- UK debt crisis brews, is key risk for GBP

- Promising another painful Autumn Budget

- But global risks ease, boosting GBP near term

Picture by Simon Dawson / No 10 Downing Street.

Surging state spending vs. improved background mood music to pull Pound Sterling in opposite directions.

The British Pound faces a summer of conflicting drivers, with positive investor sentiment expected to provide tailwinds, but the government's inability to get a grip on its public finances will be a distinct headwind.

Reports suggest Prime Minister Keir Starmer is ready to water down his attempt to slow the increase in disability benefits growth.

By tightening eligibility for Personal Independence Payment (PIP) - the benefit for those who can't work because of sickness or mental health issues - the UK government intended to shave a paltry £5BN off its expenditure.

But a massive rebellion by Labour Party MPs means the total savings targeted is no longer feasible and there is talk that Starmer will lower his ambitions to save his political skin. The u-turn comes just weeks after Starmer folded in his attempts to restrict winter fuel allowances for pensioners to those who truly needed them.

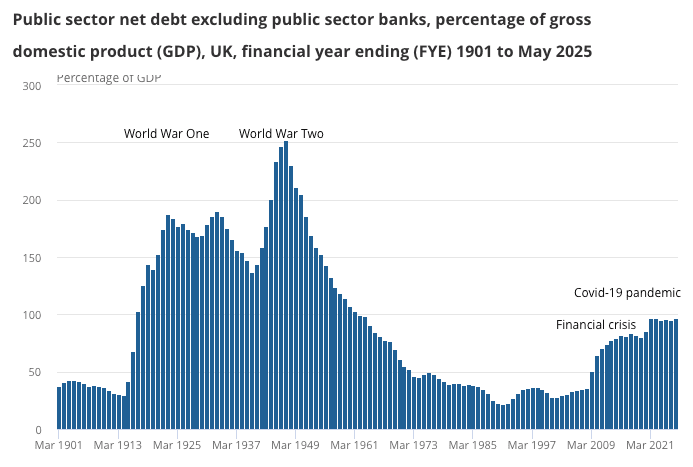

Above: UK debt as a % of GDP is nearing 100%. Source: ONS.

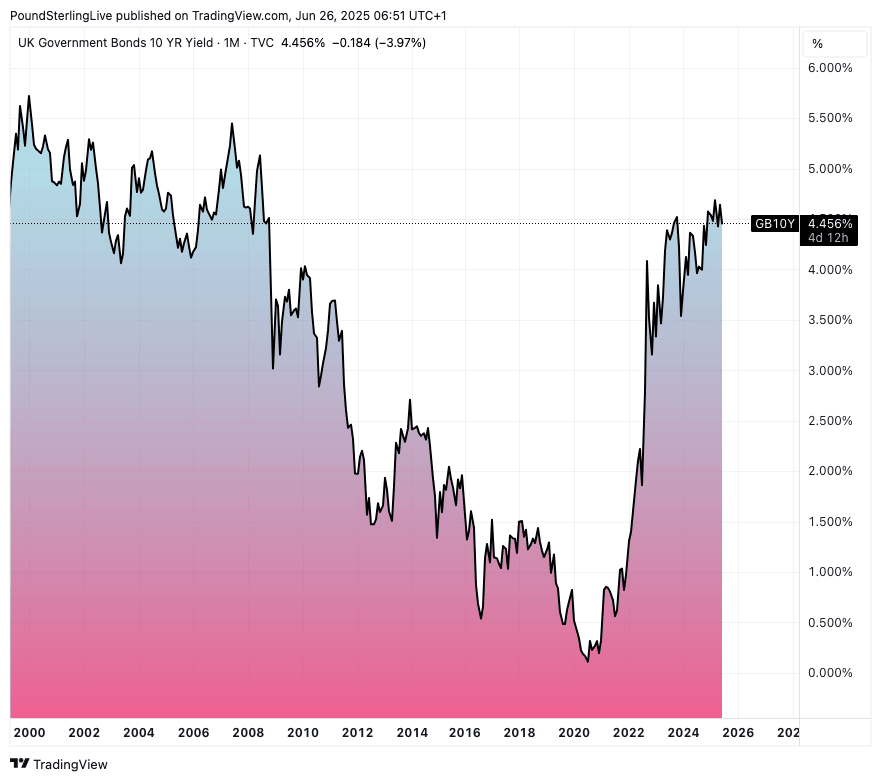

"This comes at a tricky juncture for Chancellor Rachel Reeves, whose tight fiscal rule limits flexibility. With debt above 100% of GDP and long-end yields near their highest since 1998, debt-servicing costs are rising sharply, compounding downside risks for sterling," says Antonio Ruggiero, FX & Macro Strategist at Convera.

An inability to control spending comes against a backdrop of ballooning debt and rising debt costs. One measure, the UK ten-year bond yield, is closing in on levels last seen at the turn of the millennium. For context, back then, the welfare state was nowhere nearly as big as it is now.

For the market, the messaging is clear: cutting expenditure is increasingly unlikely under the current regime, which is still in its infancy. It means the UK Chancellor, Rachel Reeves, must almost certainly hike taxes again in the Autumn and in subsequent years.

Above: The yield on UK ten-year bonds is at its highest level since 2008.

Taxes are already set to reach their highest proportion of GDP in peacetime, and there is strong evidence that further tax hikes will lead to capital flight and business retrenchment.

There will be major implications for financial markets if Reeves gets her tax hikes wrong, with a worst-case outcome being a full breakdown in market confidence in UK financial assets, including the Pound.

Already in January, we saw bond yields - the interest rate paid on UK government bonds - rise and the Pound fall. In healthy times, they move together, meaning their decoupling is the first indicator of financial market concerns.

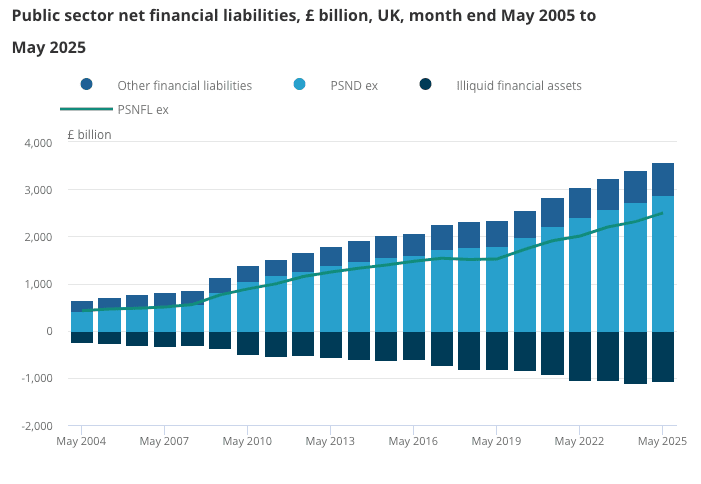

Above: "The upward trend in public sector net financial liabilities is largely because of increases in net debt." - the ONS.

Recall the Pound's collapse and the spiral in debt costs when Liz Truss tried to pass her mini-budget.

Reeves risks a Truss 2.0 moment. Back in January 2025, the worry was that the economy would slump under Reeves' previously announced tax hikes, which would mean the government would struggle to repay its debt.

More tax rises will see these fears return. Shevaun Haviland, Director General of the British Chambers of Commerce, warns today that if the Government is serious about growth, then it cannot tax business any further.

"We were unprepared for the huge burden placed upon us, and it led many of us to rethink our growth plans. As a result, our business confidence measures have fallen to their lowest levels since 2022," she says.

Although a market rout of UK assets is unlikely for now, as the Autumn Budget approaches, these issues will grow more acute, and risks making it starkly clear that the UK is running out of road.

Yet, For the Pound, It Could Still be a Good Summer

Image © Adobe Images

With the Autumn Budget still some time away, investors can focus on other issues, and Pound Sterling could find the global picture to be supportive now that the Middle East conflict is fading and we are getting a handle on how Donald Trump will approach the issue of tariffs.

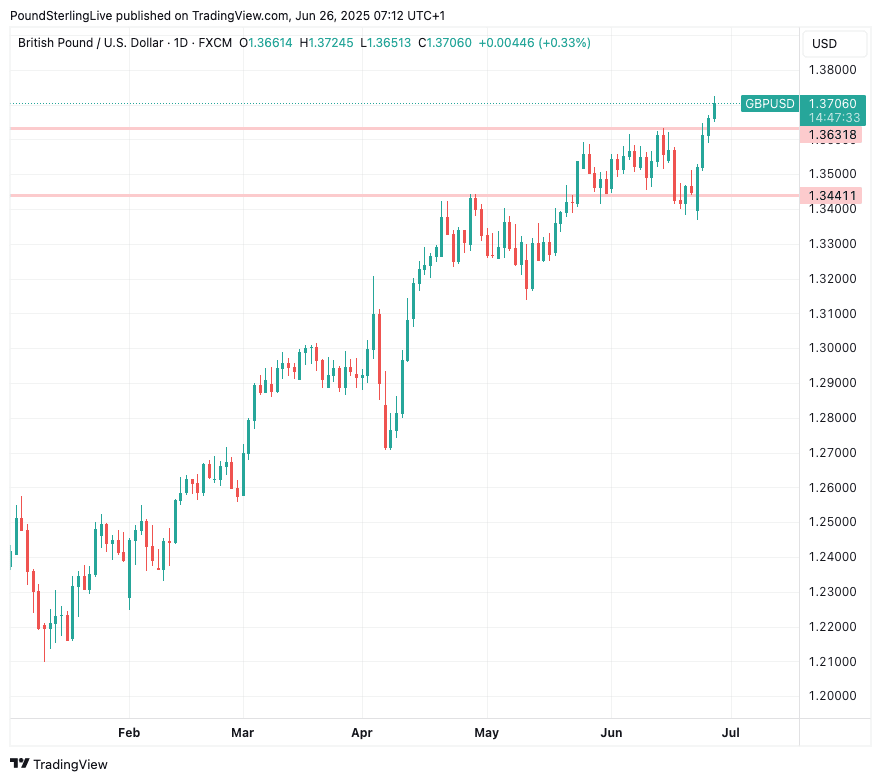

If global events become more benign, it would allow the Pound to Euro exchange rate (GBP/EUR) to hum along in recent ranges and the Pound to Dollar exchange rate (GBP/USD) to extend its rally to 1.40.

GBP/EUR tends to struggle during times of heightened market volatility, meaning a period of steady gains for world stock markets can help the exchange rate recover from recent lows.

"The higher yielder currencies will continue to benefit as we enter the Summer holiday season and see volatility grind lower and SPX grind higher," says W. Brad Bechtel, Head of FX at Jefferies LLC.

Above: GBP/USD is trending with conviction.

The Dollar is meanwhile in a determined downtrend, which gives the GBP/USD a free pass in the absence of any significant and pressing domestic developments.

"We may be entering a period of structural USD weakness as the Asian exporter community finally lets their currencies strengthen," says Bechtel.

"The asset owner community is also increasing their allocation to the EU and the EUR and that is happening now. A lot of that theme has run pretty far, pretty fast so far this year already, but it will continue to happen over many months and quarters as this is a slow grinding process," he adds.

A series of fresh highs beckon for GBP/USD in the coming weeks and GBP/EUR could even eye 1.19 again. However, when market focus returns to UK finances, sentiment towards Sterling could rapidly change.