Image © Adobe Images

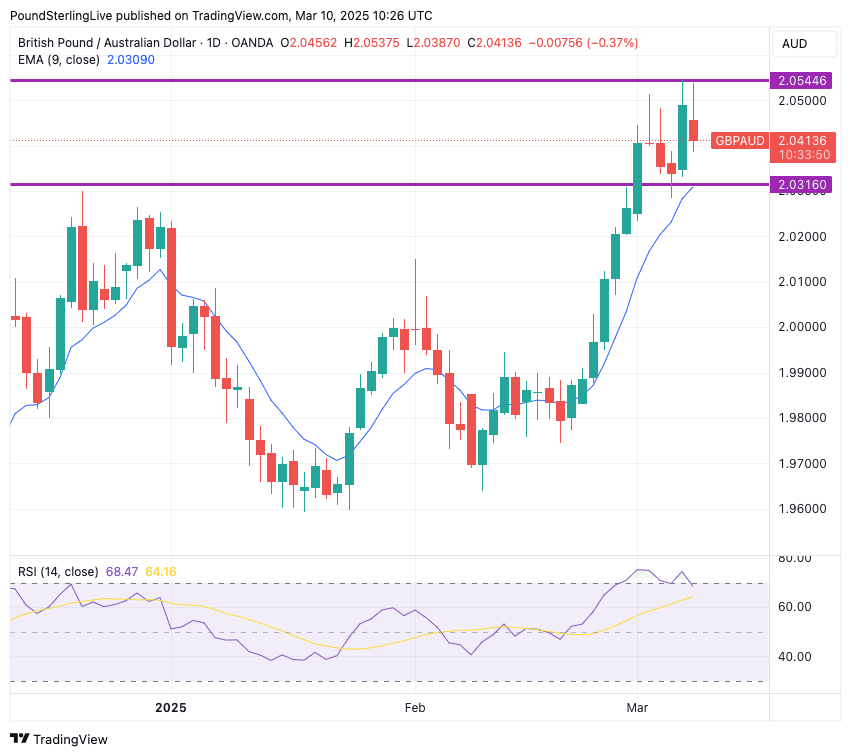

GBP/AUD has broken into a new, higher range.

The Pound-to-Australian Dollar exchange rate (GBPAUD) rose by 1.10% last week as it broke above a major resistance zone, confirming that a new, higher range will likely evolve.

The confirmed break above resistance at 2.0316 underpins the constructive technical setup in the pair, with a subsequent high being printed at 2.0544, which was the highest level recorded in nine years.

The new week starts with a pullback from that high, in line with a turn lower in the Relative Strength Index (RSI) to just below 70:

Above: GBPAUD at daily intervals.

This is important, as the RSI was screening as overbought all last week, and the subsequent retreat forms part of a necessary consolidation in the market from overbought conditions.

Our Week Ahead Forecast model predicts that GBP/AUD will broadly trade within a range between 2.0316 and 2.0544.

Weakness should be shallow as the overall setup remains constructive, and risks will remain to the upside.

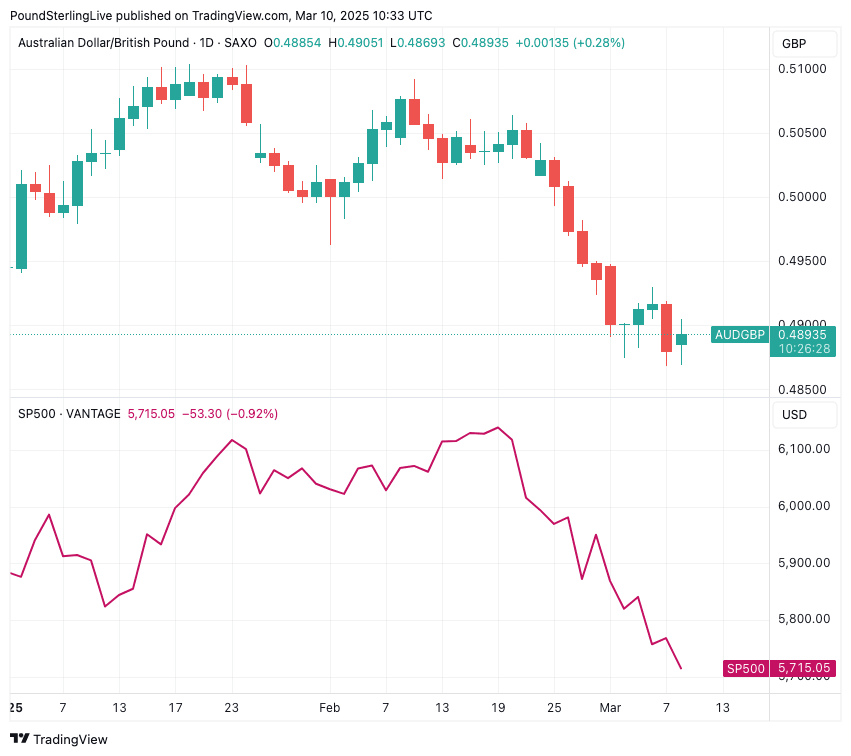

Australian Dollar losses track the pullback in global investor sentiment and U.S. stock markets over fears that U.S. tariffs pose significant challenges to the world's economy.

Given the strong correlation, further weakness in U.S. equities should keep AUD under pressure against the Pound:

Above: AUDGBP tracks the S&P 500 stock index lower.

The Australian Dollar fell to new multi-year lows against the GBP and EUR last week after China's foreign minister said his country will continue to retaliate for the "arbitrary tariffs" imposed by the U.S.

Analysts say the pointed comments by Beijing's most senior foreign affairs official point to a ratcheting up of a trade war that has implications for Australia due to its significant trade linkages with China.

This week starts with China confirming a host of new tariffs on U.S. imports, with the agricultural sector bearing the brunt of the tariffs.

Turning to the domestic agenda, Tuesday brings the Westpac-MI Consumer Sentiment reading for March.

If sentiment rises, it could signal consumer optimism, supporting AUD.

The NAB Business Survey for February is also due for release, where a stronger-than-expected reading would suggest improving business conditions, potentially supporting AUD.

A decline could indicate weaker corporate sentiment, raising concerns about slower growth.

Thursday sees the release of the Melbourne Institute (MI) Inflation Expectations for March, which will give us a signal as to whether Aussie inflation remains too high to entertain a follow-up interest rate cut at the Reserve Bank of Australia anytime soon.

Turning to the UK, Friday's UK Monthly GDP report will be the data highlight of the coming week.

"As the first month of the quarter and year, January’s GDP outturn will play a big part in setting the tone for growth expectations for both Q1 and the whole of 2025. We expect January GDP to rise by 0.1% m/m," says Hann-Ju Ho, Senior Economist at Lloyds Bank.

If GDP beats expectations, the pound will rise into the weekend, as this would confirm that fears of a material slowdown are exaggerated, taking pressure off the Bank of England to cut interest rates.