Image © Adobe Images

Fade Pound Sterling weakness as the Bank of England's policy stance remains as 'hawkish' as ever, despite Thursday's seemingly contradictory signals.

The Pound to Euro exchange rate dropped by as much as half a per cent on the day the Bank of England cut Bank Rate by 25 basis points, slashed growth forecasts, and two Monetary Policy Committee (MPC) members voted for a much bigger 50bp cut.

What got tongues wagging was the switch of MPC member Catherine Mann to vote for a 50 basis point cut. She has been a staunch 'hawk', often resisting the urge to cut or voting for a 50 basis point hike when others were voting for a more modest 25bp hike.

This prompted a slight rerating in interest rate expectations, and the market has now moved to price in three further rate cuts this year.

But the FX market reaction was more exciting. The Pound-Euro fell to a low of 1.1940 on the day and Sterling was lower against all its peers, with losses against the Dollar extending to over a per cent at one point.

However, the scale of the FX move outpaces the scale of the move in interest rate markets, which is the first sign the Pound can recover further.

The halving of growth forecasts underpins Mann's thinking and dominates financial news headlines on Friday; no wonder the decision was considered a 'dovish' one.

But the dovish assessment runs skin deep. Despite the surprise of the vote split and the GDP cut, there is overwhelming evidence the Bank will retain its cautious approach, which will underpin the Pound.

"EUR/GBP moved higher on the announcement with the dovish vote split taking centre stage," says

Kirstine Kundby-Nielsen, an analyst at Danske Bank. However, "the still cautious guidance delivered today highlights the more gradual approach of the BoE compared to European peers," she adds.

Given this, Danske Bank strategists predict Pound-Euro will move higher in the coming quarters driven by a relatively hawkish Bank of England and a growth pickup in the UK relative to the euro area in 2025.

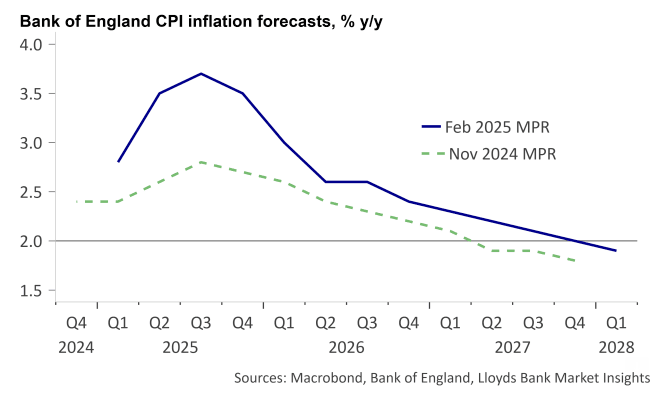

The most prominent 'hawkish' development is the jacking up of UK inflation forecasts in 2025 to a peak of 3.7% in the third quarter of this year. This is up from November's forecast for a rise to 2.8% in Q3.

The projections show inflation will suddenly drop to 'target' from 2026 onwards, but what confidence do the Bank's forecasters have that this will happen given the inherent difficulty of forecasting at longer-term timeframes?

Image courtesy of Lloyds Bank.

Most of the MPC are aware of the counter-intuitive and confusing message that would be sent by accelerating rate cuts into rising inflation. The MPC deploys a forecasting framework that is based on three scenarios it thinks will evolve, and the minutes show scenarios two and three are now favoured.

These scenarios mean most MPC think interest rates will continue to fall at their current pace or even slower.

The statement itself reinforced this, stating that rate cuts would be "gradual", that rates need to remain "restrictive for sufficiently long", and that it would be "careful" when considering further cuts.

The more we look into the details of the day, the more we see that this was as 'hawkish' an event as any.

For the Pound, this means that any weakness from the decision itself should be faded. In fact, the outlook could become a whole lot more hawkish if inflation starts to beat expectations, which is what numerous economic surveys are signalling at the start of the year.

"We remain convinced that the BoE will have to stop cutting interest rates earlier than most expect amid strengthening inflation," says Andrew Wishart, Senior UK Economist at Berenberg Bank.

"We have been here before," he adds:

Just over a year ago, investors priced in a fall in bank rate to 3.25% by end-2025. The resulting drop in fixed interest rates available to companies and households helped drive a pick-up in GDP and pay growth that delayed the first cut until August.

"A boost to demand from rate cuts at the same time as firms are facing a large increase in costs that they are keen to pass on will push up inflation to well over 3% yoy in the second half of the year. The BoE will find it difficult to justify further loosening in that environment," says Wishart.