The Chancellor of the Exchequer and the Secretary of State for Science, Innovation and Technology visit the Google Data Centre at Waltham Cross. 16/09/2025. Picture by Simon Walker / HM Treasury.

Pound sterling to stay on the defensive into November's budget.

We keep repeating to our readers that the November budget is the key source of anxiety that is holding the pound back.

It won't help, then, that the latest public sector borrowing data shows an unexpected deterioration in the government's finances.

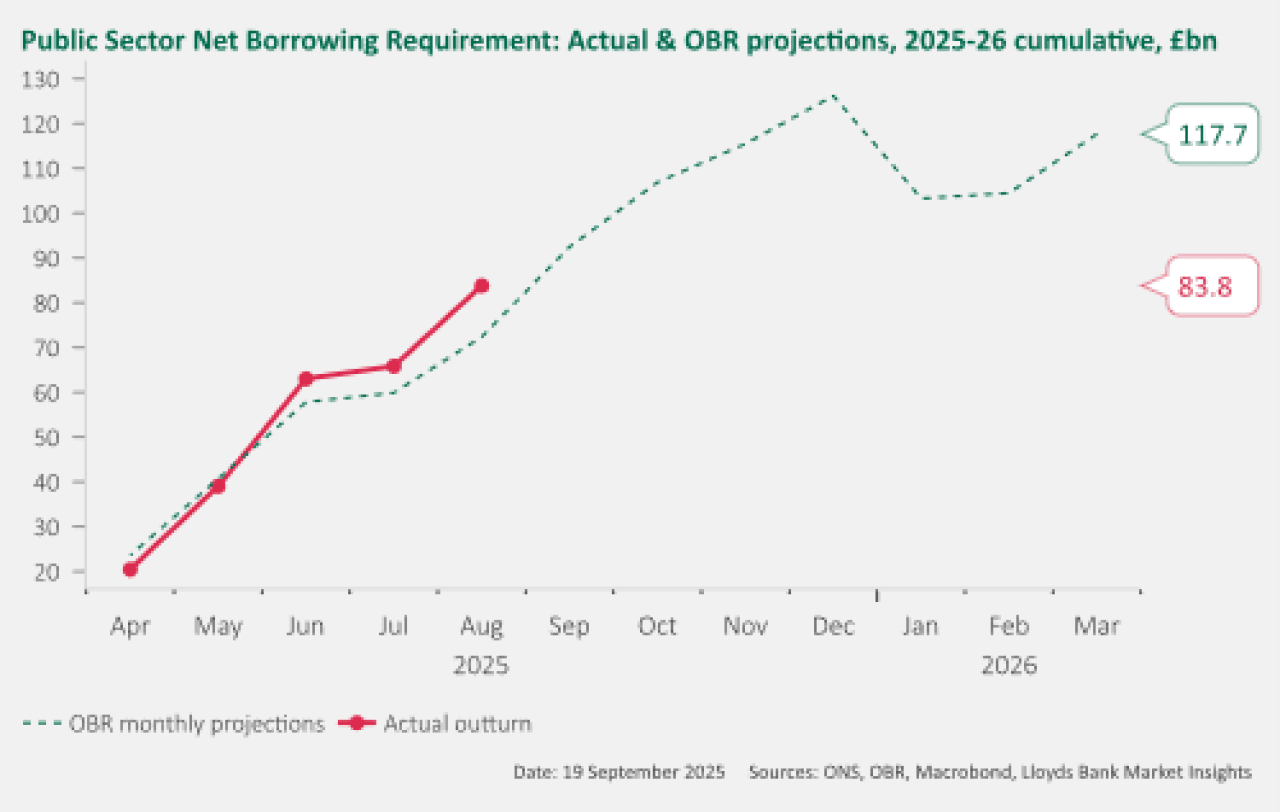

To be sure, the finances were never good, but the ONS on Friday revealed a deficit (PSNB) of £18BN for August, £5.5BN ahead of the OBR Spring forecast. This was the second-highest August borrowing on record, after the Covid shock of 2020.

There's more bad news for Chancellor Rachel Reeves: the ONS has revised the data for previous months and the overall deficit for the year stands at £83.8BN, putting it £11.4BN higher than it was forecast to be at this point in 2025-26.

Image courtesy of Lloyds Bank.

"This is a significant development as previously the deficit was tracking right in line with expectations," says a note from Lloyds Bank's economic analysts in the wake of the release. "In addition to the overshoot in borrowing in August, the ONS has engaged in a deeper review of prior months leading to unfavourable revisions."

Driving the deficit was a rise in government spending, which increased by £8.2BN (or by 9.2%) compared with August 2024, with the costs of providing public services, benefits and debt interest repayments all increasing.

Combined central government tax and National Insurance contributions receipts were provisionally estimated to have increased by £4.2BN (or by 5.7%) compared with August 2024. In short, the tax take isn't keeping up with spending.

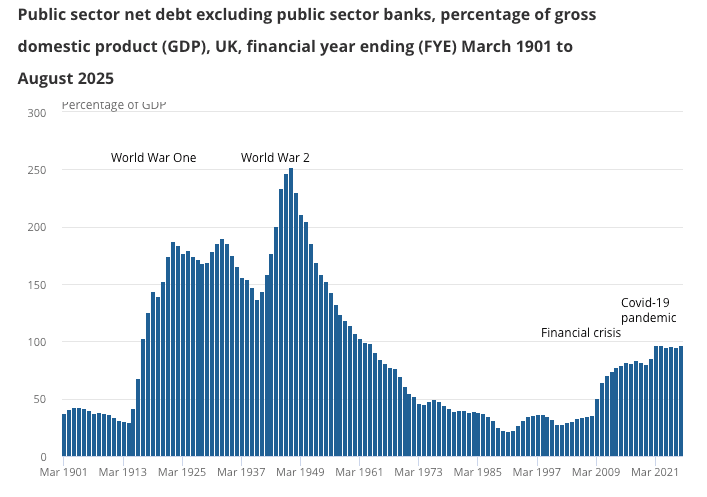

As a whole, Britain's debt at the end of August 2025 was equivalent to 96.4% of gross domestic product, the annual value of everything produced in the UK economy.

For the pound, what matters is how the spending requirements impact debt issuance by the government, and whether the market is willing to absorb this issuance of bonds. If Reeves fails to convince the bond markets that she has a grip on the situation, we could see bouts of UK bond selling that can destabilise the pound.

It's clear that for Reeves to keep markets on side, she will have to either cut spending or raise taxes again in November to ensure the UK's debt trajectory remains on a sustainable footing.

Experience shows Prime Minister Keir Starmer simply doesn't have the support of his 'back benchers' in parliament to pursue meaningful spending reductions, so it falls on taxes to do the heavy lifting.

But with the government committing to not raising the major tax levers of VAT and income tax, it's left with no option but to target investors, businesses and small business owners. It will tinker with the tax code, making it more complex and encouraging defensive tax positioning behaviour by households, investors and businesses.

The tax increases will fall on a small section of the population who play an outsized role in determining private sector investment. With caution likely to increase in anticipation of the tax cuts, a string of underwhelming economic data prints awaits the UK in the coming weeks.

Dour economic prints, general anxiety and expectations for further Bank of England rate reductions will likely pressure the pound into year-end.