Image © Adobe Images

The pound to euro exchange rate (GBP/EUR) is forecast to remain under pressure this week.

There are no major data releases, but pound sterling will keep an eye on the headlines emnating from the governing Labour Party's conference, where pressures are being put on Chancellor Rachel Reeves to boost spending and borrowing.

Reeves needs to plug an existing £30BN 'black hole' in the country's finances in the November budget, but she is being pressured to ignore the hole and boost borrowing even more as government ministers clamour for more money.

Reeves has so far resisted these calls for a more spendthrift approach to managing the country's finances, but the risk is that the pressure to break her own fiscal rules increases substantially this week.

A potential challenger to Prime Minister Sir Keir Starmer - Andy Burnham - has even called for the government to ignore the bond market, suggesting a dangerous populist move away from fiscal orthodoxy.

"GBP also lost ground to EUR... suggesting, alongside the underperformance of gilts, that UK political risks were a market driver to some extent," says a recent market note from Lloyds Bank.

With political uncertainty on the radar, we suspect the pound will struggle.

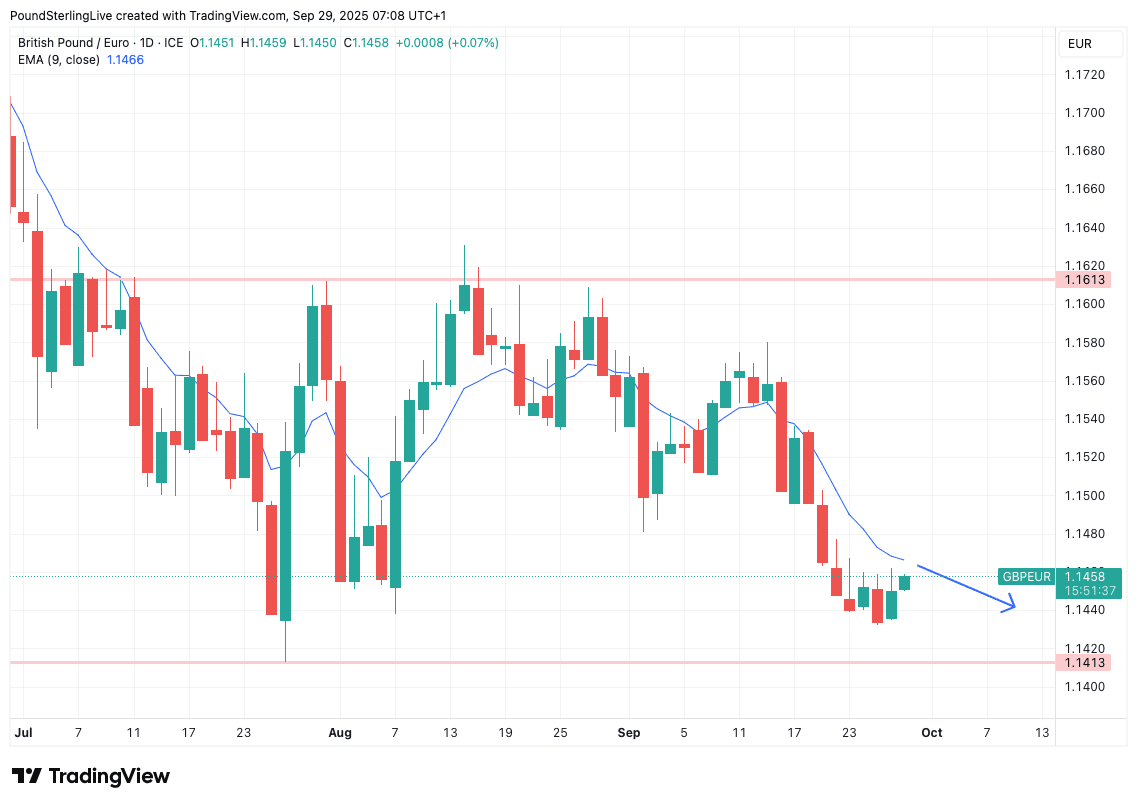

GBP/EUR vulnerability is expressed on the charts, with a host of momentum indicators indicating the easiest route forward is to the downside.

It trades well below its key moving averages, including the nine-day exponential moving average (EMA), which means our Week Ahead Forecast looks for further softness.

To be sure, a couple of tepid daily gains can't be ruled out from here, as we are at a major horizontal support zone:

The chart shows horizontal graphical support coming in at 1.1413. This markets the lower-bound of the summer range in GBP/EUR; however, we would suggest that the support actually starts around 1.1460, which suggests we are in a zone of treacle-like support that is propping Sterling up.

Nevertheless, a drift to 1.1413 is our preferred expectation for the coming days at this point.

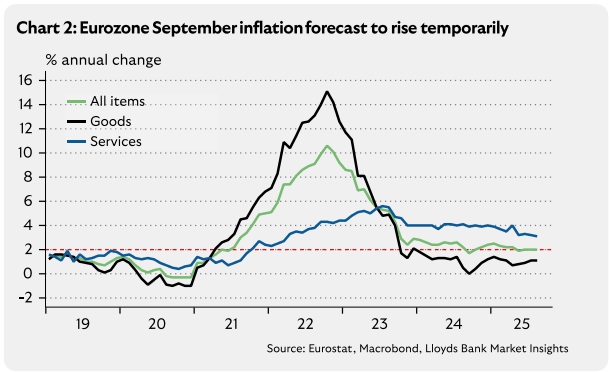

The euro has some inflation data to look forward to as national inflation figures are released, which should form an opinion about the Eurozone-wide release.

Germany, France and Italy report ahead of the Eurostat flash estimate on Wednesday.

Eurozone headline inflation is expected to rise to 2.3% from 2.0% in August, driven by petrol base effects.

Core inflation is expected to rise to 2.4%.

Such an outcome gives the European Central Bank (ECB) to retain a cautious approach to interest rates, underpinning market expectations that it has finished the rate cutting cycle.

If the data undershoots, then the euro can come under pressure. If it overshoots, the euro can strengthen.

The ECB's committment to holding interest rates contrasts with the Bank of England, which is likely to cut interest rates once more in 2025 and then again on a couple of occasions next year.

If so, UK bond yields will fall faster than those in the Eurozone, which will weigh on the pound.

This contrast in central bank policy is why numerous currency analysts we follow anticipate GBP/EUR underperformance.