Chancellor Rachel Reeves. Picture by Simon Walker / HM Treasury.

The British Pound stabilises and could recover after a shaky start to September.

A recovery in global bond markets has helped the Pound recover against the Euro and Dollar, while on the domestic front, a long wait for the Autumn budget could also help.

After falling heavily on Tuesday, UK and global bonds recovered through the midweek session, helped in part by a soft U.S. job opening report that raised the odds of more Federal Reserve rate cuts beyond September.

This has boosted global investor confidence, and the worst-hit assets of Tuesday - such as UK gilts and the Pound - lead the recovery through midweek and into Thursday.

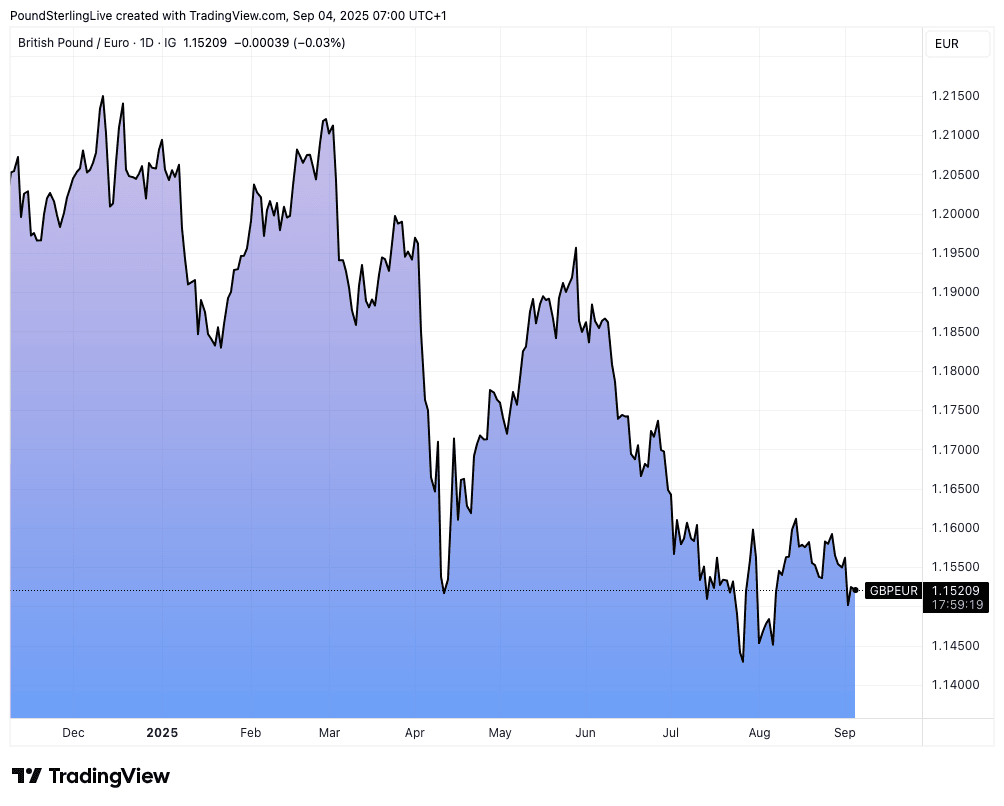

The pound to euro exchange rate recovered about half of Tuesday's loss to go back above 1.15, while the pound to dollar has also pared about half of the loss to rise back to 1.3426. Those with payment should consider setting an order to automatically secure their desired rate.

In the UK, the Treasury confirmed the budget will be held on November 26, which puts it exceptionally late in the year for a budget.

Some economists have suggested the lengthy wait confirms Chancellor Rachel Reeves has her back against the wall as she looks to plug a fiscal deficit of some £50BN. Concerns over the rising deficit and sustainability of UK debt have been blamed for a soft performance in the Pound against the Euro and other non-USD currencies over much of 2025.

However, currency strategists suggest that the lengthy wait for the budget allows Chancellor Rachel Reeves to come up with a plan, and this isn't a bad thing for the Pound.

"I don’t think this UK fiscal theme is tradable in FX for now as that 26 November date puts too much time on the clock. There could be leaks and newsflow that is tradable in the interim, but what I mean is that I don't think the economics of sitting here short GBP or long GBP puts are positive EV given the long wait."

With impetus to sell the Pound waning, the door opens to a recovery, particularly given the market is sitting on a net 'short' position, i.e. there are more sell contracts outstanding than buy contracts.

"The long wait for the Budget will not help confidence, but there might be some upsides," says Julian Jessop, economist and senior fellow at the IEA. "This leaves more time for global bond markets to calm down (gilt yields could then fall even if the UK remains an outlier."

A calming bond market will allow the pound to lose some of its risk premium it has built up over recent months and perhaps even recover some losses against the major currencies.

"There is plenty of doom and gloom around UK government bonds at present, but there are also reasons that fears may be overblown," says Richard Carter, head of fixed interest research at Quilter Cheviot. "Worries about a 1970s style IMF-crisis certainly seem exaggerated with credit derivative markets showing little concern about a potential debt default."

Ahead of the budget, the Bank of England is anticipated to lend a helping hand by stabilising the bond market.

Currently, it is actively selling bonds in its quantitative tightening programme (reversing the quantitative easing from previous crises), which increases the supply of UK debt, suppressing bond prices and pushing up yields.

But, the Bank will soon announce a review of its sales, likely cutting the volume from £100bn to £75bn for the next one-year period.

Jessop says the lengthy delay could also allow the government to find some new savings on welfare spending that would be acceptable to Labour MPs. This is after the government u-turned on plans to cut the bill by a mere £6BN in July.

Above: GBP/EUR performance since the previous year's budget.

The Treasury would also have more time to persuade the Office for Budget Responsibility (OBR) that higher public investment and new supply-side reforms will boost productive potential, so that the fiscal watchdog doesn't revise down its long-term growth forecasts too far (or at all), explains Jessop.

The rule of thumb is that growth downgrades open up the fiscal deficit, or black hole, that must be filled. Any boosts to the growth outlook would therefore be incredibly beneficial to Reeves.

Jessop says the delay could also mean there's more time for the economy to feel the benefits of less restrictive monetary policy at the Bank of England, in the form of a potential November rate cut and the scaling back of quantitative tightening.

The question is: do the positives simply stabilise the pound or are they enough to trigger a recovery?

Our suspicion is that the pound can stabilise and will have some 'up days' but that upside remains limited, denying the currency a shot at an outright rally.

Analysts agree that the currency faces a nervous wait, and that leaks regarding the budget's contents could spill over into the market again and trigger bouts of severe volatility in the Pound and gilts.

"Tax rises are bad for growth, and with little room for additional borrowing, it leaves spending cuts as one of the only future viable options. With a Labour government already cowed by its own backbenchers, those cuts are unlikely to materialise unless the market forces it to change tack. There is likely some more volatility to come in bond yields as a result," says Carter.