Ursula von Der Leyen (President of the European Commission), António Costa (President of the European Council. Image Copyright: European Union.

Pound Sterling is under pressure against the Euro, but the sell-off will fade soon.

Impending tariff announcements by the U.S. on EU imports should still limit the Euro's rise and offer respite for the Pound, say analysts.

"While downside risks for the EUR and euro-zone economy have diminished, they have not completely gone away," says Lee Hardman, currency analyst at MUFG Bank Ltd.

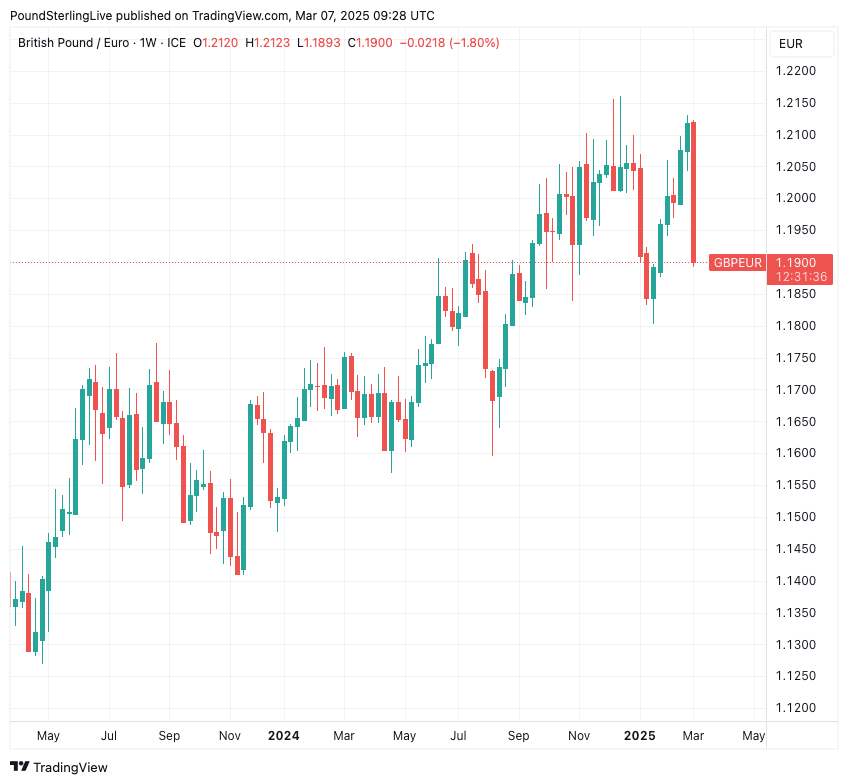

The calls come as the Pound-to-Euro exchange rate looks set to print its biggest weekly decline (-1.83% at the time of writing) since January 2023, prompting questions by market participants as to whether this is a major turning point for the pair or a deep pullback.

Above: GBP/EUR at weekly intervals showing an intact uptrend. But does this big 'down week' signal a top?

Hardman says President Donald Trump's decision to follow through and implement disruptive tariffs on Canada, Mexico and China has increased the risk that the EU will be hit hard too in the coming months.

"Tariffs are a massive near-term risk," says Bill Diviney, an economist at ABN AMRO.

Although Trump on Thursday rolled back some of those tariffs he announced on Tuesday, he said the extension would only last until April 02.

"With this being a delay rather than a lasting exemption and with reciprocal tariffs also expected to be announced after April 2, this leaves plenty of lingering tariff uncertainty," says Peter Sidorov, a strategist at Deutsche Bank.

The Pound had risen against the Euro through February as investors braced for U.S. tariffs on the EU.

However, following this week's tariff measures, the foreign exchange markets delivered a surprising reaction where the Dollar fell and the Euro rose.

"This changing reaction of the dollar comes amid an apparent broader shift in market perspectives on tariffs over the past few weeks, with the focus moving from the potential boost to inflation to the negative implications for growth," says Jim Reid, Strategist at Deutsche Bank.

Abetting the Euro's recovery was the decision by Germany to change its constitution to allow it to borrow more money to invest in defence and infrastructure, which will provide a long-needed boost to Eurozone demand.

The Euro's rally was then fuelled on Thursday by the European Central Bank's decision to cut interest rates and produce guidance that raised question marks about the likelihood of an interest rate cut in April.

European leaders then agreed at a meeting of the European Council to proceed with a special programme to inject billions into the bloc's economies to boost investments in defence.

The impact of the German spending decision impacts the Euro via ECB policy as it is inflationary, meaning the market sees far less scope for ECB rate cuts.

Above: Trump confirmed in his State of the Union address that significant tariffs were proceeding on April 02. Image: Official White House.

However, the ECB will remain cautious as Trump's tariffs pose a headwind.

"Once U.S. tariffs on the EU are announced and implemented, we look for a setback to lower levels," says Dominic Schnider, a strategist at UBS Chief Investment Office, regarding the Euro's outlook.

"The recent rally seems to be a bit stretched and we expect U.S. tariffs on Europe to bring the pair lower in coming weeks," he adds.

Francesco Pesole, FX Strategist at ING Bank, says an extension to 1.10 in EUR/USD would be inconsistent with the prospect of U.S. tariffs on the EU and rate differentials.

"Our model still shows at least a 1-1.5% correction is in store for EUR/USD in the short term," he adds.

Such a correction would prompt a recovery in the Pound-Euro exchange rate.

ABN AMRO's Diviney says that while the fiscal bazooka is rightly dominating headlines right now, Germany (and the eurozone) are on the brink of a potentially massive rise in tariffs on its exports to the U.S.

On April 02 the administration is expected to come with new tariffs on the car sector and pharma (among others), as well as 'reciprocal tariffs' which seek to correct for something that is not actually a trade barrier – VAT.

"If the administration were to go ahead with all of its threats, this would represent a much bigger growth shock than we currently have in our base case," says Diviney.