Image © Adobe Images

The British Pound retains a soft directional bias against the Australian Dollar, with 2025 being characterised by selloffs interspersed with tepid bouts of consolidation.

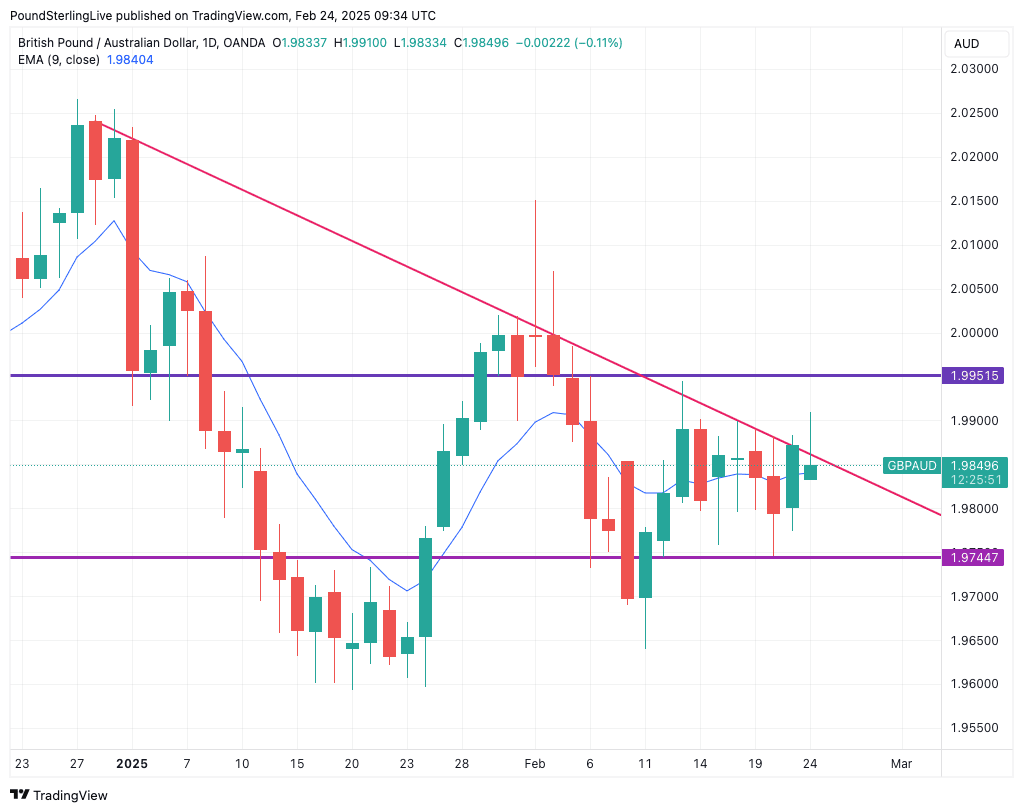

Near-term, we are looking at another period of tepid consolidation to evolve around the nine-day exponential moving average (EMA) at 1.9840, which is where we find the level of spot on Monday.

As the chart below shows, the Pound-to-Australian Dollar exchange rate (GBPAUD) has been trending down since late December, with the downward trendline capping recovery attempts and ultimately keeping its nose pointed lower:

Above: GBP/AUD at daily intervals.

With a relatively light calendar in the UK and Australia this week, we would expect this technical setup to hold sway, which advocates for another test of last week's lows at 1.9744 at some point in the coming days.

The level forms a support level, which if broken, would open the door to a move to January lows at 1.96.

The recent sideways drift seen in the setup also speaks of easing volatility levels in global FX, a testament to the waning impact of U.S. President Donald Trump's tariff proclamations.

The playbook heading into 2025 said that Australia was prone to weakness on tariffs, but Trump has shown he is not interested in pursuing worst-case tariff scenarios.

For one, it looks as though he is going much easier on China, which is Australia's main trade partner and key vulnerability in the event of a tariff war.

Even if Trump talks tariffs this week, any negative impact on AUD should soon fade, capping GBPAUD upside in the process.

That being said, the case for outright AUD gains will be tempered by growing market caution as April 01 approaches. This is when the U.S. will introduce tariffs that match the import duties other countries impose on U.S. goods.

On April 02, a 25% tariff on foreign cars, semiconductor chips and pharmaceuticals is expected to be announced.

Domestically, there is some interest for AUD:

- Monthly CPI Indicator (Feb 26): Forecasted to slightly ease from the previous 2.5% annual rate.

- Q4 Private New Capital Expenditure (Feb 27): Expected to grow at 0.8% q/q, slightly slower than the prior quarter.

- Q4 Construction Work Done (Feb 26): Forecasted at 1.0% q/q, continuing the growth trend in engineering and residential construction.

- January Private Sector Credit (Feb 28): Expected to rise by 0.5% m/m, reflecting softer housing credit growth.

The Reserve Bank of Australia (RBA) events for the week commencing February 24, 2025, are scheduled as follows:

- Tuesday, February 25 – Assistant Governor (Financial System) Jones fireside chat at DLT-Enabled.

- Thursday, February 27 – Speech by the Head of Economic Analysis, Plumb, on the importance of productivity at the ABE Conference.

The RBA cut interest rates last week but the guidance was more 'hawkish' than expected, with the RBA signalling it is not yet ready to commence a fully-fledged cutting cycle. This limits the scope of further cuts this year and supports AUD.

A strong run of data would underpin this recalibration, and we would expect the RBA speakers to warn that inflation risks in Australia mean it is too soon to consider another imminent cut.

Central Bank Speak is Also the Highlight of the GBP Calendar

Deputy Governor for Monetary Policy at the Bank of England, Clare Lombardelli, will give the opening remarks on Monday at the annual BEAR conference. Chief Economist Huw Pill will deliver the closing remarks to the same conference; his comments are always closely followed.

In the afternoon, Dave Ramsden will discuss the Bank’s balance sheet ahead of the Bank’s decision on its future balance sheet later in the year. Ramsden will deliver another speech on Friday, giving him ample scope to touch on interest rates.

Ramsden is important because he is 'dovish', and we will be interested to hear whether he would vote for another interest rate cut next month. Any hint of hesitation, in light of rising inflation pressures, would bolster GBP.

Swati Dhingra will also be speaking, and she will almost certainly confirm she will be voting to cut again next month. As her views are so predictable, she is not expected to be a market mover.

The market has lowered bets for the number of rate cuts to come from the Bank this year, following last week's consensus-beating economic data prints, and is now pricing in just two more cuts.

We know the Bank itself would prefer about three more cuts (maintaining its quarterly run rate), and it is therefore hard to see how this repricing can continue. Some 'dovish' MPC members will likely try to encourage the market to price in more cuts, which would technically weigh on Pound Sterling.

However, we would expect weakness to be limited, as the economy has a louder voice, and right now, it is warning that inflation risks are notably tilted to the upside, limiting the scope for Bank of England rate cuts.