Image © Adobe Images

Currency markets are priced for calm at precisely the moment the risks to volatility are increasing.

Currency markets are incredibly subdued as the major drivers of the FX markets are unusually balanced, leading exchange rates to respect ageing and well-worn ranges, many of which have been in place for more than a year.

"G10 FX volatility has kept trending lower across the board, with many implieds reaching their lowest levels in years, as spot rates have remained stuck in the same sorts of ranges," says Alexandre Dolci, FX Strategist at Crédit Agricole.

For corporates, importers, exporters and investors, this means FX hedging is relatively inexpensive.

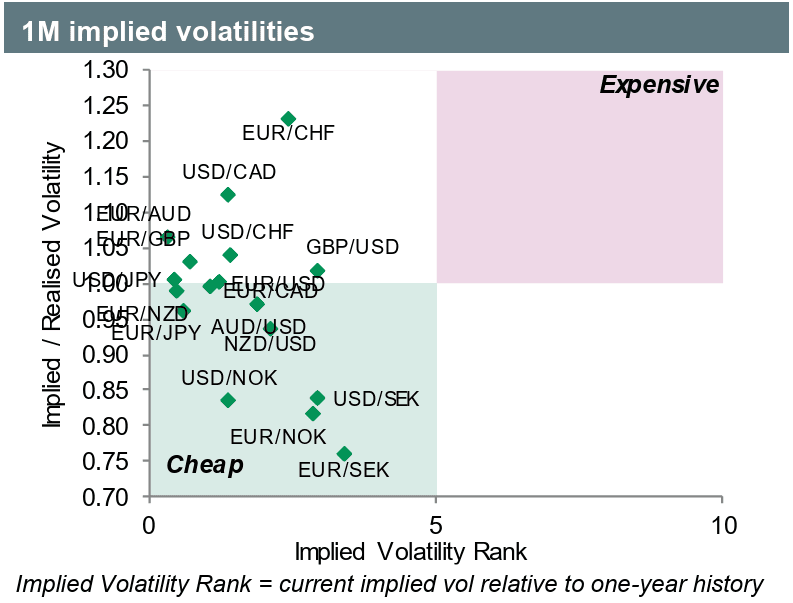

Image courtesy of Crédit Agricole.

Examples of subdued volatility in the GBP universe include GBP/CAD, which is respecting a sideways range that's been in place since February last year.

GBP/EUR has been well behaved between 1.15 and 1.16 for most of the year; casting back to 2025 shows the contours of the current range were actually first noted in July.

"Years could actually be decades for EUR/GBP vols, as ATM from 3M to 1Y have actually fallen to their lowest level since 2007," says Alexandre Dolci, FX Strategist at Crédit Agricole.

That's the market effectively saying: "we don’t think EUR/GBP is going anywhere."

History suggests such confidence is often dangerous.

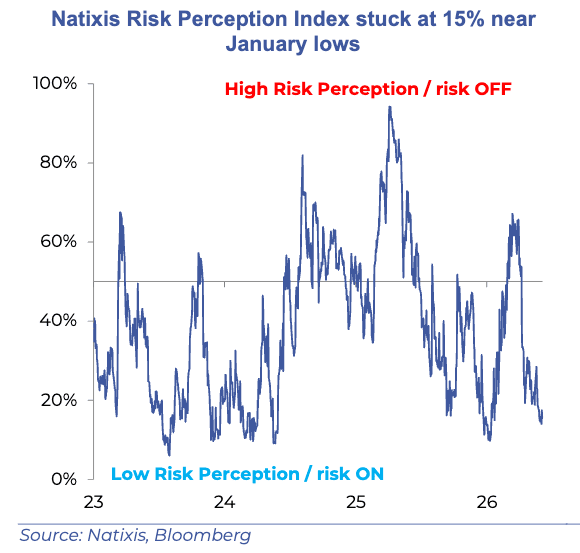

"Low levels of implied volatility everywhere look like complacency. We think it might not be a bad time to tactically hedge equity risk," says Emilie Tetard, an analyst at Natixis.

The current setup resembles the summer of 2007 before the credit crisis, early 2017 before major Brexit repricing and late 2019 before Covid.

Periods of very low volatility are often followed by sharp bursts of volatility, not because something terrible has happened, but because markets become positioned for nothing happening.

Absent major shocks, central banks are most likely candidates to play a role in any pickup in volatility in the near term.

Tetard says the Fed and rates are the other main current concern for risk assets right now, as growth stocks and AI investment are highly sensitive to interest rates

"The outcomes of the next ECB and Fed meetings may carry greater uncertainties than in recent months, which is not necessarily evident when looking at money markets," says Dolci.

The ECB is set to raise interest rates next week, while the Federal Reserve will likely drop its easing bias a week later as global central banks pivot to fighting an uptick in inflation triggered by the Iran war.

AI Trade Runs Red Hot

Concerns also centre around the incredible rally in technology stocks as the AI bull run spreads outwards from the early AI leaders into the wider stock market.

Blockbuster IPOs and huge cash raises by the likes of Alphabet are also signalling an extremely hot market.

"The AI narrative is at full speed with the forthcoming mega IPOs (SpaceX on June 12th, Anthropic and OpenAI), equity fund raising (Google) and the tension between realized fast-growing earnings, the AI-theme ongoing diffusion (across region and supply chains) and exuberance risk," says Tetard.

A combination of AI-related equity exuberance, major IPOs, uncertain Fed and ECB decisions and exceptionally low volatility pricing creates the conditions where a relatively small surprise could produce a disproportionately large move in equities, bonds and currencies.

How Would the Pound Fare In a Vol Pick-up

Volatility is incredibly subdued, even if there are risks aplenty.

The rulebook suggests that when volatility rises the dollar, franc and yen would tend to benefit.

The pound would typically fall against those currencies, as well as the euro.

It would likely gain against the Scandinavian names and the commodity dollars of Australia and New Zealand.