Image © Adobe Images

The Australian Dollar's strong start to 2025 looks set to extend, with domestic jobs data pointing to a robust economy.

The Australian Dollar is the second-best-performing G10 currency in 2025 amidst improving global economic sentiment and strong domestic performance.

Outperformance comes amidst bullish global investor sentiment, stability on the Chinese news front and ongoing domestic economic strength.

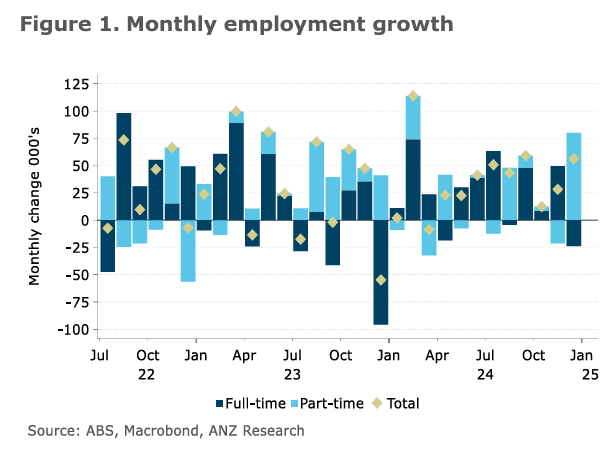

The robust domestic picture was fortified Thursday by news employment rose by 56.3K in December from 28.2K in November, exceeding a market estimate for growth of 15K.

The report's strength slightly lowered the odds of a February interest rate cut at the Reserve Bank of Australia, which mechanically lifts the currency.

"AUD/USD temporarily lifted to near 0.6250 after Australian jobs growth surprised to the upside," says Kristina Clifton, FX Strategist at Commonwealth Bank of Australia.

The Australian-U.S. Dollar exchange rate has risen for three days now and trades at 0.6210, ensuring it now holds a gain for the year. This, as most other developed world currencies nurse losses against a rampant U.S. Dollar.

Indeed, AUD is up against all its peers, with the Pound to Australian Dollar exchange rate having fallen to 1.9653 from 2.02 on January 02. The Euro to Australian Dollar rate has fallen from 1.6750 to 1.6562 in 2025.

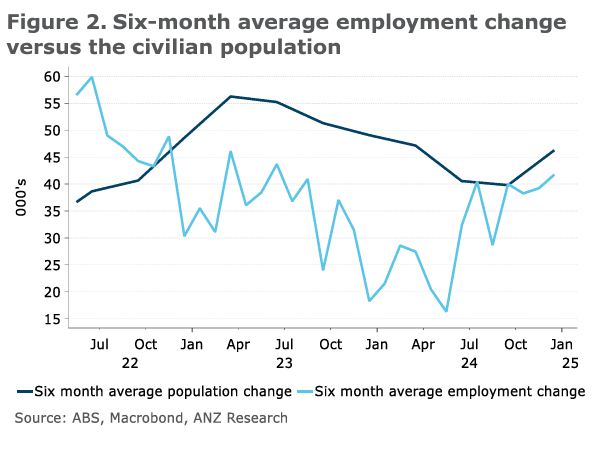

At a three-month average pace of 2.7% y/y, employment growth is unchanged versus three months ago and is only slightly below the 3.0% pace recorded a year ago in December 2023.

"Perhaps most impressive is the fact that the employment-to-population ratio once again rose to a fresh record high in December, up to 64.5% – a sign that the labour market, while having eased somewhat over the past two-or-so years, remains in a solid state in aggregate," says Ryan Wells, an economist at Westpac.

A strong labour market implies wages will remain robust, and central banks work from an assumption that higher wages bolster domestic inflation rates.

Image courtesy of ANZ.

The strong labour market, therefore, lessens the need for the RBA to cut interest rates on February 18, which would mechanically support Australian bond yields and the currency.

However, a number of Australian economists think the Bank might still pull the trigger owing to signs of a slow and steady easing in inflation. Australia's monthly trimmed-mean CPI was reported at 3.2% in November, from 3.5%, reinforcing 2025 RBA rate cut expectations.

The RBA's most recent policy meeting hinted at a potential cut in early 2025, with the Bank shifting its language to show it was now less concerned about the persistence of inflation. The Bank's minutes from the December policy meeting said there was the potential for "relaxing the degree of monetary policy tightness".

Image courtesy of ANZ.

From a currency perspective, a surprise RBA cut in February might not damage the AUD's rebound. What is clear is that the economy is in good shape, and there will be limited scope to cut too far.

In short, what matters is how many cuts will come across the duration of 2025, and not necessarily whether the central bank cuts in February or waits.

On this count, the RBA looks like it will be in the slow lane, particularly given the message from the labour market.

The AUD looks set for further outperformance in the coming weeks.