Image © Adobe Images

The Pound-to-Australian Dollar exchange rate (GBP/AUD) is ready to pull back and unwind from overbought conditions.

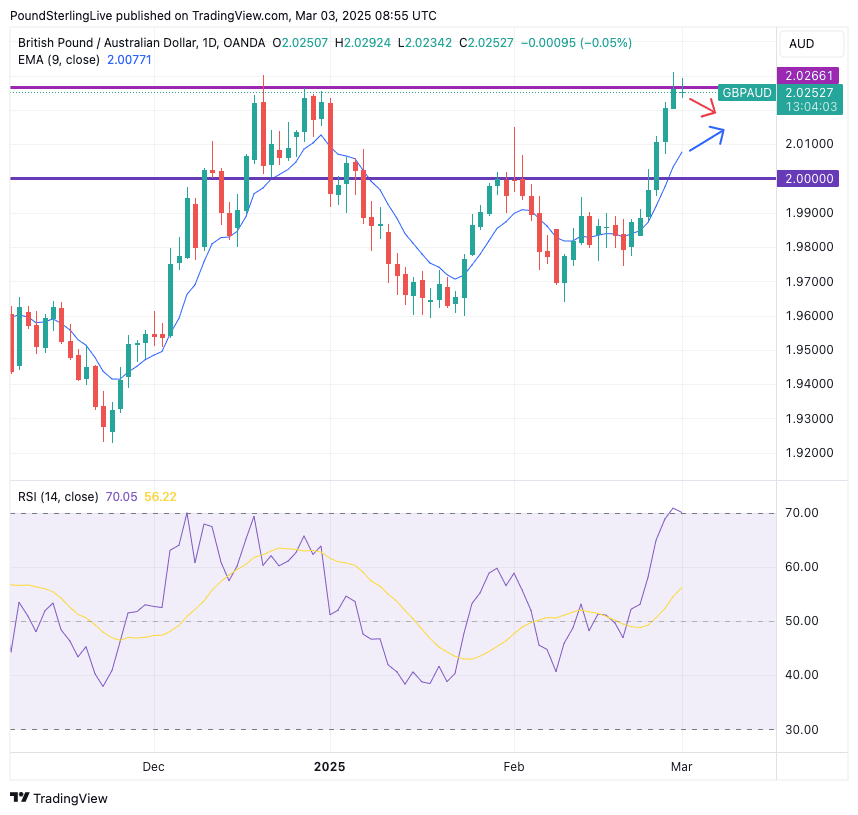

GBP/AUD scaled a new near-five-year high at 2.0309 last week and remains close by on Monday at 2.0226, confirming that the broader, multi-month, multi-year trend remains to the upside.

But, our interest here is what happens in the week ahead, and the signals are advocating for a pullback, with GBP/AUD having diverged quite significantly from its nine-day exponential moving average (EMA).

We watch the nine-day EMA as a short-term indicator, judging that if an exchange rate is above it, the trend higher trend is to be preferred.

However, when the exchange rate diverges significantly from the nine-day EMA we prepare for the gap to close and look for a consolidative correction.

This is where we are with GBP/AUD right now, and we would look for the exchange rate to fall and meet the rising EMA, which gives an approximate target of 2.0200.

Above: GBPAUD at daily intervals.

The overbought signal is confirmed by the Relative Strength Index (RSI), located in the lower pane in the chart. The RSI breached 70, which makes it technically overbought and advocating for a consolidation or pullback.

Recent AUD weakness follows rising tensions ahead of the March 04 U.S. tariff announcement for Canadian and Mexican imports, which if confirmed would signal a notable setback to free trade is indeed underway.

"Increased trade friction, and its potential to negatively impact global growth, could dampen global risk appetite and weigh on the AUD/USD," says Preksha Jain, FX Strategist at ANZ Bank.

"AUD/USD will ease further this week because 'peak tariff' has not yet been reached. Instead, the global trade war is intensifying with the US set to impose higher tariffs on imports from China, Canada and Mexico on Tuesday. U.S. tariffs on imports (particularly from China) will spillover to pull AUD/USD lower in our view," says Kristina Clifton, FX Strategist at Commonwealth Bank of Australia.

However, the AUD would benefit if U.S. President Donald Trump announces a delay to tariffs on Mexican and Canadian goods or announces a package that is less severe than the 25% import tariff he has touted since coming into office.

This would be consistent with a view that further tariff packages will be prone to negotiation, meaning a worst-case global tariff outcome is ultimately avoided.

For risk-sensitive, pro-trade currencies, such as the Australian Dollar, this is a supportive development and one we think is highly likely this week.

But what mood is Trump in? Will he be all-out 'hawkish' and announce maximalist tariffs on Canada and Mexico, in line with his 'hard man' stance that was on display on Friday when he clashed with Ukrainian President Volodomyr Zelensky in the White House?

Or will he be the familiar Trump that we got to know in his first term, where tariffs were watered down, delayed or ultimately cancelled following negotiations? Recall that in his first term, Trump ultimately cancelled tariffs placed on Mexico after just three days following concessions made by Mexico.

Above: Trump said at the first cabinet meeting of the administration that tariffs would proceed this week. The comments caused risk-on assets like AUD to decline. Official White House Photo by Molly Riley.

U.S. Commerce Secretary Howard Lutnick on Sunday confirmed tariffs were still going ahead, but he said they are yet to be determined. He noted concessions from Canada and Mexico had been made, which suggested some type of compromise would be reached.

Any hint of compromise will be taken as pro-risk, which would benefit the likes of the Australian Dollar.

The Pound would come under broad pressure under any tariff-inspired relief as it has proven to be something of a safe haven amidst tariff fears.

Last week, Trump hinted that the U.S. and UK would work towards a trade deal, which carves out the Pound as relatively insulated from the tariff threat. However, when that threat recedes, any safe-haven premium must be unwound, which could result in weakness.

Keep an eye on Friday's U.S. jobs report, too. This is a highly anticipated publication as it would give some signal as to whether the slowdown seen in a host of U.S. survey data is manifesting in official data.

The ten-year U.S. bond yield has fallen below 4.4%, its lowest since December 12, and money markets show investors now see 54 basis points of easing from the Fed by the end of the year, compared to 48bp on Monday.

This means there are now two 25bp cuts expected this year, confirming that investors think the U.S. economy is slowing. It also suggests they think the government's efforts to lower the country's debt will pay off.

Elon Musk's DOGE programme is snipping away at the deficit, which reached 6.4% of the GDP in 2024, but analysts say that the amounts being achieved so far are relatively small as a percentage of total expenditure.

However, DOGE's message is bigger than the actual cuts it delivers: that Trump is determined to lower the country's debt. This boosts bets for rate cuts via two channels: 1) lower debt = less bond issuance = lower bond yields. 2) increased policy uncertainty weighs on business and consumer sentiment = slowing economy = slowing inflation = rising rate cut bets = lower bond yields.

If bond yields continue to fall, then the Dollar can soften, and stocks can rise.

This pro-risk environment would boost the Australian Dollar, which is a proxy for global sentiment.

We will also be watching China this week, where the 'two sessions' get underway.

This is the annual meeting of China's top legislature, the National People's Congress (NPC), and the top political advisory body, the National Committee of the Chinese People's Political Consultative Conference (CPPCC).

Here, the direction of the economy will be decided. Investors are looking for signs that authorities plan to boost stimulus in anticipation of any tariff-inspired slowdown.

This would help the Australian Dollar, which trades as a proxy to China, as Australia is highly reliant on trade with China.

Based on these expectations, we wrote last week that China could offer AUD a route higher in March, which would hint at a more notable pullback in GBP/AUD over the coming weeks.

"The tariff war between the U.S. and China may encourage the Chinese government to announce stronger demand stimulus at this week’s National People’s Congress to offset the negative impacts of tariffs on the external sector," says Clifton.