Image © Adobe Images

There are very few routes to weakness for the Pound on Thursday.

Thursday's interest rate cut at the Bank of England will be of little interest to currency markets, which have had the whole of July to steadily sell the Pound in anticipation.

Instead, the forward-looking market will keep a finger on the trigger and hit the currency on any signal that the Bank intends to cut on two more occasions in 2025, or indicate it aims to press Bank Rate below 3.5% in 2026.

This means that for the Pound to weaken on Thursday, some interesting developments are required in the communications. Given recent history, we just don't see such an outcome transpiring.

What the Sellers Need

To be sure, there could yet be some volatility on the day, particularly if some members of the Monetary Policy Committee (MPC) vote to cut interest rates by 50bp, having judged that the economy is slowing and that more support is required in light of consecutive monthly falls in payrolled employment.

Unemployment is rising, vacancies are falling and wage growth is moderating, which will potentially prompt Swati Dhingra to vote for a 50bp move.

"A 25bp cut is well priced in and focus will be on the vote split with markets expecting a quarterly pace of cuts. Any unexpected dovish lean on the back of recent softness in data can weigh on the GBP," says a note from TD Securities ahead of Thursday's decision.

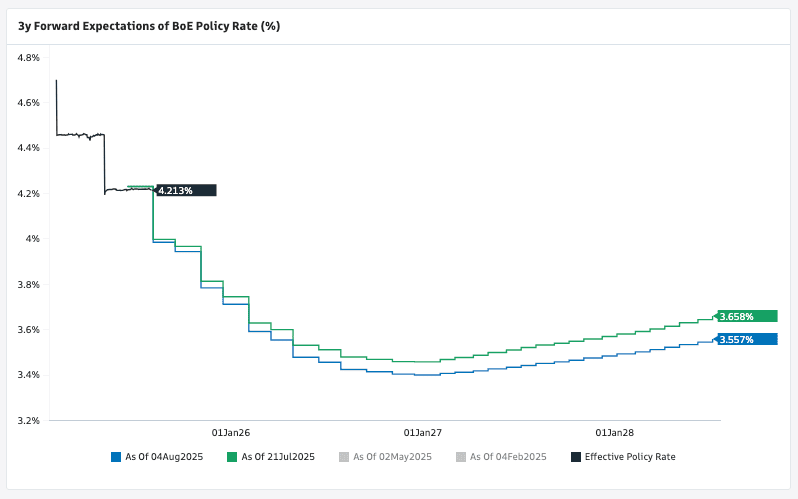

Above: Bank Rate expectations were lowered during July, weighing on the Pound. The question is, how much further can it fall from here?

The Pound to Euro exchange rate (GBP/EUR) has fallen for two months in succession, with a 0.75% decline registered in July, as markets moved to fully anticipate the August and November rate cuts.

However, Chris Turner, head FX analyst at ING, says a further rate cut in the new year is not quite fully priced, and this could expose the Pound to some weakness.

"If the BoE is working off a cycle of 25bp rate cuts per quarter, then market rates are lagging at pricing in only 55bp of cuts by next February's meeting. The risks are skewed to more rather than less easing being priced in – threatening upside risks to EUR/GBP. At the same time, the noise around the November UK budget adds a negative event risk for sterling," says Chris Turner, head of FX research at ING Bank.

Why the Pound Will be Supported

Although there are risks to the downside for the Pound, the reality is that inflation in the UK is simply proving too stubborn to justify any quickening in pace or a deepening of the cycle below 3.5% next year.

"Given the resurgence in inflation, and the risk of second-order effects, we expect a couple of MPC members to vote for a hold," says Christopher Graham, an economist at Standard Chartered.

Inflation is rising again, while food inflation is doing so increasingly quickly, which risks resetting consumer and business inflation expectations higher. If that were to happen, inflation will prove incrasingly difficult to supress in coming months and years.

The judgement of the majority of the MPC is that signalling quicker rate cuts at such a moment risks a catastrophic deanchoring of inflation expectations that would undermine the Bank's credibility.

Image courtesy of Standard Chartered.

They will be aware that falling wages don't appear to be suppressing inflation, as was expected, which analysts say should prompt the majority of MPC members to opt to stick with current guidance.

However, some analysts we follow think the Bank could soon be forced to abandon its cutting cycle altogether.

"We have a hawkish Bank Rate forecast, expecting August to see the final cut this year, and the last cut until after 2027," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.

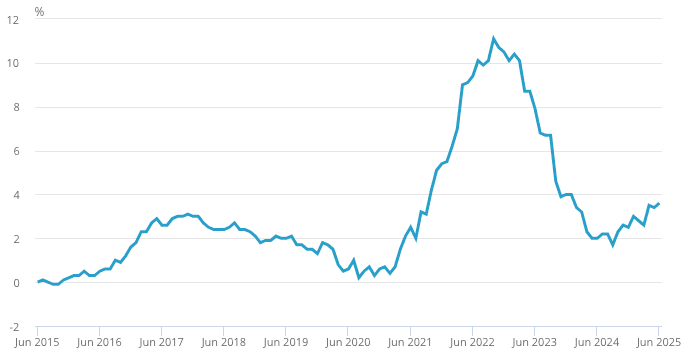

Above: Inflation is rising again, having only briefly reached 2.0%.

Pantheon Macroecomic's argument is that the economy is more resilient to high interest rates than many might assume. Their calculations reckon that the 'neutral' level in Bank Rate is in the 3.75-4.00% region. This means another cut leaves rates "barely restrictive," says Wood.

It also means the Bank risks entering stimulatory territory - where it actively contributes to higher inflation - if it cuts again in November and early 2026, which is what money market pricing shows investors currently anticipate.

"It will be interesting to see whether the BoE maintains its 'gradual and careful' rate guidance. We suspect that it will, although any change here would almost certainly be greeted by a bout of GBP weakness," says Enrique Diaz-Alvarez, Chief Economist at Ebury.

For the Bank to abandon a November cut, we would need upcoming inflation prints to surprise to the upside, which would convince the MPC that it risks making a policy mistake by cutting beyond August.

It's clear that the Bank's best option is to stick to current guidance that suggests more cuts are coming, but that it will remain cautious.

Because this outcome is expected, it would represent little downside threat to the Pound, and could even encourage a relief rally to transpire.