Image © Adobe Images

The Pound to Euro exchange rate lost altitude in early trade on Wednesday as the US Dollar unravelled afresh in an apparent response to the latest in the US-China trade conflict, and a proposal in Washington for a tax on foreign holdings of American assets to be imposed on some jurisdictions.

Adding slightly to GBP/EUR’s decline early in the London session was a 20 basis point fall in the rate of inflation, to 2.6%, and a larger as well as more meaningful 30 basis point decline in the rate of services sector inflation, to 4.7%, which is the measure most closely watched by the Bank of England.

However, the decline dates back to President Donald Trump’s statement late on Tuesday suggesting he may force countries to choose between trade relations with the US and trade relations with China, threatening a possible bifurcation of the global economy and financial markets.

“Moreover, underlining that what starts with tariffs and trade spreads to capital and other areas, Congressional Republicans are proposing legislation that would penalise holders of US financial assets for anyone from a country that imposes a “discriminatory” tax,” says Michael Every, a global strategist at Rabobank.

Above: GBP/EUR at 15-minute intervals with ICE US Dollar Index. Click for closer inspection.

In addition, there is reportedly a new proposal in Washington for a 5% annual levy, rising by 5% per year up to a maximum of 20%, on US assets held by countries who maintain digital services taxes, which would apply mainly to the European Union and Canada, according to Every. However, both the UK and Switzerland are among the others who also have similar taxes, perhaps due to Brussels' own penchant for pushing the extraterritorial adoption of its own rules and regulations.

To say the least, the proposals risk prompting a renewed or continued Exodus from Dollar assets similar to that seen in the week to Passover on Friday. The Dollar already fell against all G20 currencies overnight except for the Chinese Renminbi and Indonesian Rupiah even as global equity markets also declined broadly.

“In keeping with the Passover theme, it’s also important to stress we have four kinds of analysts’ takes on what’s going via the questions they ask about it: the Wise (“Why is this happening?”); the Wicked (“What has this got to do with me/my view?”); the Simple (“What?”); and Ones Who Don’t Know How to Ask,” Every says.

“Which analyst are you? To the answer: this market is different from all other markets because in all other markets we assume there is one global economy within which all goods, services, and capital flow, with one single global reserve currency, the US dollar. Now, we might be witnessing an Exodus from it,” he adds.

Above: GBP/EUR at daily intervals with ICE US Dollar Index. Click for closer inspection.

The Dollar unravelled in a broad-based rout last week that took place amid simultaneous declines in all major US equity markets accompanied by periodic bouts of weakness in the Treasury market, and amid what appeared to be frequent interventions from Beijing in support of the Chinese Renminbi.

The asset sales seen over that period clearly and strongly favoured currencies of current account surplus jurisdiction such as the Euro Area, Switzerland and Japan, among others, who are some of the largest foreign holders of US stocks and bonds.

However, without irony, Beijing currently appears to be one of the few things, if not the only thing, keeping the Dollar from falling into a bottomless pit or abyss, as it seeks to maintain a “basically stable” trade-weighted Renminbi, which is positively-correlated with the Dollar.

“The shift in correlations between the dollar, US yields and US equities is startling in recent weeks, with the USD falling despite higher US yields and lower US equities. This may be temporary, but it has happened very rarely in the past so does bear watching,” says Dominic Bunning, head of FX strategy at Nomura.

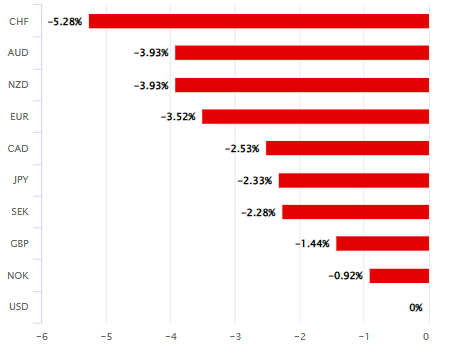

Above: US Dollar performance relative to G10 currencies for the week to Friday, 11 April.

Source: Pound Sterling Live. Click for closer inspection.