- The U.S. and Germany are piling on the debt

- Leaving already heavily indebted countries like the UK exposed

- This could push UK debt yields even higher

- At some point, this will become negative for GBP

- Long-term investors are worried, warns Morgan Stanley

File image of Rachel Reeves. Picture by Kirsty O’Connor / Treasury.

Pound Sterling could be on a downward slope against the Euro as UK debt worries mount.

Analysts at investment bank Morgan Stanley have just issued some important research into the British Pound that we think readers should be aware of, given the prevailing discussions about the sustainability of government debt.

Researchers say that the Pound is fine for now, but there is a decent risk that another confidence crisis strikes, which could send it hurtling lower.

Interestingly, the risks are likely to be particularly evident against the Euro, leaving analysts wary that the Pound will fall back to multi-year lows in the coming months.

"As we saw in January and in other periods before, there can be an unexpected emergence of a 'tipping point' where the GBP-gilt correlation flips from positive to negative and where risk premium could prove problematic," says David S. Adams, a currency researcher at Morgan Stanley.

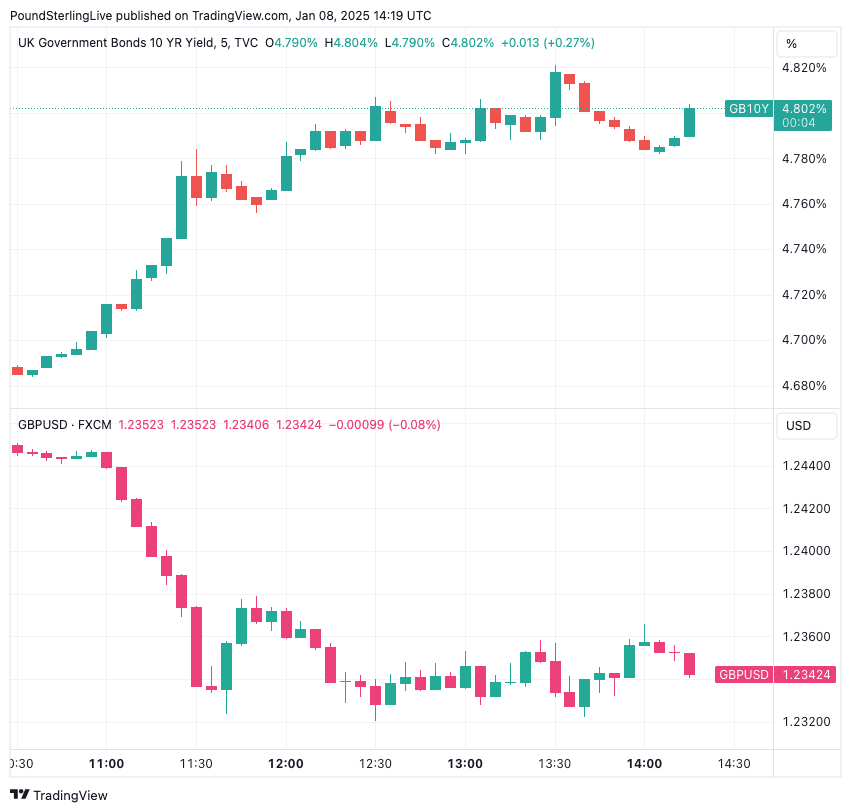

To recap: in January, the Pound slumped DESPITE UK bond yields rising, which meant a typically steady relationship between the currency and the all-important bond market had broken, signalling investor concerns that the UK was becoming too indebted.

Worries were centred on Chancellor Rachel Reeves' tax hikes announced in October 2024, which were deemed to be negative for growth at a time of ballooning debts. If the government is to pay off the country's debt, the economy must grow.

Above: The correlation flip that hit GBP in January. Read: Pound Sterling Caught in a "Fiscal Death Spiral"

However, the most famous episode of the bond-pound breakdown occurred in October 2022 when Liz Truss tried to pass her mini budget that markets deemed as not being credible, in that the UK would struggle to pay for the largesse proposed.

The important point is that these episodes tend to crop up, and the worry at Morgan Stanley is that the fear of another one occurring in the coming months will sideline long-term investors in the GBP, prompting it to ultimately trend lower.

Big Debt is a Big Deal Again

The UK's high interest rates relative to most other G10 countries are seen as a key driver of Pound Sterling outperformance.

This is because foreign investors seek out the greater returns that UK assets (usually government bonds) offer, creating a flow that boosts the Pound.

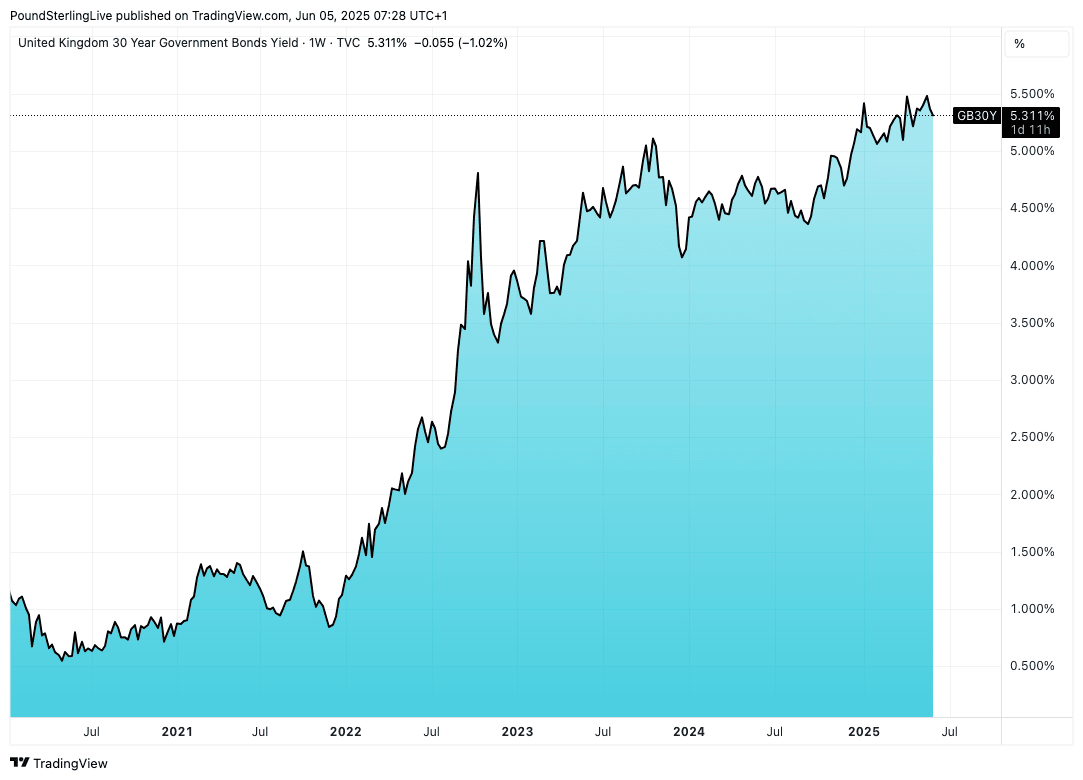

Above: Long-term yields on the UK's 30-year bond reflect a demand for increased compensation by investors.

However, risks are brewing as governments across the world continue to splash the cash, issuing debt to fund the spending.

This is particularly relevant today as the U.S. looks to pass President Trump's One Big Beautiful Bill, which will add trillions to the U.S. debt pile.

The bill is forecast to add $3.8 trillion to the existing $36 trillion national debt, according to the non-partisan Congressional Budget Office.

That is a lot of money that investors must stump up. Keep in mind, increased U.S. debt issuance will meet Germany's increase, as Chancellor Merz looks to rearm and boost infrastructure.

Yet even before this, the UK has a greater debt-to-GDP burden than both Germany and the U.S., and there are no signs Reeves intends to make the necessary spending cuts required to limit the UK's exposure to a strike by buyers of debt.

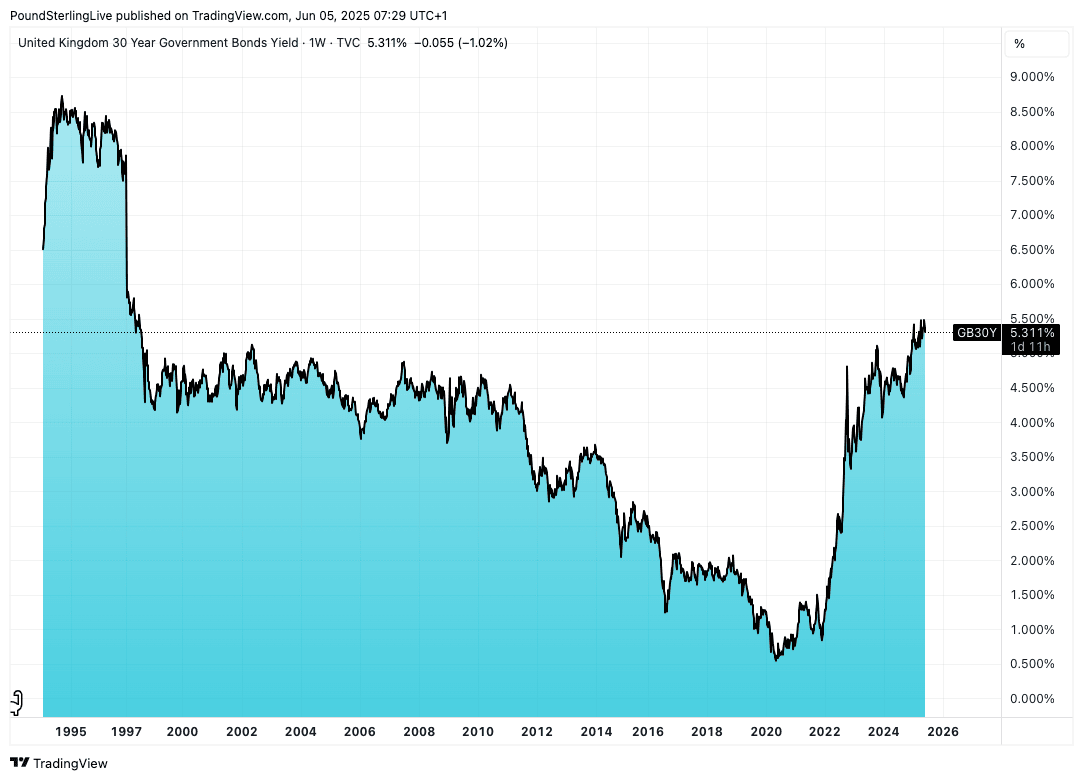

Above: The UK's 30-year bond is yielding at levels last seen in the late 1990s.

The UK Has a Debt (Premia) Problem

UK bond yields, particularly long-term bond yields, are elevated as investors demand a greater return for holding UK bonds.

For now, this is helping the Pound. But, Morgan Stanley explains this can change.

"If higher rates are driven by term premium, that may be seen as less sustainable and as indicating future volatility and adverse outcomes and returns. If yields are rising alongside higher term premium, the risk is that the correlation between GBP and UK yields breaks down like we saw in the past.

In fixed income markets, the term premium refers to the extra yield that investors require to hold a longer-term bond instead of a series of shorter-term bonds. It compensates for risks associated with time, such as uncertainty about inflation, interest rates, and the economy over the bond’s life.

When term premium rises, it usually signals that investors are demanding more compensation for long-run risks (e.g., fiscal instability, inflation uncertainty).

Rising term premium can push long-term yields up even if central banks keep short-term rates steady, which may disrupt markets or currencies.

In currency markets (like GBP/EUR), term premium affects capital flows. If higher UK bond yields are due to a rising term premium (and not economic strength), investors may view UK assets as riskier, potentially weakening the pound.

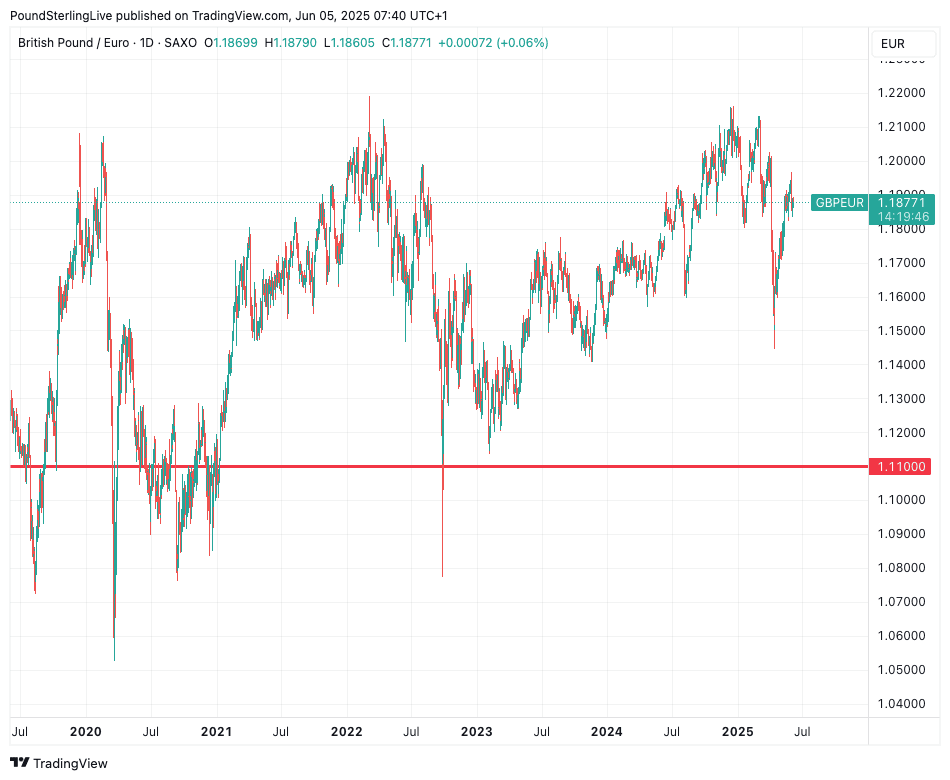

Above: GBP/EUR at daily intervals, showing the 1.11 level.

Pound-Euro at Risk

Interestingly, Morgan Stanley research shows the Pound to Euro exchange rate is particularly at risk of another breakdown in confidence towards the UK.

With debts rising and fiscal sustainability under scrutiny, there is the possibility that another episode of GBP weakness associated with rising debt costs is nearing.

"As we saw in January and in other periods before, there can be an unexpected emergence of a 'tipping point' where the GBP-gilt correlation flips from positive to negative and where risk premium could prove problematic," says Adams.

"This is a key reason why we think that EUR is likely to outperform GBP; investor caution about a sudden change in GBP's relationship may limit the enthusiasm with which investors may add GBP longs," he adds.

Morgan Stanley thinks this may keep EUR/GBP in an uptrend toward the top of its medium-term range of about 90c. In Pound-to-Euro terms, this would mean a fall back to 1.11.