Image © Adobe Stock

We're watching the RBA decision, UK political risks and U.S. payrolls this week.

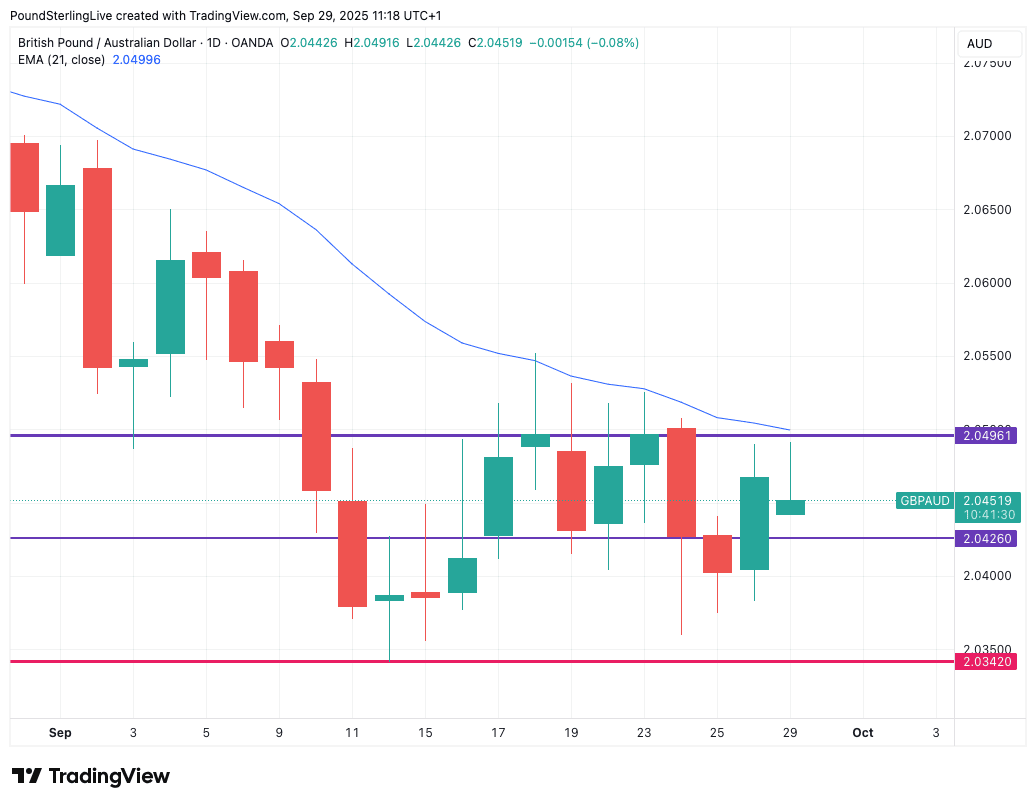

The pound to Australian dollar exchange rate (GBP/AUD) remtains a consolidative tone ahead of a what could be an interesting week for the exchange rate.

As the chart shows, GBP/AUD has been consolidating in a relatively tight range since September 10, and this should provide a decent guide as to how the pair should behave into Tuesday's Reserve Bank of Australia (RBA) decision:

As can be seen, the range is defined by 2.0496 at the top and 2.0342 at the bottom, but it's the middle of the range ~2.0426 that has the major gravitational pull.

We would anticipate further gyrations around this level near-term, unless either GBP or AUD are catapulted by some kind of event risk.

Event risks in the UK are relatively elevated heading into this week's Labour Party conference, where calls for more spendthrift policies and higher borrowing will be made.

Be under no doubt, Chancellor Rachel Reeves is under pressure to boost borrowing, and this risks a messy response from bond markets and a repeat of the Liz Truss bond and pound selloff of 2022.

As always with this type of headline-driven risk, the timing is difficult to gauge, and the best advice we can offer readers is that they should just keep this major GBP-negative risk in mind.

Turning to AUD, the Reserve Bank of Australia (RBA) is set to leave interest rates unchanged on Tuesday, but currency markets will be interested in guidance regarding the potential for a cut in November.

The Aussie has shown itself quite responsive to domestic economic developments of late, given it will have a steer on what the RBA does going forward.

It signals that the AUD is responsive to RBA expectations, ensuring Tuesday's decision can have a bearing on near-term trade.

Should the RBA do enough to encourage the market to raise bets for a November rate cut, then AUD can come under pressure. If it pushes back against these odds, then AUD can strengthen.

The odds of a November rate cut were reduced last week after Australia's monthly measure of inflation rose to 3.0% year-on-year in August, which was stronger than the expected 2.9% and a step higher than the previous month's reading of 2.8%.

However, just a week before, employment data surprised to the downside, raising the odds of RBA cuts and weighing on the currency.

This signals there are enough cross-currents to keep Tuesday's decision interesting and this can elicit a currency reaction.

"The RBA is unlikely to rush into rate cuts, but nor will it keep policy tighter than necessary for too long. Hence, we continue to expect the RBA to remain on hold next week, with cuts to follow in November," says a note from Westpac Bank.

However, it will likely be the U.S. labour market report, due at the end of the week, that will have the greater bearing on AUD direction.

A soft reading would bolster the case for further rate cuts at the Federal Reserve, which will weigh on the dollar and allow pro-risk currencies like the Australian Dollar to appreciate.

The market looks for approximately 55K jobs to have been added in September, meaning this is the bar that must be crossed.

Beware, though: U.S. data has been coming in at above-consensus levels over the past month, signalling the economy risks performing better than anyone is expecting going into year-end.

It raises the odds of Friday's non-farm payrolls report beating expectations and lifting the dollar, at the expense of AUD exchange rates.