Image © Adobe Stock

The Pound can extend a short-term recovery against the Canadian Dollar in the coming days.

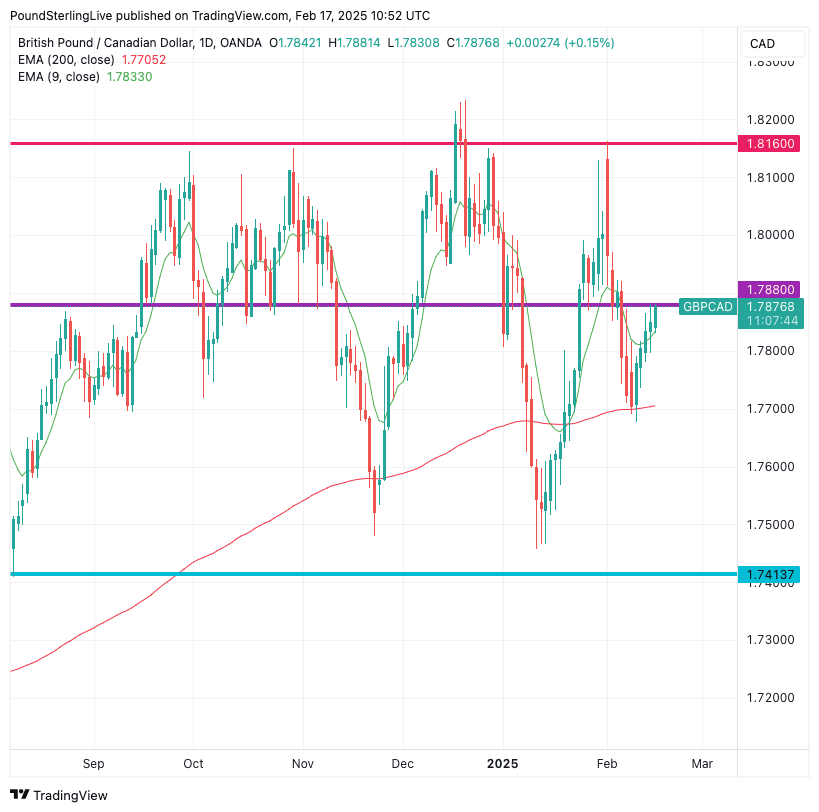

The Pound-to-Canadian Dollar exchange rate (GBPCAD) recently fell to the 200-day moving average on the daily chart, where it promptly found buying interest and rebounded, keeping alive a longer-term uptrend in the process.

Our Week Ahead Forecast for higher levels rests on the belief that this particular recovery sequence can extend.

Above: GBPCAD at daily intervals.

A rule-of-thumb we deploy when assessing an exchange rate's outlook is that it is in an uptrend while above the 200-day moving average, which GBPCAD has managed to defend.

That being said, this can hardly be described as a decisive and clean uptrend, and as the chart above shows, a rather random sideways chop has been in place for nearly half a year now.

That chop is, in fact, an oscillation between a clearly defined ceiling at 1.8160 and a floor at 1.7413. But as the chart shows, there is also support at around 1.77, where a recent selloff was arrested on February 11.

A pivot lies at approximately 1.7880, and the anticipated move above here opens the door to 1.7950.

Much will depend on the nature of Canadian inflation numbers due on Tuesday, where a rise in CPI inflation of 0.1% month-on-month is anticipated for January, marking a return from deflation of -0.4% in December.

A stronger reading would be reflexively supportive for CAD as it would imply the Bank of Canada has increased scope to pause the rate cutting cycle later in the year.

However, an undershoot and another deflationary reading would have the opposite effect.

Will the numbers materially impact the Bank of Canada's outlook? We don't think so and anticipate any CAD moves to fade as we think the Bank will maintain a dovish approach to policy in the coming weeks and months owing to uncertainty over U.S. tariffs and policy.

"Risks of a further spike in the CAD's tariff premium are ever-present ahead of the end of the one-month grace period on 3 March and a more definitive resolution to the US-Canada trade spat," says a weekly FX market note from Barclays.

That said, the Canadian Dollar has already ridden out some tariff-related volatility since Donald Trump came to power and could continue to find support as the perceived tariff threat fades further.

Trump has shown tariffs to be part of a negotiating ploy, lessening the more severe downside scenarios for CAD.

The UK calendar will be busy this week and offers some GBP-specific GBPCAD volatility.

The data pulse is in the process of recovering, having cratered after the country came under new management following last year's July election.

With expectations so low, the prospect of upside surprises has grown, which can boost the Pound.

Here's what to watch:

Tuesday, February 18

? Average Weekly Earnings (Dec, YoY)

Inc. Bonuses: 5.9% (expected) vs. 5.6% (previous)

Ex. Bonuses: 5.9% (expected) vs. 5.6% (previous)

? Market Impact: A higher-than-expected figure could reinforce inflationary wage pressures, possibly suggesting the Bank of England must maintain a steady stance on interest rates. This would bolster GBP.

? ILO Unemployment Rate (Dec)

Expected: 4.5%

Previous: 4.4%

? Market Impact: If unemployment rises, it could signal the labour market softening, potentially weakening GBP.

? Employment Change (Dec, 3m/3m)

Expected: 50K

Previous: 35K

? Market Impact: A strong reading indicates resilient hiring trends, supporting growth and possibly keeping wage growth elevated.

? BoE Governor Andrew Bailey Speaks

? Market Impact: If Bailey delivers hawkish remarks, GBP may strengthen as markets price in fewer rate cuts in 2025. A dovish tone could weigh on GBP.

Wednesday, February 19

? Consumer Price Index (CPI) (Jan, YoY & MoM)

MoM Expectation: -0.3% vs. -0.2% (previous)

YoY Expectation: 2.8% vs. 2.8% (previous)

Core CPI (YoY): 3.7% vs. 3.2% (previous)

? Market Impact: A slowdown in inflation would increase the probability of BoE rate cuts later in 2025, weighing on GBPCAD. A stronger print could delay rate cuts and boost the exchange rate.

? CBI Industrial Trends Orders (Feb)

Expected: -30

Previous: -34

? Market Impact: A higher-than-expected figure suggests improving UK manufacturing sentiment, but the sector remains weak overall. This data series tends to have a limited market impact.

Friday, February 21

? GfK Consumer Confidence (Feb)

Expected: -24

Previous: -22

? Market Impact: A lower confidence reading reflects weaker consumer sentiment, possibly dampening future spending and economic growth.

? Retail Sales (Jan, MoM & YoY)

Inc. Automotive Fuel (MoM): 0.5% (expected) vs. -0.3% (previous)

Ex. Automotive Fuel (MoM): 0.9% (expected) vs. -0.6% (previous)

? Market Impact: A rebound in retail sales could support GDP growth and indicate stronger consumer spending, boosting GBP.

? Public Sector Net Borrowing (Jan)

Expected: -£20.3bn

Previous: £17.8bn

? Market Impact: Lower borrowing could ease fiscal pressures, but higher-than-expected borrowing might increase concerns over government debt levels.

? UK Services PMI (Feb, Preliminary)

Expected: 51.0

Previous: 50.8

? Market Impact: A reading above 50 signals expansion, which may support UK economic optimism and boost the Pound.

? UK Manufacturing PMI (Feb, Preliminary)

Expected: 48.5

Previous: 48.3

? Market Impact: Still in contraction (<50), but a slight improvement could signal bottoming out of the UK manufacturing sector.