Above: A shopper in a Berlin store. Image © Adobe Images

Euro exchange rates eased ahead of the weekend following weak German state inflation, jobs and retail sales data.

German CPI and retail sales data have been rolling in through the course of Friday, and the headline is that a significant disinflationary trend is building in Europe's largest economy.

The Consumer Price Index fell to -0.2% month-on-month in January from 0.5% in December, undershooting expectations for 0.1% growth. The annual measures fell from 2.6% year-on-year to 2.3%, which is less than the 2.6% that was expected.

"For the ECB doves, today’s German inflation data is good news as it paves the way for more rate cuts to come," says Carsten Brzeski, Global Head of Macro at ING Bank.

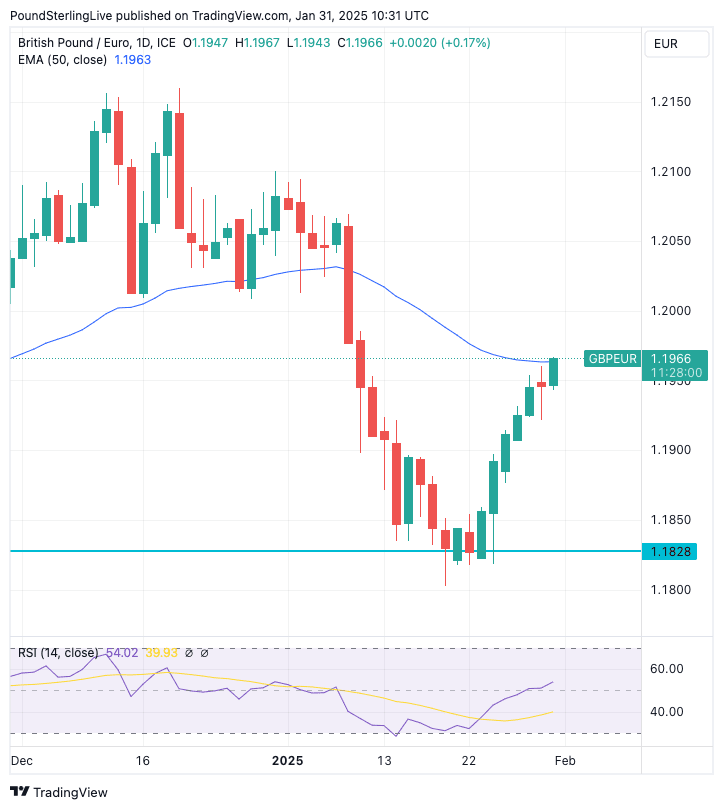

Following the data, the Pound to Euro exchange rate rose to 1.1964, its highest value in three weeks. The Euro is down for a fourth consecutive day against the Dollar at $1.0383.

Employment in January disappointed, coming in at 11.0k jobs vs. consensus of 15.0k. The unemployment rate came in a tick higher than consensus at 6.2%, the highest since 2021.

"The number of those unemployed in Germany reached a 10-year high in January, not only showing that hopes of a consumption revival this year might have been overdone, but also boding well for more disinflationary pressures later this year," says Brzeski.

Retail sales slumped to -1.6% month-on-month in December, down from -0.1% in November and significantly undershooting expectations for growth of 0.2%.

This speaks of a notable fall in domestic demand, which economists say would be expected to weigh on inflation.

Above: GBPEUR recovery sequence intact.

The ECB cut interest rates again on January 30 and indicated more cuts were likely as it believed the disinflation process was intact.

These data would confirm this and underpin the expectation that the ECB will cut interest rates faster and further than the Bank of England.

This naturally implies an upside for the Pound to Euro exchange rate and means the current recovery can extend back towards late-2024 highs.