Image © European Central Bank

Pound Sterling starts the new week in the red against the Euro; however, the near-term outlook remains constructive, and another weekly gain is possible as tariff risks are high and a European Central Bank rate decision is due.

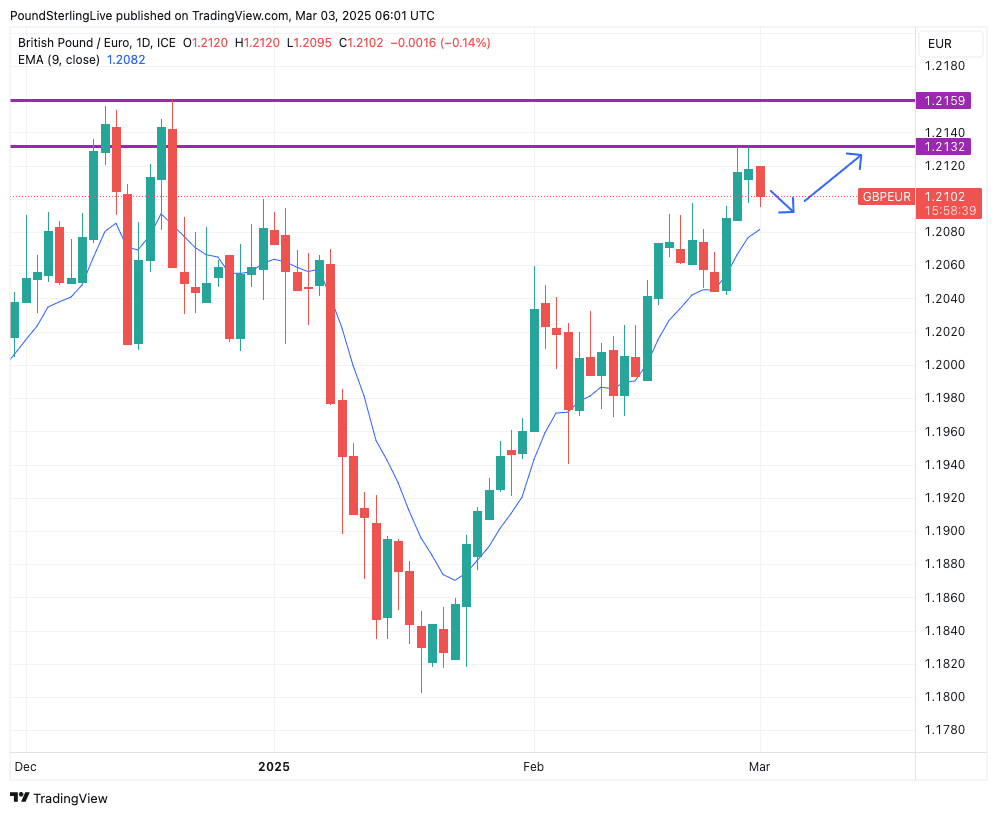

Last week's 0.36% advance was the 5th weekly gain out of six, confirming an uptrend to be in place with the ultimate target being the 2024 high at 1.2160.

The entire gain came on Wednesday, Thursday and Friday, which leaves the Pound-to-Euro (GBPEUR) exchange rate overbought according to its divergence from the nine-day exponential moving average (at 1.2081).

We would look for that overbought condition to unwind via a brief pullback to approximately 1.2080-1.2090, ahead of a resumption higher.

The technical setup remains constructive from a medium-term perspective, and by all accounts, GBPEUR is trending towards the 2024 high at 1.2160 ahead of a move towards fresh peaks.

Above: GBPEUR at daily intervals.

Pound Sterling's advances come amidst heightened geopolitical concerns, although last week's talk of a U.S.-UK trade deal would confirm the UK is far less exposed to President Donald Trump's tariff ambitions.

The big event this week is the tariff announcements on Mexico, Canada, and China, which are due to be confirmed on Tuesday.

The March 04 decision could set the tone for global FX for the coming week and, indeed, the coming month.

The U.S. President will likely confirm that he will proceed with 25% tariffs on Mexico and Canada, which have obvious implications for the affected countries, as well as a 10% tariff on China.

"There are going to be tariffs on Tuesday on Mexico and Canada, exactly what they are, we’re going to leave that for the president and his team to negotiate," said Commerce Secretary Howard Lutnick on Sunday.

The message for the Euro will be clear: if he proceeds, the European Union will almost certainly be next in line for punitive tariffs, which means the Euro could come under further pressure in the coming days.

"While April 2 is the date for the broader reciprocal tariffs, the March 4 date is probably more important because if Trump is willing to tariff the closest allies at 25%, there is not much doubt the hammer will drop again April 2," says Brent Donnelly, founder of Spectra Markets.

April 02 is the date set for a global tariff announcement targeting cars, chips, steel and aluminium.

"Certainly, the UK is less exposed to tariffs than its European counterparts. It is hard to argue against EUR/GBP testing major lows at 0.8225 (this) week," says Chris Turner, chief FX analyst at ING Bank.

0.8225 in EUR/GBP gives a GBP/EUR target of 1.2158.

Jeremy Stretch, Head of G10 FX Strategy at CIBC Capital Markets, also considers this level viable.

"The Sterling backdrop looks relatively well supported versus the EUR, not least when combined with the fact that the UK looks less exposed than the eurozone to tariff concerns," says Stretch.

Given that UK goods trade remains relatively balanced and or Trump appears to have a favourable view of the UK, relative to his antipathy as regards the EU, Stretch looks for an extension in the GBP/EUR uptrend.

The CIBC analyst forecasts EUR/GBP to move towards the 19 December low at 0.82225, which in GBP/EUR terms, is 1.2162.

However, should Trump delay the tariffs on Mexico and Canada again, it would signal that the U.S. is negotiating down the full impact of the tariffs.

Above: Canada has said it will retaliate to tariffs, which would encourage Trump to water down the final measures.

This would imply relief for the impacted currencies and a reversal for the Pound.

After all, as we have noted on this website, the Pound is trading as something of a tariff 'safe haven', meaning it stands to give back value in the event that tariffs are watered down or delayed.

So this really is a week of two-way risks for the Pound-to-Euro exchange rate, although there is nothing to suggest the medium-term uptrend will be killed.

Turning to the calendar, the ECB decision is due on Thursday, where a 25 basis point cut is to be expected.

What will be of interest is how the ECB reacts to signs of renewed disinflation in Germany, France and Spain, as it suggests there is more scope to cut interest rates beyond March.

If the ECB hints that it is growing more comfortable with inflation and that the economy remains in need of further support via lower interest rates, then the EUR can come under pressure.

However, analysts agree that there is not enough in the data to warrant a major change in course, which should limit any post-decision market reactions.