Image © Adobe Images

Pound Sterling is under pressure against the euro ahead of the weekend, and strategists we follow think further weakness will be a feature of the coming weeks, owing to concerns over the Autumn budget and another Bank of England interest rate cut falling before year-end.

The Bank's decision to hold interest rates unchanged on Thursday was unremarkable, but there was no clear sign that it was ready to pause the cutting cycle.

In fact, the Bank displayed a confidence that it believesd inflation is about to peak and it will come down materially in 2026. With the market getting a whiff of further cuts, Sterling repriced lower across the board.

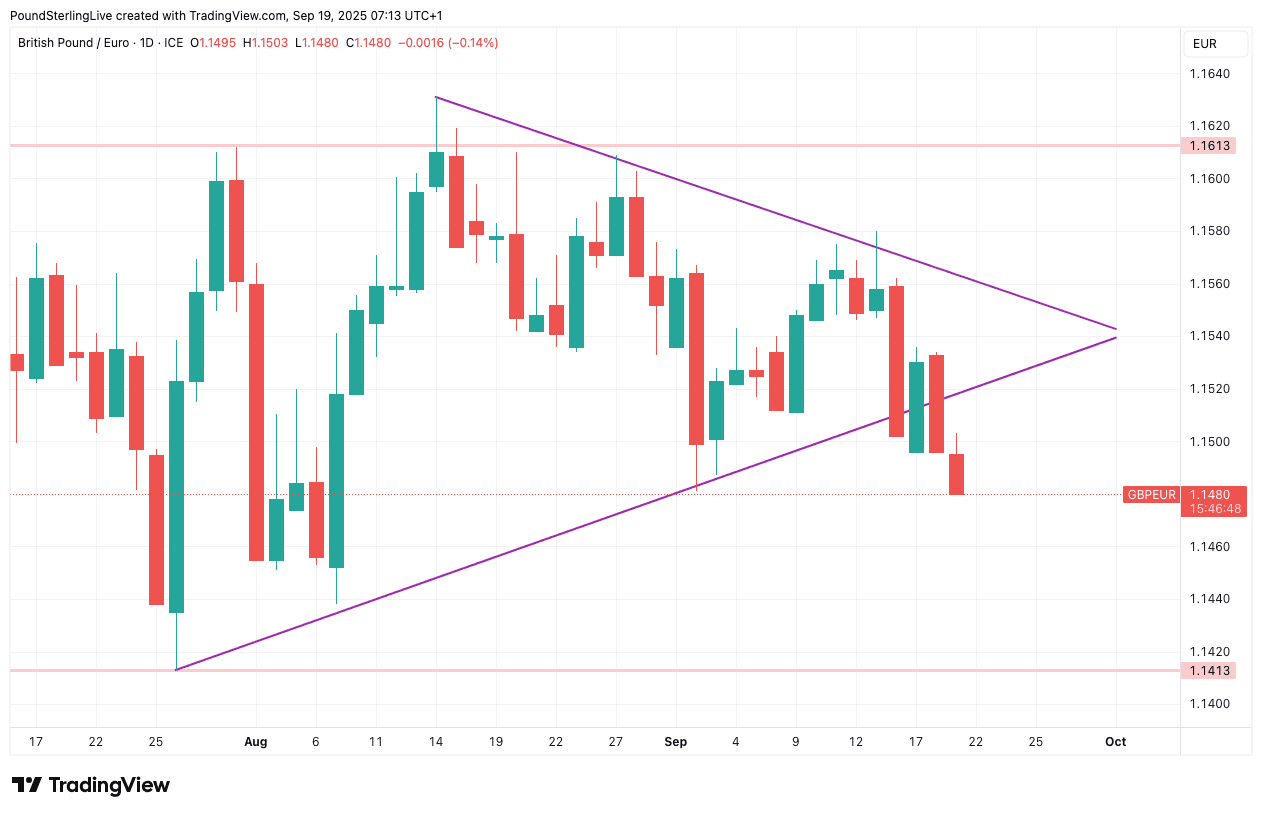

Heading into this week, we warned readers that the pound to euro exchange rate (GBP/EUR) was at an interesting technical juncture and that a breakout was imminent.

A recent period of consolidation left the pair increasingly constrained in a sideways wedge, and we saw 50-50 odds of the breakout being to the upside or the downside, depending on how the data and Bank of England decision landed.

The resolution looks to have been to the downside, with the exchange rate falling to 1.15 at the time of writing, having started the week at 1.1550. We think those with FX payment requirements should account for building risks and lock in a portion of the payment budget at current rates.

Looking back, it wasn't this week's UK inflation or jobs data that pushed GBP/EUR lower; rather it was a globally inspired surge in the euro on Tuesday which was followed by a dovish reaction to the Bank of England's policy decision and guidance.

In short, the Bank of England will likely cut interest rates again as it thinks the current pulse of inflation is nearing its end. It indicated a belief that a notable decline in wage pressure will soon have a disinflationary effect.

"For Sterling, the key implications from the Bank’s policy path rest on whether a quarterly pace of cuts is maintained at the November meeting," says FX researchers at Goldman Sachs.

Economists at Goldman Sachs think the Bank is ready to skip a November cut and will make the next advance in February.

Part of the reasoning rests with a post-decision interview given by Governor Andrew Bailey that suggested a pause to the quarterly pace of cuts the economy has thus far enjoyed is possible, in order to see how the economy unfolds.

Nevertheless, Goldman Sachs economists says the path to lower UK interest rates is intact and Bank Rate will come to rest at 3% by the end of 2026.

"We continue to think a dovish BoE repricing should still support a negative reaction in the currency," say Goldman's FX researchers.

A longer wait for the next interest rate cut could help support the pound in the near term. This is because the UK commands the joint highest base rate of the developed economies, ensuring short-term UK bonds yield greater returns to foreign investors than their peers.

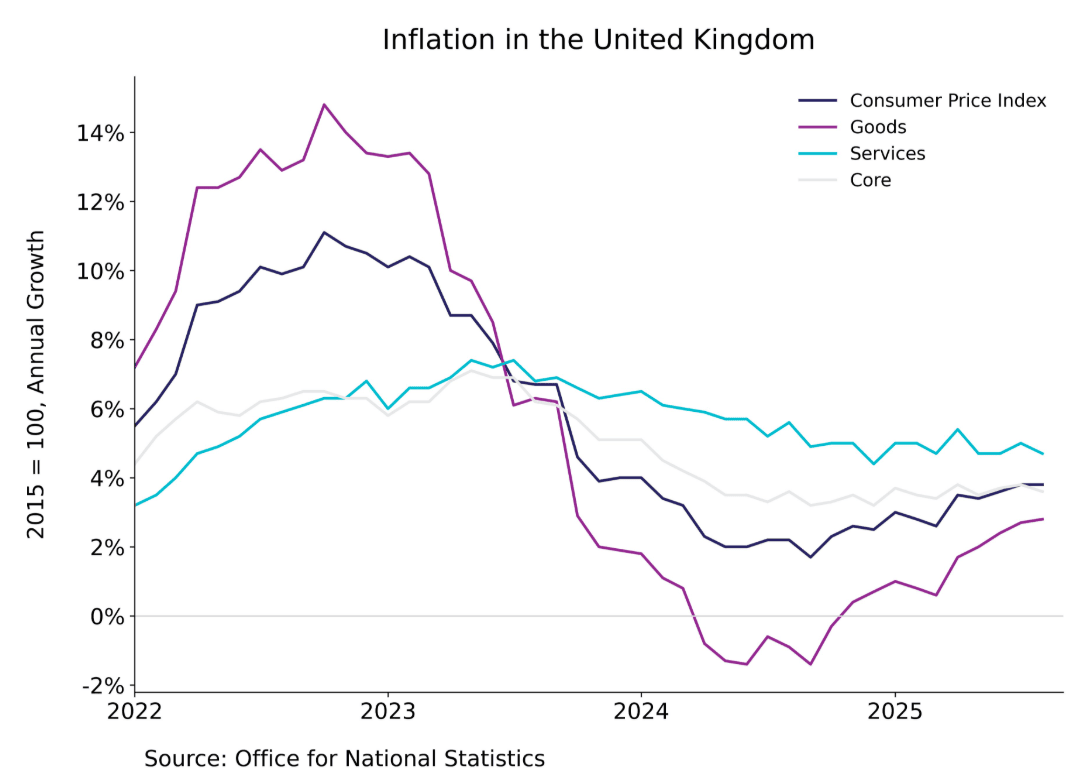

Above: UK inflation is stubbornly high.

Those seeking higher returns are therefore incentivised to snap up UK debt, creating demand for the currency.

However, Jayati Bharadwaj, Head of FX Strategy at TD Securities, reminds us that the UK budget is looming, which risks undermining any potential interest rate support Sterling might have enjoyed.

She thinks the GBP will be vulnerable to weakness against EUR in the coming weeks.

"Tactically, we see EURGBP upside heading into the UK's autumn budget in November, which can create some headwinds for GBP. It is harder to see GBPUSD downside with the USD beta and a relatively hawkish BoE stance, but easier to see relative underperformance vs EUR," says Bharadwaj.

Given the proximity of the budget to the November decision, there is a decent chance the Bank skips a November cut in favour of a December move.

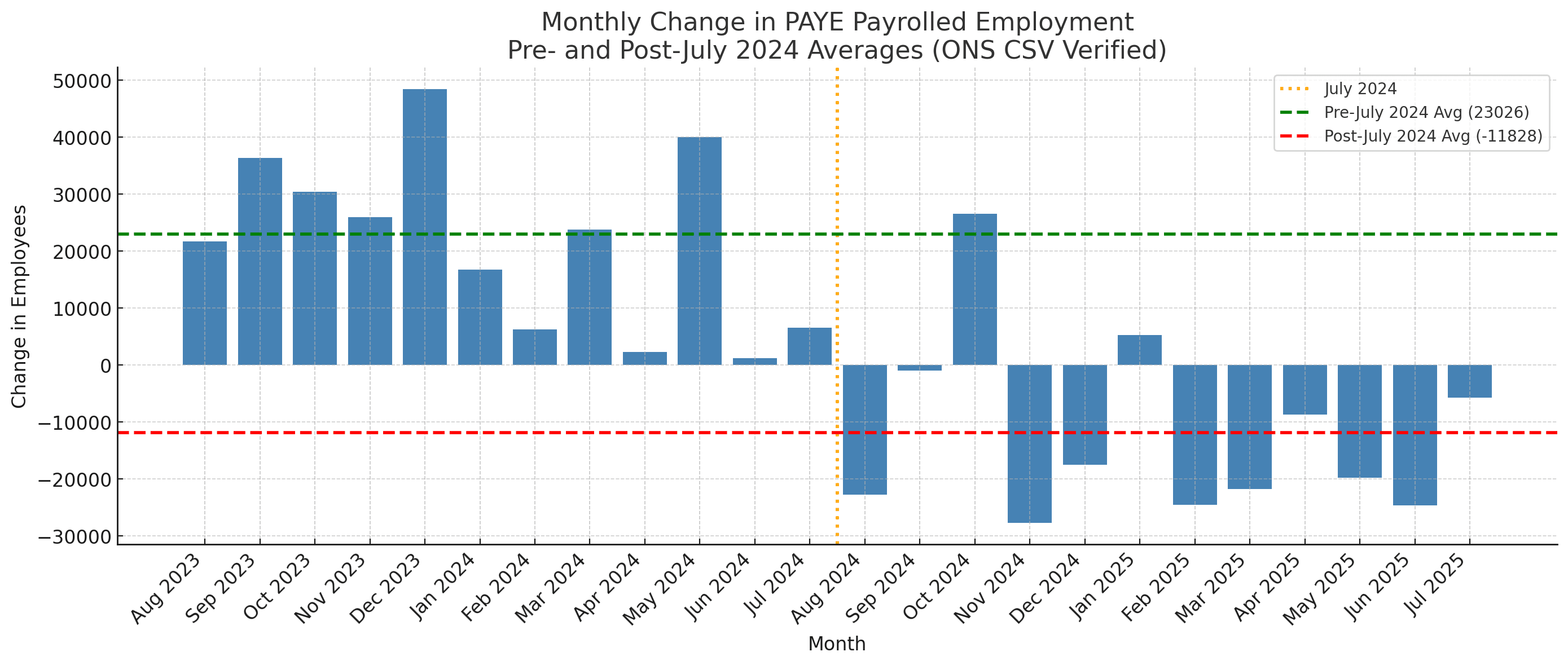

Above: There is a distinct deterioration in the labour market, which should weigh on wages, and inflation in the coming months.

"The UK faces a very sterling-unfriendly fiscal/monetary policy mix, with further fiscal tightening likely at November’s Budget and rate cuts set to follow. The Government feels the need to establish fiscal credibility but has struggled to control spending, making tax increases inevitable," says a note from Societe Generale's FX strategy team.

Soc Gen strategists told clients this week to actively position for GBP/EUR downside (by buying a variety of EUR/GBP products).

"EUR/GBP is now moving in line with its short rates differential, and our new Global Economic Outlook expects the ECB to have completed 80–90% of its easing cycle, while the BoE has only completed 50–60%. The probability of a BoE cut in November is now close to 50–50, leaving room for near-term GBP downside," says Soc Gen.

Soc Gen's FX analysts expect Sterling to be "the most vulnerable European currency." It's house forecasts show EUR/GBP gradually moving towards 0.90. (GBP/EUR down to 1.11).

The consensus amongst economists reacting to Thursday's decision is that a delay to the Bank of England's rate cutting cycle would be to absorb the contents of the November budget, opening the door to a December cut.

For FX, November or December is of little interest; what matters is that rates are going down again.

"From a policy perspective, the Bank has maintained its gradual and cautious approach. There appears to be little risk of a change in November, ahead of the Budget, but we continue to see the possibility of an adjustment in December," says Jeremy Stretch, a strategist at CIBC Capital Markets.

The GBP/EUR technical setup advocates for further losses, while an impending tax-hiking budget and further rate cuts offer a dour fundamental narrative.