Image © Adobe Images

The Pound is forecast to deflate further against the Australian Dollar this week.

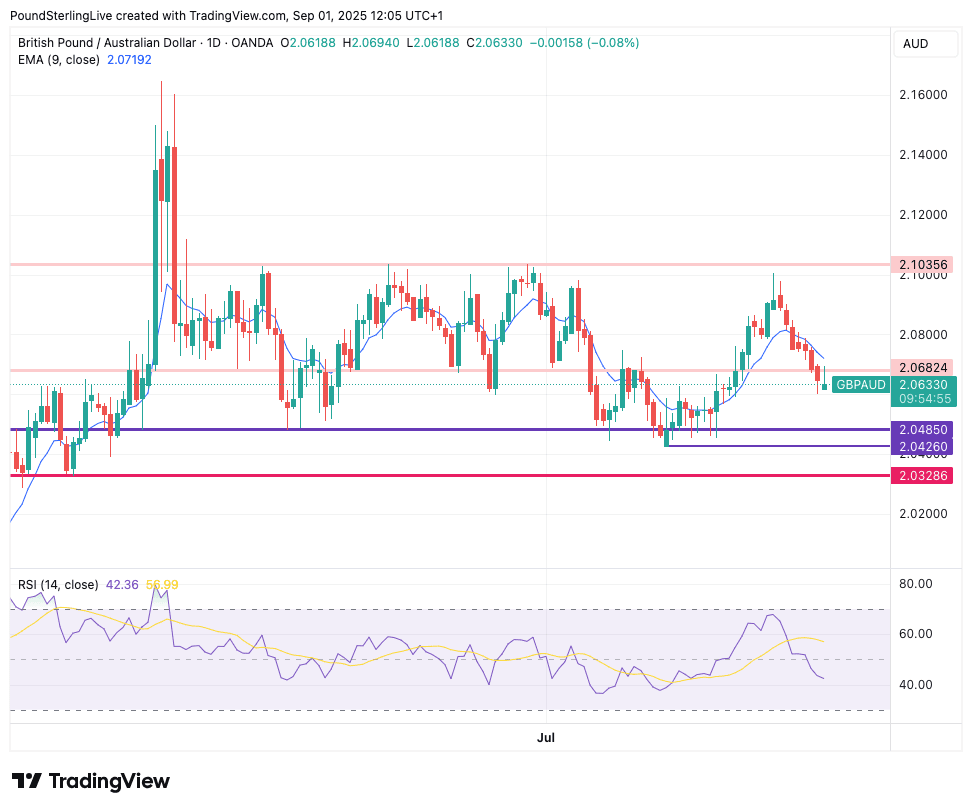

The Aussie Dollar has advanced against the British Pound for seven successive days now, speaking of a building momentum that pushes GBP/AUD to 2.0630 at the start of the new month.

Technical studies confirm the Pound to Australian Dollar exchange rate (GBP/AUD) has entered a period of depreciation, and a test of 2.0485 is coming into view in the short term.

The exchange rate is locked below the nine-day exponential moving average (EMA), located at 2.0718, which advocates for further declines short-term.

Momentum, as per the Relative Strength Indicator (RSI), backs this view, with a reading of 40 and its nose pointing lower.

The first target is 2.0485 which forms the bottom of the April-July range. However, below here is firmer support at 2.0426, which was the range's floor through much of August:

For now, we anticipate this area to offer a solid source of support as there is little by way of news on the fundamental front to provide the succour to drive a genuine downtrend in GBP/AUD.

For this to happen we suspect the Chinese economy will need to put in a bout of genuine outperformance, as we note that the AUD's most notable periods of outperformance are tied to the fortunes of China.

With this unlikely to happen due to the transitions underway in China, AUD gains should ultimately have limits.

Nevertheless, the British Pound is hardly an inspiring 'buy' and it can test lower levels against the Aussie as investors fret over the UK's poor debt dynamics and the prospect of swinging tax rises in November.

Enrique Diaz-Alvarez, Chief Economist at Ebury, says action in the gilt market, where long-dated rates continue to rise relentlessly, is a worry that can keep GBP under pressure.

"This is of course a general trend in sovereign debt markets, but British yields remain the highest in the G10," says Diaz-Alvarez.

UK ten-year bond yields have risen to 4.74%, which is at the top of a ceiling that has been in place since 2023, and the risk is that they shift gear into a new higher range in the coming months, which would put tremendous pressure on the UK's public finances.

The 30-year yield is also knocking on the door of fresh highs, at 5.635%.

"Labour's inability to control spending amid persistent unpleasant surprises in the inflation numbers certainly do not help. Markets are currently pricing in less than a 50% chance of even a single rate cut this year from the Bank of England, but the steady rise in medium and long term rates threaten to render policy moves less effective regardless," says Diaz-Alvarez.

The UK budget looms as the main concern for UK-focussed assets, with the November event likely to see a wave of new taxes being placed on a country that already suffers under the highest tax burden since the Second World War.

Uncertainty ahead of the announcement will keep businesses and households on the defensive, constraining the economy and troubling the Pound.

Turning to the near-term focus, watch Bank of England Governor Andrew Bailey's testimony before UK lawmakers midweek, where he should shine some more light on the prospects of further interest rate cuts this year.

The main data event of the week will be Friday's release of retail sales figures.