File image of ECB President Christine Lagarde. Image: Andreas Reeg/ECB.

The pound advances against the euro amidst a decline in Eurozone bond yields as markets pull back expectations for ECB rate hikes on rising hopes that the Iran war will soon be settled.

The euro has steadily fallen against the British pound as markets pare expectations for ECB rate hikes in the coming months, with an intervention by ECB President Christine Lagarde proving decisive.

Lagarde said on Tuesday the euro area economy has moved away from the ECB's Iran-war baseline, but not enough yet to justify leaning toward rate hikes, noting that "we are in between the baseline and the adverse" scenario.

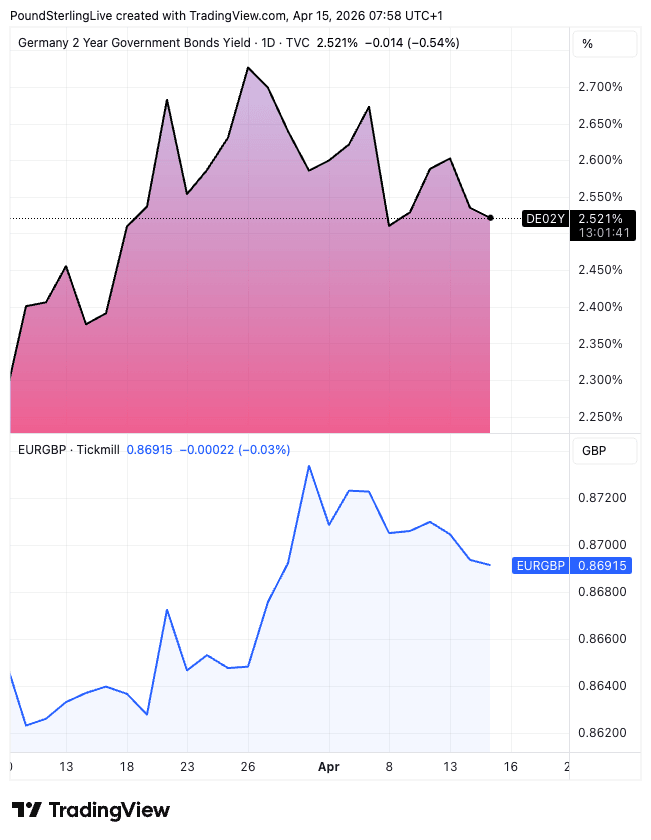

The market had steadily raised bets that the ECB would respond to the war by raising interest rates in the coming months, which has aided the euro to some degree. But Lagarde is clearly trying to caution against that assumption. Her tone helped prompt a shift lower in area bond yields with Germany's 2-year bond falling 2.50% on Tuesday.

"The pullback in oil prices, together with comments from C. Lagarde, helped bring down ECB tightening expectations, with the market now pricing just over two rate hikes for this year. The 2Y Schatz yield fell by about 10bp to 2.54%... The 10Y Bund yield dropped 7bp, returning close to 3%," says a note from Natixis, the French investment bank.

As the chart shows, that move in bond yields is correlating quite strongly with EUR/GBP at the present time, suggesting to us that central bank interest rate expectations could be helping GBP strengthen against the euro in the short term:

April has seen the pound steadily recover the losses it experienced against the euro in the second half of March. That recovery in GBP - and the fall in central bank rate hike bets that we have mentioned - are linked to hopes that oil will soon start flowing out of the Middle East once more.

"With the global energy shock taking centre stage, EUR/GBP price action has instead been dictated by risk and terms of trade impulses," says a weekly FX research note from Goldman Sachs.

It's expected that Iran and the U.S. will be back at the negotiating table within days, keeping alive the prospect of an eventual deal to unlock energy flows in the coming weeks.

The scent of a deal should be enough to keep oil price gains in check - albeit at high levels - and prompt further gains in the perennially optimistic stock markets.

The dollar is in retreat and GBP/USD is now higher than it was in the days leading to the Iran war.

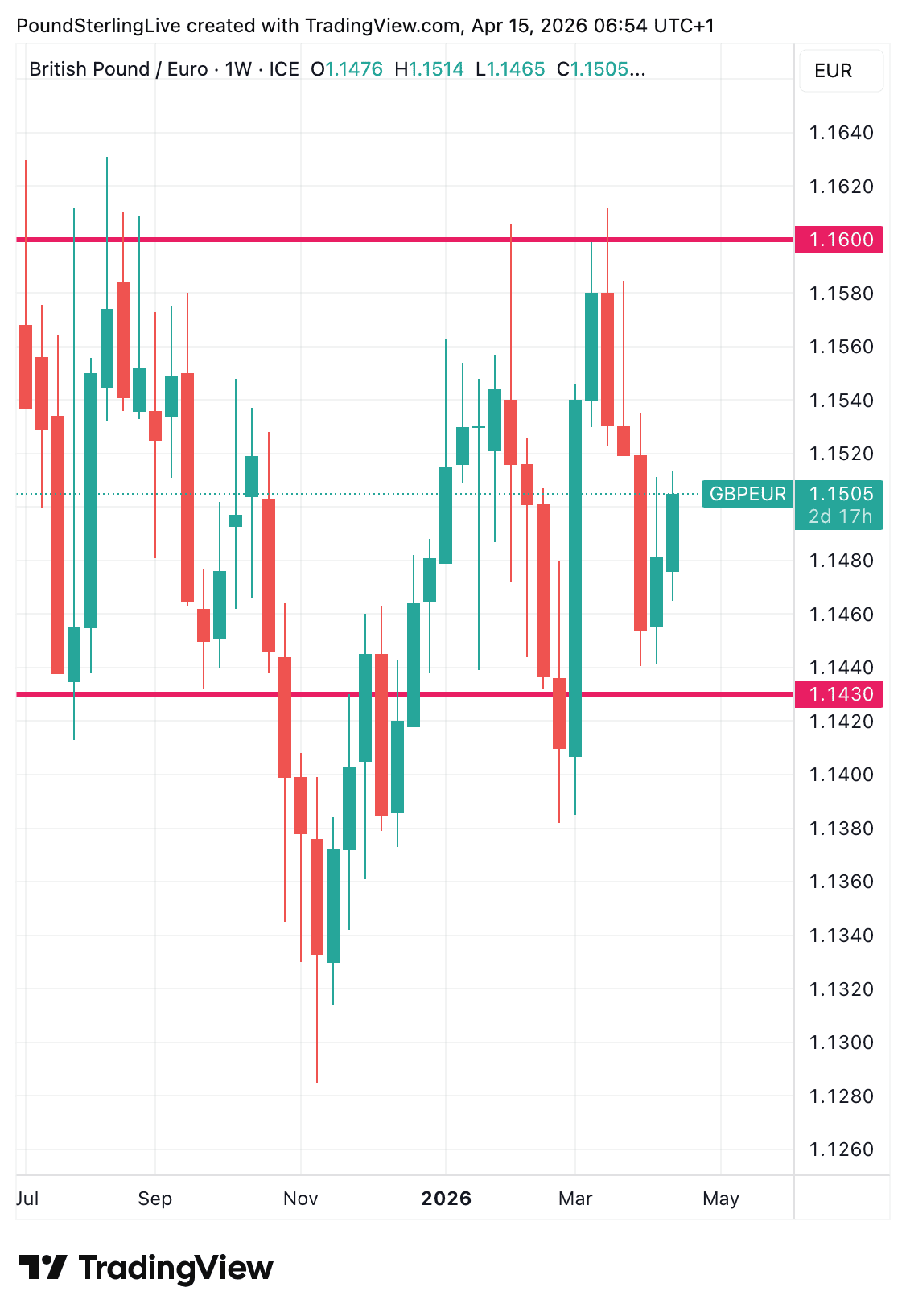

Although GBP/USD is making noticeable gains, owing to the broader USD pullback, GBP/EUR is more muted, having only risen from 1.1440 to 1.1500 in the past two weeks.

GBP/EUR is the better indicator of sterling-specific sentiment, which is hardly bullish for pound sterling.

As the war de-escalates, investors can return focus to domestic issues facing the pound: a reset higher in energy prices, falling employment, uncomfortably high public finances and rising political uncertainty into May's local elections.

"Some of the UK-specific themes potentially drifting back into focus in the medium-term. This includes the May local elections, which are now under a month away, and in our view present an asymmetric risk of bouts of Sterling downside on a return of the type of political uncertainties that were a key feature for the currency earlier this year," says Goldman Sachs.

Growth headwinds are a challenge and were highlighted by the IMF's latest quarterly economic forecasts: they show the UK economy will suffer the biggest hit from the war of the G7 and a period of stagflation will ensue.

The IMF highlighted specific reasons why the UK is more exposed than its peers.

Energy Import Dependence: As a net importer of energy owing to perverse political policies, the UK is highly sensitive to rapid price rises in gas and oil.

Fiscal Constraints: The IMF said the UK has "much less room to move" and urged the government to be "very cautious" about new support spending.

Unemployment: The jobless rate is projected to rise to 5.6% in 2026.

Despite the headwinds, GBP/EUR looks relatively comfortable around 1.15, which is more or less the middle of a long-running range that has been in place since last year.

We're hovering around the 100- and 200-day moving averages at the current time, which confirms there is some longer-term equilibrium around these levels and that valuation can anchor the exchange rate in the short-term.

Gains towards 1.1550, or even 1.16 are possible in the coming days but we wouldn't place too much hope on a move to the upper band.

Just as likely as a test of 1.16 is a repeat of 1.1440.

"We believe GBP is still exceptionally sensitive to any re-escalation of geopolitical tensions," says Sarah Ying, analyst at CIBC Capital Markets, in a recent note that warns rising energy costs will negatively impact the economy today, and in the coming months.

"The balance of risks favours being long EUR/GBP, and we believe the pair can retest 0.8742 into the coming week," says Ying.

EUR/GBP at 0.8742 gives GBP/EUR at 1.1440, which is the March low and approximate start of the long-term range lows.