Still of Andrew Bailey. File image. Source: FT.com. There is no planned press conference, but the Governor could well conduct media interviews after the decision.

There is one scenario in which the pound rises, and two in which it falls.

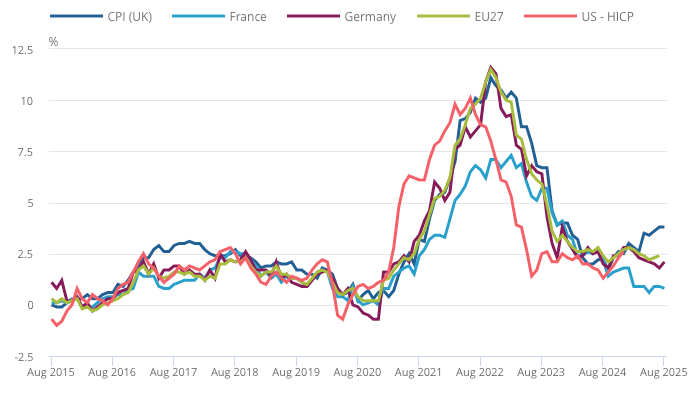

The UK's high inflation rate will preclude the Bank of England from significantly hurting the pound's recovery prospects when it issues its decision on interest rates today.

A survey of economists shows the Monetary Policy Committee (MPC) is expected to vote 7 to 2 in favour of leaving interest rates unchanged. It should maintain guidance that it remains attuned to economic developments and is not precommitted to further changes in interest rates.

It should do enough to keep expectations for another cut in November at bay. Currently, the market sees 50-50 odds of another move in November, but the Bank can ill afford to say anything that would ramp up these expectations owing to the UK's persistently high inflation problem.

The Bank narrowly managed to pass another cut by a margin of 5 to 4 in August, indicating growing resistance to further cuts owing to rising inflationary pressures, which rose to 3.8% y/y in August.

Deputy Governor Clare Lombardelli and the Bank's Chief Economist Huw Pill both opposed Governor Andrew Bailey in voting against a cut, as inflation is expected to peak near double its 2.0% target this month.

If the Bank votes 7-2 and maintains guidance, then the pound can count on ongoing support from the UK's relatively high interest rates.

Foreign capital tends to flow to where interest rates are elevated, and the UK has the highest base rate in the developed world.

Above: The UK commands high interest rates because it has a unique inflation problem.

Interest rate cuts in the U.S. and Canada midweek boost the UK's interest rate advantage, which should underpin the pound if global market volatility remains supressed.

Ahead of the midday decision, the pound to euro exchange rate trades at 1.1530, putting it back in the middle of a multi-week consolidative zone.

The pound to dollar pair retreats to 1.3595, having topped out in the wake of the Federal Reserve's midweek policy decision, as the expected "sell the fact" reaction to the decision played out.

If anything, a status quo vote could allow the dollar to recover further against the pound, with strategists at TD Bank looking for a further 0.20% decline on such an outcome. It sees a 55% chance of this happening.

However, analysts at TD also see a small chance of an outright 'dovish' scenario where the Bank tries to prime the market for a November cut.

Here, Bank Rate remains on hold at 4.00%, "but the message returns to there being two-sided risks, noting sticky inflation on one side but an easing labour market on the other."

It says there's only a 10% chance of such a scenario, which would hit the pound with an approximate 0.60% loss.

What would the Bank need to do in order to push the pound higher?

According to TD Bank, the vote split would need to come in at 8-1 in favour of a hold, suggesting even the doves are less comfortable about inflation's rise.

The statement would also need to say that although there's been "substantial disinflation over the past two and a half years," the path is now less certain and the pace is slower than expected.

"There is an allusion to monetary policy not being sufficiently restrictive, suggesting that the pace of easing will slow," says TD Bank.

The UK's deteriorating labour market advocates for further rate cuts, and a small minority members of the MPC will likely vote for a cut today.

Strategists at TD reckon there's a 35% chance of such an outcome. Here, the pound stands to gain by as much as 0.30%.

The Bank of England will need to be very cautious as there is growing evidence it has lost control of the inflation narrative.

The Bank's own inflation survey was out last Friday and it revealed inflation expectations for the next five year period have unanchored to well above 2.0%.

The British Retail Consortium is meanwhile out with a poll on Tuesday that finds 52% of the public predict an economic deterioration in the next three months owing to inflation's rise.

"Inflation is now one of the biggest concerns among the public, with food inflation expected to rise to 6% by the end of the year," says Helen Dickinson, chief executive of the BRC.

Rising inflation expectations are a headache to the Bank, which is mandated to bring inflation back down to 2.0%. If the public and businesses think inflation will rise they will pursue inflation-stimulating behaviour, for example seeking higher wages and selling goods and services at higher prices.

If the public thought the Bank had a grip on inflation, their expectations for future price rises would settle, which would provide a positive feedback loop.

The Bank will also need to be cautious heading into the November budget, where the Chancellor will likely announce further tax rises.

Economists say increasing National Insurance in 2024 was undoubtedly inflationary and unhelpful for the Bank. If the Bank thinks the government will make the same decisions again, then it would do well to maintain caution on interest rates in the coming months.