Image © Adobe Stock

The Pound-to-Australian Dollar exchange rate (GBPAUD) could tap 2.0 in the week ahead, but this will require a dovish Reserve Bank of Australia (RBA) decision and some above-consensus UK inflation data.

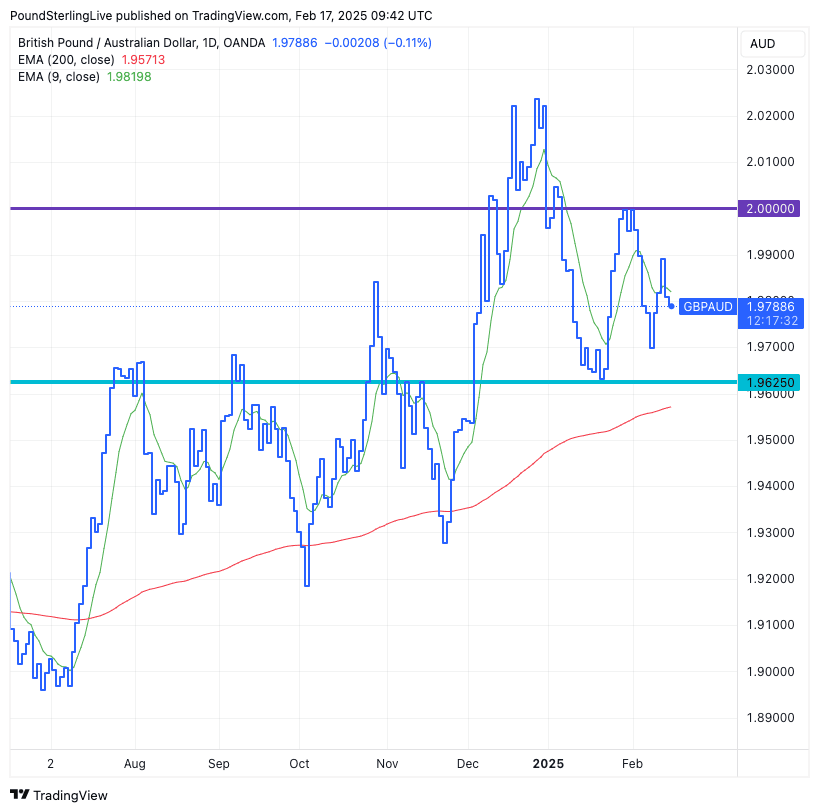

The Pound is looking for direction against the Australian Dollar amidst a process of consolidation, and luckily, the coming week looks set to provide events that can allow this to happen.

The consolidation comes amidst a drop in volatility centred around 1.9820, which is the nine-day moving average, which is the centre of a broad range that is contained by 2.0 at the top and 1.96250 at the bottom:

Above: GBPAUD at daily intervals, showing the daily close and opens. This shows a recent growth spurt has evolved into a consolidation, albeit within quite a wide area.

Some observations to consider for those with AUD-based payments in the coming week:

- The uptrend is still alive as spot is above the 200-day exponential moving average (EMA). This level is down at 1.9571 and only when we break below here does the market flip into a downtrend.

- While above the 200-day EMA we expect periods of weakness to be shallow, giving way to fresh highs

- GBPAUD can enter prolonged periods of sideways trade, albeit in a wide zone. This means it's difficult to call directional moves and it is best to position for sideways churn.

A busy week for both sides of the GBP/AUD equation gets underway on Tuesday when the Reserve Bank of Australia is expected to cut interest rates.

The consensus is leaning towards a 25 basis point cut, with the associated guidance likely to be cautious and noncommittal regarding further cuts. This would be a 'hawkish' cut that could ultimately support AUD and push GBPAUD down to support at 1.9625.

"We acknowledge the risk of a hawkish surprise by the RBA, either by keeping the cash rate unchanged at 4.35% or via cautious guidance from Governor Bullock at the press conference," says Nicholas Chia, FX and Macro Strategist at Standard Chartered. "On AUDUSD, a hawkish cut by the RBA may nudge the pair above the 0.64 level."

However, should the RBA cut rates and suggest it stands ready to deliver more in the coming year, then the AUD can weaken, and GBPAUD would be on course to hit 2.0.

There is a degree of uncertainty as to which way the RBA will steer markets, which means we could see some decent volatility.

Week Ahead: AUD

Tuesday:

? Reserve Bank of Australia (RBA) Policy Decision

Expected Cash Rate: 4.10% (cut from 4.35%)

Previous: 4.35%

? Market Impact: If the RBA delivers the expected 25bps rate cut, it may put short-term pressure on AUD as rate differentials move against it. However, a pause or a more hawkish tone could support the AUD.

? RBA Statement on Monetary Policy

? Market Impact: The statement will provide guidance on future rate cuts. If the RBA signals a slow pace of cuts or remains concerned about sticky inflation, AUD could find support.

Wednesday, February 19

? Westpac-MI Leading Index (Jan, Annualised Growth Rate)

Previous: +0.25%

? Market Impact: A stronger-than-expected reading suggests economic resilience, which could limit AUD downside. A weaker print reinforces slower growth risks, weighing on AUD.

? Q4 Wage Price Index (WPI, QoQ & YoY)

Expected (QoQ): 0.8%

Previous (QoQ): 0.8%

Expected (YoY): 3.2%

Previous (YoY): 3.5%

? Market Impact: Lower-than-expected wage growth could increase expectations of further RBA cuts, weighing on AUD. If wages surprise to the upside, markets may scale back rate cut bets, supporting AUD.

Thursday, February 20

? Employment Change (Jan, MoM)

Expected: +15K jobs

Previous: +56.3K jobs

? Market Impact: A weaker-than-expected employment gain may increase expectations of further rate cuts, weakening AUD. A stronger print would suggest labor market resilience, reducing RBA easing expectations and supporting AUD.

? Unemployment Rate (Jan)

Expected: 4.1%

Previous: 4.0%

? Market Impact: If unemployment rises more than expected, AUD could decline due to growing concerns about slowing economic momentum. A lower unemployment rate would ease concerns and support AUD.

Friday, February 21

? RBA Parliamentary Testimony

? Market Impact: If RBA officials push back on aggressive rate cut expectations, AUD could rally. A dovish tone may further weaken the currency.

Potential Market Implications for AUD

Putting it all together:

✅ Bullish (AUD Strengthening) Scenarios:

The RBA does not cut rates or signal a slow pace of easing.

Stronger-than-expected wage growth or employment data, reducing expectations of rate cuts.

Hawkish RBA parliamentary testimony, suggesting inflation risks persist.

❌ Bearish (AUD Weakening) Scenarios:

RBA cuts rates and signals further easing in 2025.

Weak wage growth reinforces expectations of lower inflation and rate cuts.

Higher unemployment rate and slower employment growth.

Soft Westpac-MI Leading Index, indicating weaker economic momentum.

Week Ahead: GBP Faces Crucial Wage and Inflation Data

Tuesday, February 18

? Average Weekly Earnings (Dec, YoY)

Inc. Bonuses: 5.9% (expected) vs. 5.6% (previous)

Ex. Bonuses: 5.9% (expected) vs. 5.6% (previous)

? Market Impact: A higher-than-expected figure could reinforce inflationary wage pressures, possibly influencing the Bank of England’s (BoE) policy stance.

? ILO Unemployment Rate (Dec)

Expected: 4.5%

Previous: 4.4%

? Market Impact: If unemployment rises, it could signal labor market softening, potentially weakening GBP.

? Employment Change (Dec, 3m/3m)

Expected: 50K

Previous: 35K

? Market Impact: A strong reading indicates resilient hiring trends, supporting growth and possibly keeping wage growth elevated.

? BoE Governor Andrew Bailey Speaks

? Market Impact: If Bailey delivers hawkish remarks, GBP may strengthen as markets price in fewer rate cuts in 2025. A dovish tone could weigh on GBP/AUD.

Wednesday, February 19

? Consumer Price Index (CPI) (Jan, YoY & MoM)

MoM Expectation: -0.3% vs. -0.2% (previous)

YoY Expectation: 2.8% vs. 2.8% (previous)

Core CPI (YoY): 3.7% vs. 3.2% (previous)

? Market Impact: A slowdown in inflation would increase the probability of BoE rate cuts later in 2025, weighing on GBP. A stronger print could delay rate cuts.

? CBI Industrial Trends Orders (Feb)

Expected: -30

Previous: -34

? Market Impact: A higher-than-expected figure suggests improving UK manufacturing sentiment, but the sector remains weak overall.

Friday, February 21

? GfK Consumer Confidence (Feb)

Expected: -24

Previous: -22

? Market Impact: A lower confidence reading reflects weaker consumer sentiment, possibly dampening future spending and economic growth.

? Retail Sales (Jan, MoM & YoY)

Inc. Automotive Fuel (MoM): 0.5% (expected) vs. -0.3% (previous)

Ex. Automotive Fuel (MoM): 0.9% (expected) vs. -0.6% (previous)

? Market Impact: A rebound in retail sales could support GDP growth and indicate stronger consumer spending, boosting GBP.

? Public Sector Net Borrowing (Jan)

Expected: -£20.3bn

Previous: £17.8bn

? Market Impact: Lower borrowing could ease fiscal pressures, but higher-than-expected borrowing might increase concerns over government debt levels.

? UK Services PMI (Feb, Preliminary)

Expected: 51.0

Previous: 50.8

? Market Impact: A reading above 50 signals expansion, which may support UK economic optimis and boos the Pound.

? UK Manufacturing PMI (Feb, Preliminary)

Expected: 48.5

Previous: 48.3

? Market Impact: Still in contraction (<50), but a slight improvement could signal bottoming out of the UK manufacturing sector.