Image © Adobe Images

A turbulent week ends with across-the-board gains for the British pound.

Pound sterling's Friday recovery grew in confidence after it was reported that the UK's economy grew comfortably in January.

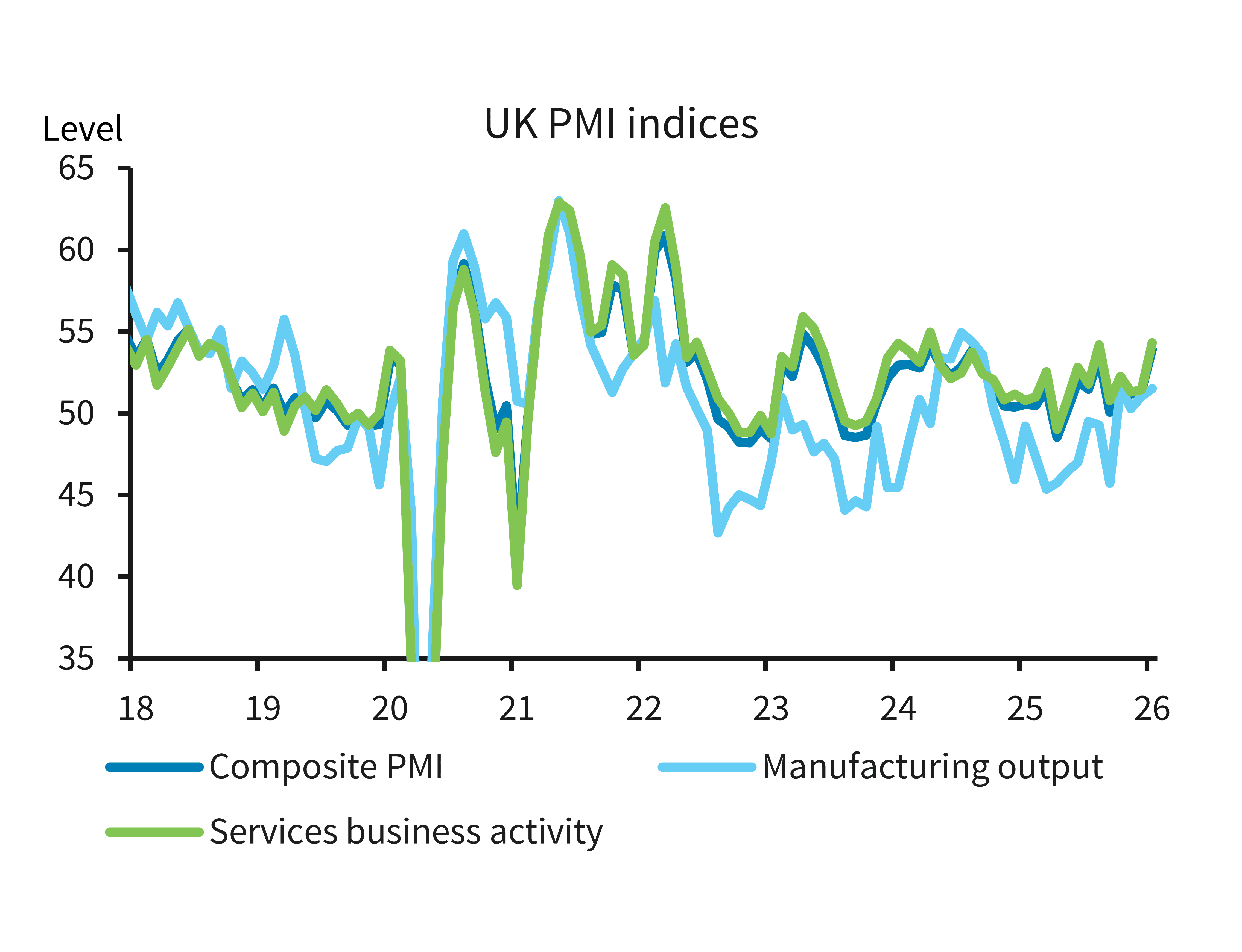

S&P Global's PMI survey of the private sector economy exceeded market expectations with all three components coming in above 50, which is the level that marks the boundary between growth and contraction:

○ Manufacturing: 51.6 vs. 50.6 exp. (prior 50.6)

○ Services: 54.3 vs. 51.7 exp. (prior 51.4)

○ Composite: 53.9 vs. 51.5 exp. (prior 51.4)

There was a discernible reaction in key GBP pairs following the release as investors judged these figures would ensure the Bank of England holds interest rates next month.

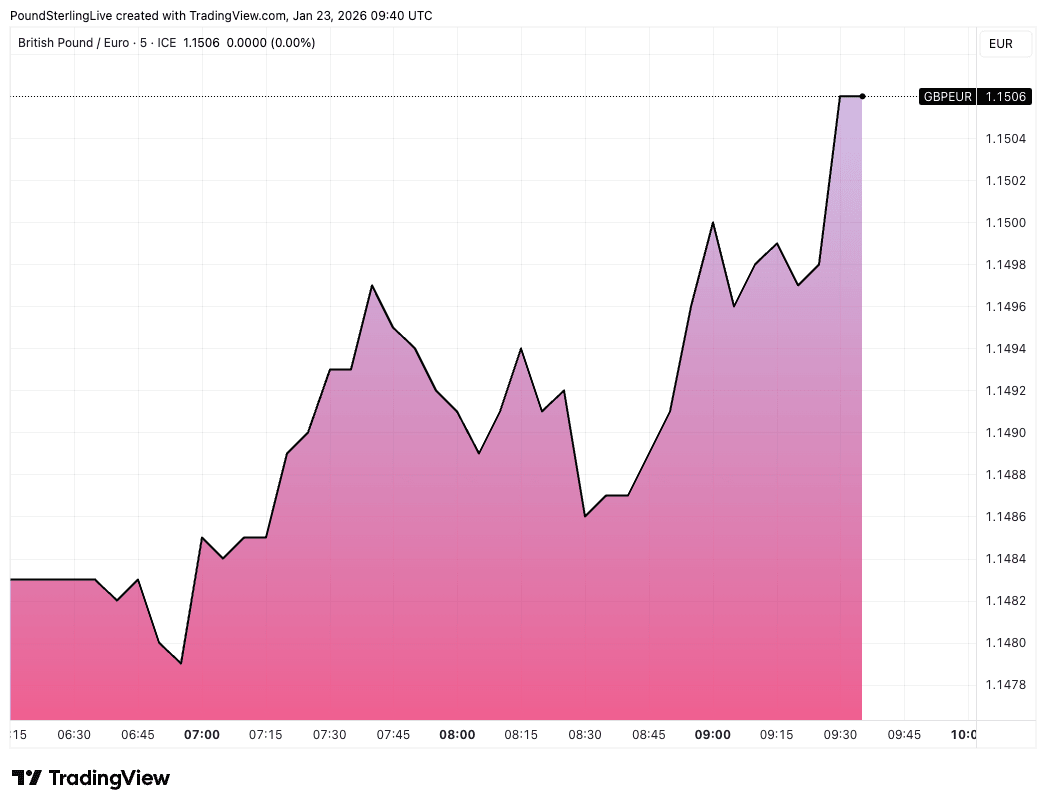

The pound to euro exchange rate (GBP/EUR) cleared 1.15 and built on earlier gains that followed the release of a consensus-beating set of retail sales figures. The pound to dollar exchange rate rose to 1.3529, putting it on course to register a +1.0% gain for the week.

Above: GBP/EUR price action on Friday.

Just 30 minutes earlier, the Eurozone's PMI data were released, and they disappointed against expectations. The contrasting outcomes create a clear wedge in fortunes that compels GBP/EUR higher.

To be sure, it's been a bruising week for the pound against many of its G10 compatriots (it's still down on the week against most), but it heads into the weekend with some welcome fundamental developments that put wind in its sails.

S&P Global said their January PMI survey showed UK private sector companies experienced a solid increase in output levels at the start of 2026, with the overall rate of expansion reaching its fastest for just under two years.

"Importantly, the closely watched PMIs bounced strongly to start the year with private sector growth at a 21-month high. Growth looks poised to bounce by around 0.5% q/q," says Sanjay Raja, Chief UK Economist at Deutsche Bank.

January data also signalled a sustained improvement in new order intakes across the private sector economy that bodes well for entum to sustain through Q1.

"While growth continues to be driven by the service sector, and in particular financial services and tech, the manufacturing sector is also continuing to report a gathering recovery," says Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

Image courtesy of Barclays.

The news on inflationary pressures was also particularly noticeable: strong input cost inflation persisted resulted in the greatest increase in average prices charged by private sector firms since August 2025.

These data effectively put to rest expectations for a February rate cut at the Bank of England and will raise questions as to whether the Bank can get away with more than one cut this year.

"With prices looking stickier on forward-looking data... the risk now is for a slowdown in the pace of rate cuts - including a possible Q1-26 skip," says Deutsche Bank's Raja.

As markets pare bets for further cuts, UK short-term bond yields consolidate at higher levels which fundamentally offers GBP/EUR support, all else equal.

"High staffing costs were meanwhile again widely reported as a key cause of higher selling prices, hinting at an intensification of price pressures at a level above the Bank of England target," says Williamson.