Image © Adobe Images

The Australian Dollar's interest rate tailwinds are set to fade, which should alleviate downside pressures on GBP/AUD.

Following the release of May's inflation data, economists at a number of institutions we follow say the Reserve Bank of Australia (RBA) is all but set to raise interest rates again in early August, the fourth hike of the year.

For the AUD, the succession of rate hikes has helped drive outperformance, and the H1 performance board saw AUD as the G10's second-best performer.

But, the tide could turn on AUD outperformance if there's a conviction that the next hike is the last of the cycle.

And that's important because it will prompt traders to cast their minds to the future and consider what comes next: Money market pricing shows investors are looking for the next RBA to potentially lead the cutting cycle.

So, for AUD, a narrative could emerge that cuts will be needed to reverse the effects of the hikes.

That's a potential headwind for the currency that would underscore the view that GBP/AUD has bottomed as the AUD's powerful rates tailwind narrative is complete.

What Inflation Tells us

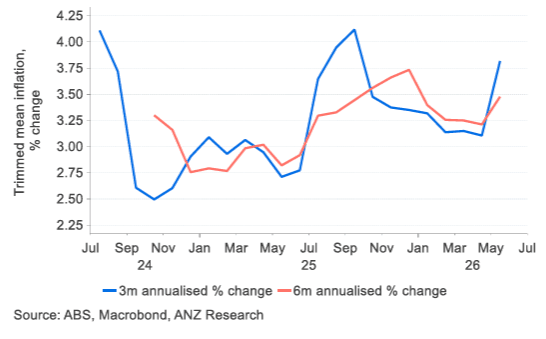

Wednesday's inflation print could be the final piece of the puzzle that prompts the RBA to raise interest rates again: Australia's headline CPI decreased 0.7% m/m in May, with year-over-year growth decelerating 20bp to be 4.0% y/y, weaker-than-expected.

However, despite the decrease in headline inflation, trimmed mean inflation (the RBA's preferred measure) rose 0.4% m/m, according to the ABS.

What's more, year-over-year growth accelerating 20bp to 3.6%, stronger-than-expected.

And looking ahead to jobs data tomorrow, markets look for employment to rebound 40k following a weak outcome in April, underscoring the view that the economy remains as robust as ever.

RBA to Hike Again

These data, and particularly the trimmed mean reading, can't be ignored by the RBA, which opted to skip a hike in its most recent meeting.

"The May data reinforce the RBA’s concern that inflation remains too high and that a period of slower growth will be needed to return inflation to target," says Neha Sharma, Economist at Westpac.

The inflation numbers are contextualised by the RBA's most recent guidance that made it clear that it was prepared to increase the cash rate further "if required".

"Governor Bullock repeated this point in the media conference. That looked deliberate, and suggests the Board wanted to push back against speculation that it is done hiking," says Sharma.

"On the RBA, after Bullock's hawkish hold in June, stating that 'inflation is still too high' and that her decision 'does not rule out further tightening' we continue to lean towards another 25bp rate hike at the August meeting," says Goldman Sachs.

But That Hike Would be the Last

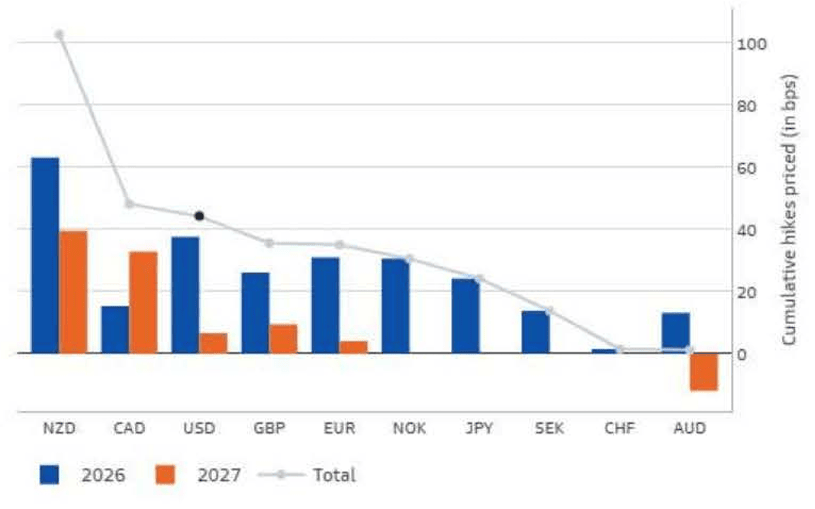

With the market looking for one more hike in the cycle (if not August, then on the occasion of the next meeting in September), there's enough latent interest rate support floating about to keep AUD supported.

However, the money markets also show there's a building expectation that the RBA will be cutting rates relatively early in 2027:

In fact, the RBA could lead the cutting charge, signalling that markets think that the effect of recent rate hikes will require some reversal in policy direction to reboot demand.

AUD could sing from the most hawkish currency candidate in the pack to the most dovish.

For AUD, that poses the prospect of a soft H2 trade.

What if RBA Doesn't Hike in AUG?

A rate hike in August isn't a shoo-in, despite, today's inflaton data, with the money market actually priced a little under 50% for a rise.

Madeline Dunk, Economist at ANZ Bank says "the cash rate has peaked," as trimmed mean inflation is still tracking slightly below RBA forecasts and there's increasing evidence of a slowing economy.

Any decision to hold rates would, on balance, weigh on AUD on the day.

Money markets are nevertheless still priced for a hike by the September meeting, meaning if August is skipped, it's done in September.

That means any post-decision weakness in AUD would be relatively short-lived as markets await the final move.

But, a September hike doesn't change the view that the market thinks 2027 will see the RBA cutting rates.

And that's the big story for AUD into year-end.

For GBP/AUD, The Floor is In

The rates story times with a better supported GBP/AUD.

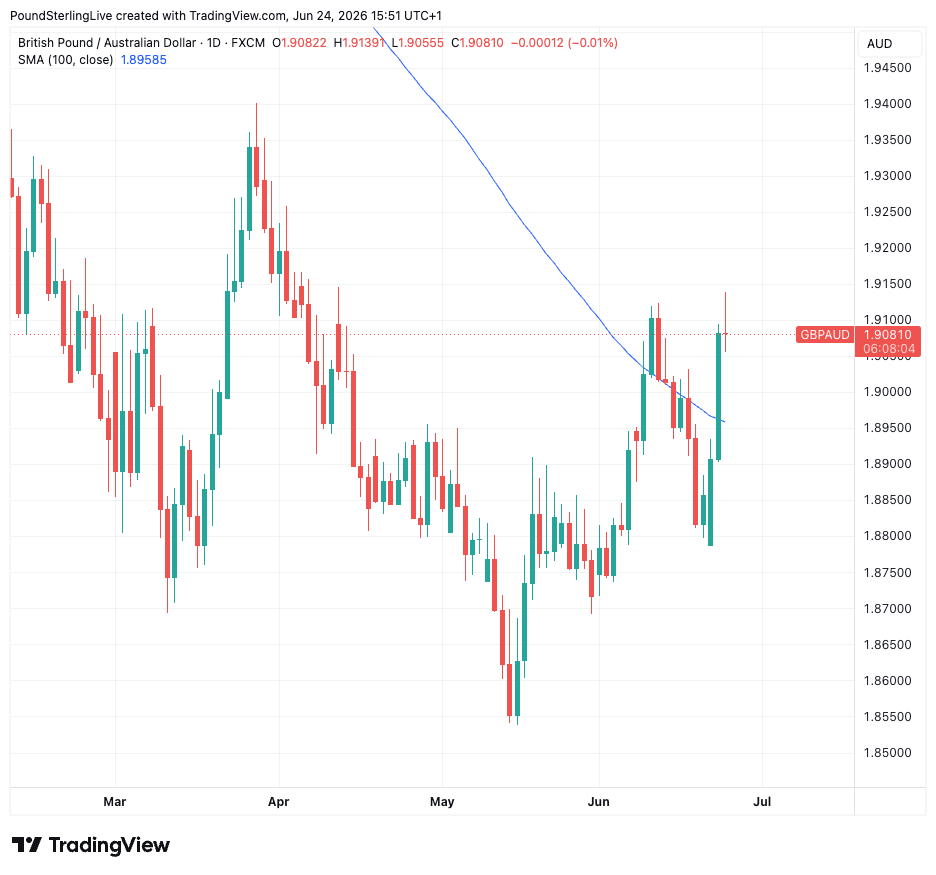

GBP/AUD fell to a low of 1.8537 in mid-May, a move that marked the culmination of months of near-relentless selling.

To be sure, although 1.8537 is the low, the real support line is more likely at 1.87, which has held sellers at bay on numerous occasions since March.

Now, the pair is looking to build a recovery sequence. Technicals are still relatively mixed, but a couple of daily closes above the 100-day moving average would help draw a conclusion that the selloff of H1 has completed.

That technical observation would gel nicely with the view that the AUD's supportive rates story has faded.