Image © Adobe Images

The Pound-to-Euro exchange rate is expected to trend towards a new three-year high in the coming months amidst ongoing support from elevated UK interest rates.

However, progress to this level might be slow as money markets show investors are cooling bets for further interest rate cuts in the Eurozone.

Overnight indexed swaps, a measure of where investors think central bank interest rates will travel, show expectations for just two more interest rate cuts at the Bank of England this year.

Just two weeks ago, the expectation was closer to four, confirming a repricing in expectations has occurred that has bolstered the Pound, resulting in GBP/EUR rising from January lows of 1.18 to 1.2090 on Wednesday.

"Recent high inflation means rate-setters have to be more cautious now," says Rob Wood, UK Economist at Pantheon Macroeconomics.

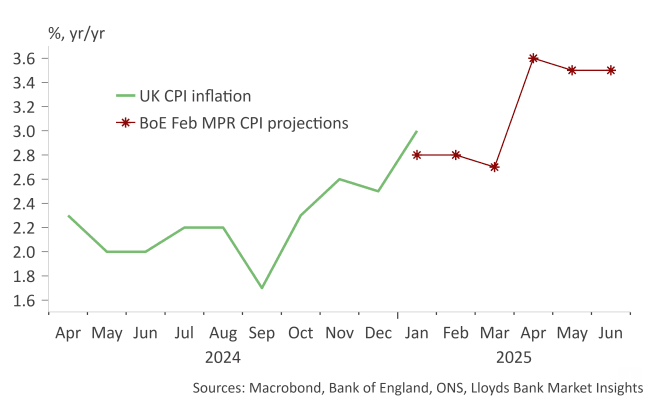

UK data this week has confirmed the Bank of England is right to maintain a cautious approach to interest rates, with inflation unexpectedly rising to 3.0%, beating estimates for a climb to 2.8%.

February's policy decision at the Bank of England confirmed that rate-setters were more inclined to continue at a pace of four cuts a year or once a quarter.

Money markets now show this is too fast, confirming investors think the Bank will have to capitulate in the face of rising inflation.

Wood says economic surveys suggest "underlying disinflation is over as firms pass wage costs on to prices, making a 4% inflation print later this year quite plausible."

Economists are increasingly of the view inflation is on course for 4.0%, citing rising fuel prices, goods prices and services costs linked to the government's tax hikes and minimum wage increases due to come into place in April.

"Many firms likely to pass on cost increases in the first half of the year," says Sanjay Raja, Chief UK Economist at Deutsche Bank. "While there remains significant uncertainty around the path of energy prices, we see CPI reaching a peak of 4.25% over the summer before making its descent back to target in 2026."

Above: January's inflation outturn means the Bank of England is already underestimating the path of inflation. Image courtesy of Lloyds Bank.

Pantheon Macroeconomics expects only two more rate cuts in 2025, which would be in keeping with existing market structures, while others see just one further cut.

For the Pound, this would imply ongoing support as rate expectations tighten further.

"We expect the pound sterling to remain robust short term as the UK’s rate advantage over European peers rises," says David Alexander Meier, Economic Research analyst at Julius Baer.

Julius Baer thinks the Bank of England will likely remain cautious, holding rates in March. "The BoE's slow pace of cuts will temporarily widen the pound's interest rate advantage," explains Meier.

The Swiss bank sticks to its short-term optimistic outlook on the pound with a 3-month target of EUR/GBP 0.82, with strength likely to fade as the rate advantage narrows later this year.

This translates into a GBP/EUR equation of 1.22.

Above: File image of ECB Board Member Isabel Schnabel Image © European Central Bank

Whether or not the Pound-Euro exchange rate can extend to 1.22 could also depend on what happens with European interest rates.

If the European Central Bank (ECB) resists cutting interest rates as fast and far as markets expect, the interest rate differential between the UK and Eurozone will shrink, potentially pressuring GBP/EUR lower.

Markets were alerted for such an eventuality by prominent ECB board member Isabel Schnabel, who said midweek that it might pause or even stop interest rate cuts.

The ECB has cut rates five times since June as policymakers worried about slow eurozone economic growth, but concerns about inflation have returned with a trade war on the horizon.

"We are getting closer to the point where we may have to pause or halt our rate cuts," Schnabel told the Financial Times.

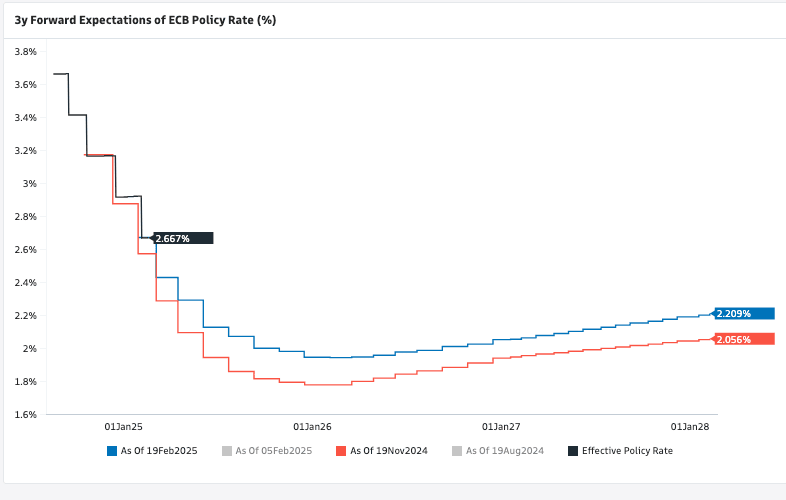

Above: Market expectations for the depth of ECB rate cuts have reached a nadir and are climbing again.

"We need to start that discussion," she added, "we can no longer say with confidence that our monetary policy is still restrictive."

The comments prompted a recalibration of bets on money markets about how swiftly the ECB could cut interest rates.

The reduction in expectations for Eurozone rate cuts came alongside similar moves for the UK, which maintained the interest rate differential, explaining why the GBP/EUR exchange rate didn't jump higher in the wake of Wednesday's surprisingly strong inflation release.

The ECB’s main policy rate now stands at 2.75%, down from 4% in September 2023, and traders expect at least two more cuts this year, with an 88% chance of a third.

There is still further scope for that third cut to be priced out, meaning greater scope for a 'hawkish' adjustment in Euro rates than UK rates. This can potentially cap GBP/EUR upside or at least ensure the climb higher is a slow one.