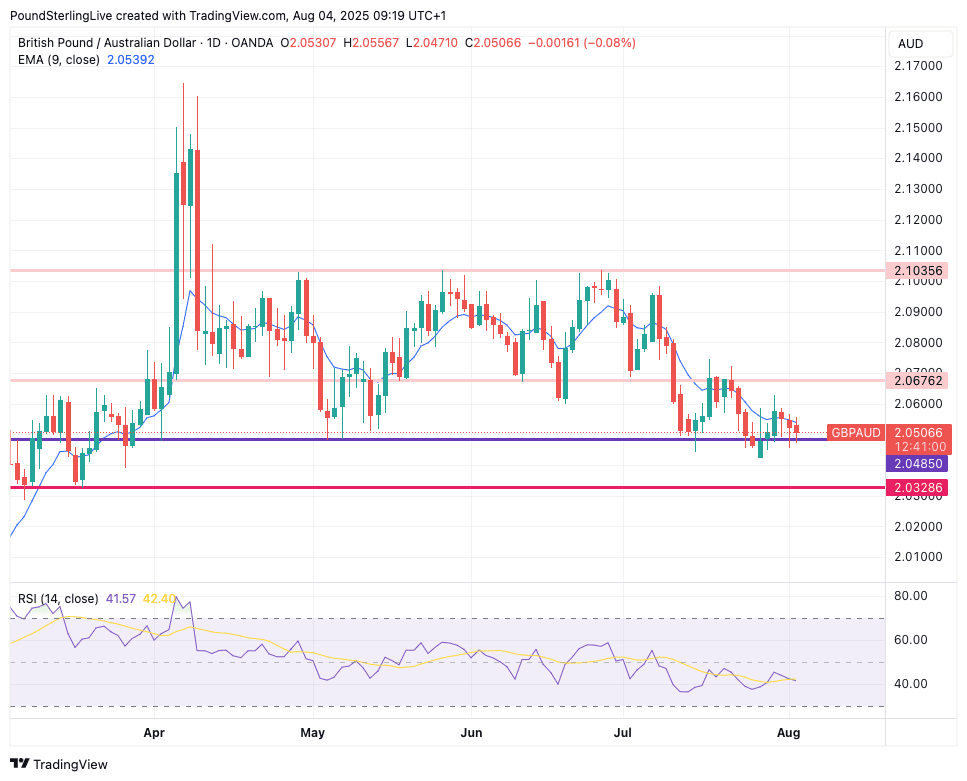

The Pound to Australian Dollar exchange rate (GBP/AUD) remains in a short-term downtrend, even if progress lower has been decidedly slow and disjointed.

Interestingly, we would have expected GBP/AUD to have shot higher following the negative market reaction to Friday's soft U.S. jobs report. Yet, it actually ended the day 0.14% lower.

That the Australian Dollar rose amidst a spike in global market volatility is certainly a bullish development for a currency that tends to slump under such scenarios. Currency strategists are taking note of a broad set of Aussie positives, including a robust domestic economy, and we recently reported that the team at Deutsche Bank think the AUD can extend a period of outperformance.

This all leaves GBP/AUD looking precariously balanced on the horizontal support line at 2.0485: note that the pair often finds buying interest here and that has the effect of frustrating meaningful AUD rallies. This frustration could yet continue to underpin GBP/AUD.

That being said, GBP/AUD is still capped by a downward sloping nine-day exponential moving average (EMA), a momentum line that is the benchmark of our Week Ahead Forecast models here at Pound Sterling Live.

The rule is that when below the nine-day EMA, a pair is in a short-term downtrend. For GBP/AUD to solidify support at the 2.0485 support, it must climb back above the nine-day.

Above: GBP/AUD at daily intervals.

Failure to climb above the line will dunk GBP/AUD below 2.0485 and allow for a test of 2.0426, last week's low, ahead of a move to 2.0328, May's lows.

The calendar event to watch this week involves the Bank of England, where an interest rate cut of 25 basis points is to be expected.

With the rate cut 'in the price' of GBP/AUD, the directional signal will have to come from the guidance pertaining to future moves. Does the Bank see the deterioration in the jobs market, and its associated slowing wage pressures, as reason enough to signal further hikes?

Or does it remember its mandate is to bring inflation back to 2.0%, and therefore a more cautious approach is warranted?

The arguments in favour of both are strong and it would not be unreasonable to think either side wins out. However, we think this seemingly contradictory economic fundamentals will simply translate into another divided Monetary Policy Committee vote, which should ensure the status quo remains intact.

As a reminder, that status quo is the preference to maintain a quarterly pace to the cutting cycle, while retaining an ambiguous guidance whereby the Bank says risks to inflation lie to the upside and downside and that it will continue to monitor the data.

Given the scope of the GBP's recent decline we would imagine that the market is already relatively pitted against Sterling, meaning that it will take a noticebly 'dovish' policy event to trigger fresh lows. Given this, the risks are skewed to the upside if cautious guidelines are issue.

"We have a hawkish Bank Rate forecast, expecting August to see the final cut this year, and the last cut until after 2027," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.