Above: Christine Lagarde. Image by Dominique HOMMEL. © European Union - Source: EP

It's not hard to see euro downside risks materialising as the ECB fails to deliver on market expectations.

Markets want more than just today's cut, they are positioned for two more recutions this year and aren't anticipating rate cuts in 2027.

This pricing will be challenged in the coming months and for the euro, that's a headind

First Cut in Three Years

the euro was higher against the pound but lower against the dollar, confirming a mixed FX reaction to the European Central Bank's June policy decision, where it raised rates for the first time in three years in response to inflationary pressures.

The decision was expected, as was an uplift to internal inflation projections that show inflation climbing to 3.0% in 2026 and 2.3% in 2027, from 2.3% and 2.2% previously.

This hike is the ECB looking to get ahead of inflation, something it was slow to do following the 2022 inflation shock caused by Russia's invasion of Ukraine.

Those new inflation projections suggest a shock that will be of a far smaller magnitude than that of 2022; importantly, the prospect of a strong inflation pass-through is far lower owing to a different set of circumstances.

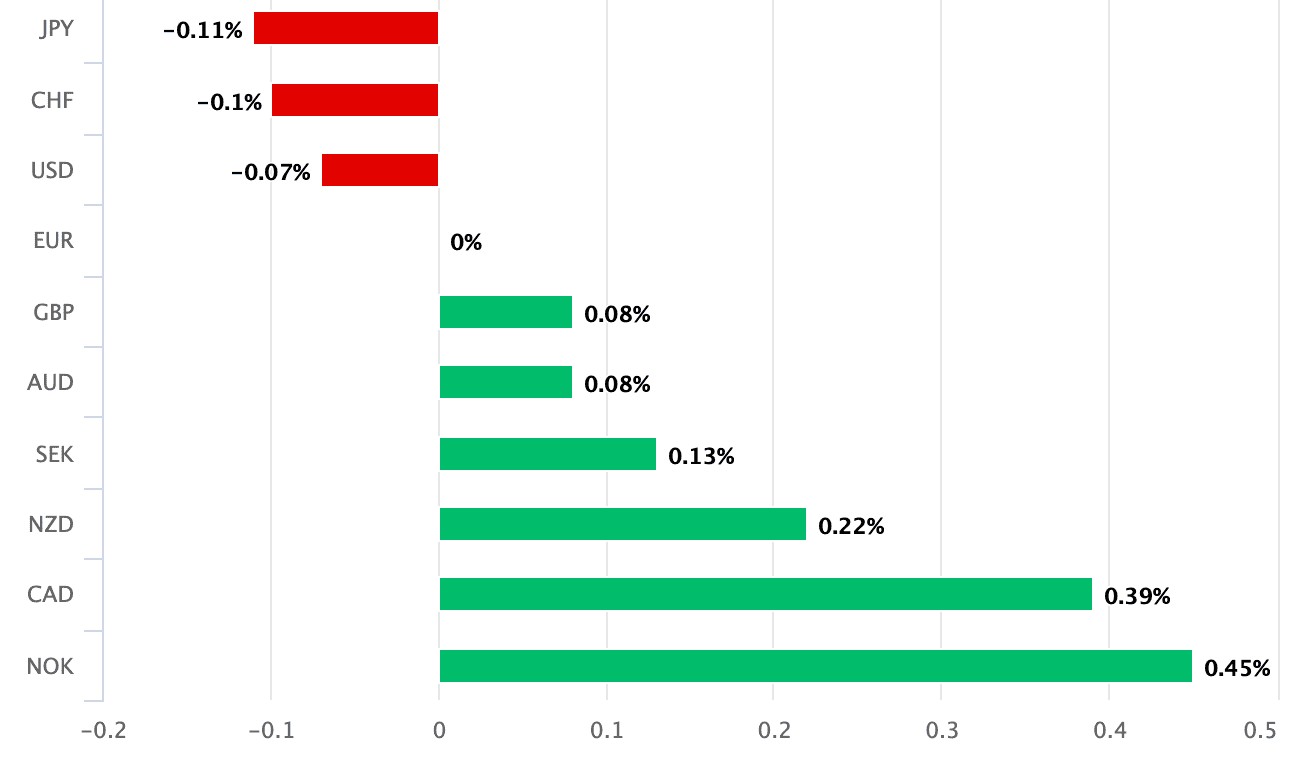

Above: EUR is mixed on the day.

This time is different because the Eurozone economy has more 'slack' to absorb before inflation really snowballs: growth projections were revised down to 0.8% in 2026 and 1.2% in 2027 from 0.9% and 1.3% previously.

The anticipated growth slowdown is a significant disinflationary development to contend with and raises questions about the ability of the ECB to hit the market's elevated expectations for future rate hikes.

"The ECB is saying that a ‘look through’ strategy is not a robust response. The question is how far can this tightening cycle go? Not far, is our answer. There is upside risk to inflation, but there is also downside risk to growth. One more hike in September and that’s it," says Mark Wall, Economist at Deutsche Bank.

Two More Hikes is a Big Ask

Markets entered the day expecting two further hikes this year, a pricing that needed to be maintained in the coming weeks if euro exchange rates are to remain steady near current levels.

"Expectations of the ECB remain ambitious, despite a correction in recent weeks. Even if the ECB were prepared to raise interest rates three times this year, Christine Lagarde is unlikely to commit to that today," says Michael Pfister, FX Analyst at Commerzbank.

Lagarde was understandably non-committal on what will be done next, warning risks to growth were lower, but risks to inflation were higher. Equally contradictory was the warning risks to wages were to the downside, but that firms were ready to raise prices.

"I think they're hoping that we end the day with pricing close to two than three... I think they're comfortable with two hikes; not three, at this point," says Claus Vistesen, analyst at Pantheon Macroeconomics.

As incoming data confirms the slowdown and the shock proves smaller than in 2022, market pricing will drift from two more hikes toward one, and the rate premium currently supporting the euro gets repriced out.

Downside Risks for Euro Crystallising

For the euro, there's nothing dramatic on the day; but a slow erosion of the currency rate support lies ahead.

"The balance of risks are stacking up against the EUR," says Daragh Maher, Senior FX Strategist at HSBC.

HSBC's economists think that the market is underappreciating the prospect that the ECB starts cutting again in 2027 as the effects of the Iran war rapidly fade out of the inflation basket.

That's a pricing that's underappreciated by the market says Maher: "The medium-term monetary-fiscal mix looks less supportive than the market assumes... downside risks to EUR-USD may be crystallising."