Friedrich Merz. Reichstag Building, Plenary Hall, Berlin / Germany. Photographer: Marc Beckmann.

Pound Sterling rises against the Euro as the glow of the German fiscal bazooka fades.

Yes, a massive spending deal has been agreed upon, but implementation and embedded structural constraints in the German economy mean it can only go so far.

The Euro is at risk of "buy the rumour, sell the fact" price action after German politicians passed a law allowing the government to ramp up spending on defence and infrastructure.

The German Bundestag agreed to a €500BN infrastructure fund and changes to the debt brake to allow for nearly unlimited defence spending and for state governments to borrow more.

Despite the law being passed, the Euro was unable to advance further against the Pound Sterling, the Dollar and other major peers, confirming that much of the spending 'bazooka' is now 'in the price'.

Goldman Sachs Slashes Pound-to-Euro Forecast

Carsten Brzeski, Global Head of Macroeconomics at ING, says the market sees the chances of a cyclical rebound in the German economy on the back of positive sentiment effects from increased spending. However, some challenges remain.

"How long this cyclical rebound will last and whether it could become a structural recovery will now highly depend on whether or not the official coalition talks will eventually lead to real structural reforms. Otherwise, today's fiscal package will only be a very huge flash in the pan," he says.

The Pound-to-Euro exchange rate has recovered 0.20% in the 24 hours since the Bundestag passed the laws, reaching 1.19.

The Euro rose in the wake of incoming chancellor Friedrich Merz's announcement that he would seek to change the debt brake to boost spending. Sterling is still down 2.0% since the announcement, and analysts at Goldman Sachs have subsequently slashed their forecasts for the pair following a significant long-term reapraissal of the German economic outlook.

The Euro-to-Dollar has fallen 5.60%, helped by broader USD weakness, prompting a raft of forecast upgrades for the single currency.

All indications point to the German 'Bazooka trade' finding its limits, which could ease the rally.

"As with reunification, a fiscal expansion does not guarantee success: the next government will need to deliver structural reforms to turn this fiscal package into sustainable growth," says Robin Winkler, Chief German Economist at Deutsche Bank.

Berenberg economists say the planned spending boost will raise German economic growth and inflation to 2.4% in 2026 and 2.5% in 2027, up from 2.3% in 2025.

Expectations for higher German inflation rates have boosted German bond yields relative to elsewhere as investors demand greater compensation for holding German debt. Increased yields, meanwhile, attract investor cash, boosting currency flows that support the Euro.

This raises the question of how much higher bond yields can go, because if the trend can extend, so too would the Euro's rally.

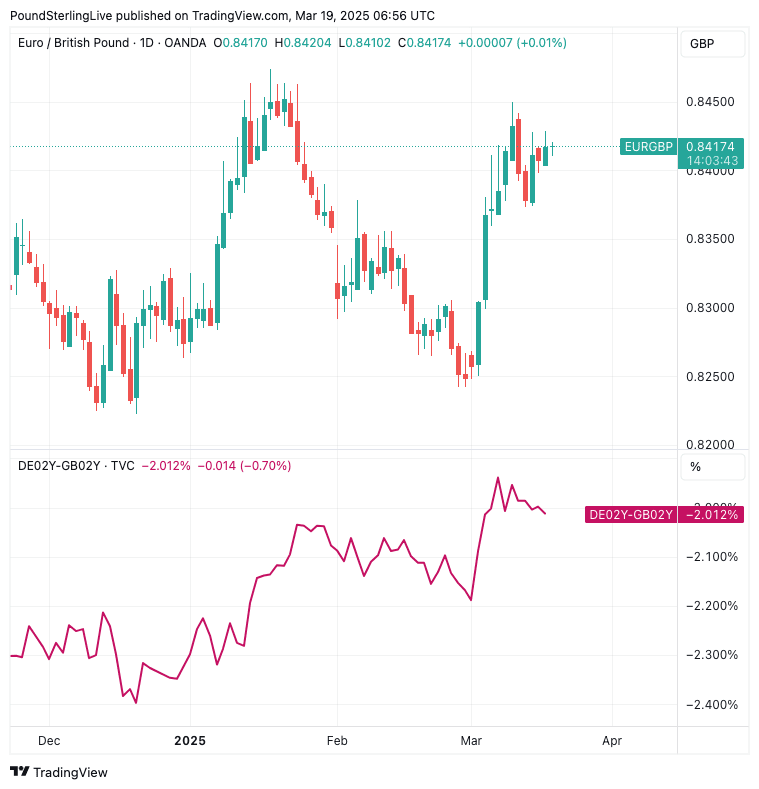

Above: EUR/GBP has risen as the difference between UK and Germany bond yields (lower panel) shrinks.

Berenberg economist Holger Schmieding says more German public spending justifies higher bond yields, but he sees limits from here.

"We find the knee-jerk surge in yields by 40-50bp after Germany had unveiled the plan to loosen the debt brake somewhat overdone," he explains. "A permanent rise in German (and Eurozone) 10-year bond yields by up to 30bp relative to a scenario without Germany’s fiscal U-turn seems more adequate to us."

Economists at Capital Economics agree that German bond yields are reaching a limit and "will remain around its new level."

A decline in bond yields would weigh on the Euro.

"We forecast a drop back in the euro," says Hubert de Barochez, an economist at Capital Economics.

Currency analysts at Commerzbank have warned the Euro could be set to fall "quite sharply" in the coming weeks as "euphoria" over Germany's spending plans fades.

The timing of the fiscal impact will have lags and Commerzbank economists do not expect Germany's planned stimulus to have an effect until next year at the earliest.

They also warn Germany has historically struggled to spend, even when the money is made available.

"This year, growth in the euro area could even be weaker if Trump follows through on his tariff announcements on EU imports in the near future. In short, we expect the EUR-USD exchange rate to fall quite sharply in the coming weeks," says Michael Pfister, FX Analyst at Commerzbank.

Nevertheless, most analysts agree that the significance of the reforms in Germany will have a positive knock-on effect on other sectors of the economy and in neighbouring European economies.

Germany's most-watched confidence survey, from ZEW, showed strong growth in expectations in March:

"The brighter mood is likely due to positive signals regarding the future German fiscal policy, for example, the agreement on the multi-billion-euro financial package for the federal budget," says Achim Wambach, President of ZEW.

"Prospects for metal and steel manufacturers as well as the mechanical engineering sector have improved. Last but not least, the sixth consecutive interest rate cut by the ECB means favourable financing conditions for private households and companies," he adds.

According to Nick Kennedy, FX Strategist at Lloyds Bank, Germany's shift is "a rare bullish development for the EUR and Eurozone. This is still a potentially significant structural shift in market and economic dynamics, with several positive layers to it."

So while the Euro's rally could fade, setbacks might prove to be shallow and 2025's lows might be in the rear view mirror.