Above: File image of Andy Burnham. Copyright by World Economic Forum / Faruk Pinjo. Licensing and source.

Political uncertainty ramps up as a big name in Labour politics is set to challenge Prime Minister Sir Keir Starmer.

Pound Sterling enters a new era of political uncertainty as Andy Burnham, Mayor of Manchester, has confirmed he is actively considering challenging embattled Prime Minister Keir Starmer for the keys to 10 Downing Street.

He told The Telegraph in an exclusive interview that Labour MPs are privately urging him to challenge Starmer. This after he told the New Statesman: "the issue... is not who is the deputy leader of the party, who is the leader of the Labour Party... are we up for that wholesale change? Because I think that’s what the country needs."

The overt confirmation comes after weeks of speculation that he is ready to challenge the Prime Minister.

"Political risks in the UK is once again spooking the UK's bond market. Andy Burnham, the mayor of Manchester, seems keen to replace Kier Starmer as Prime Minister," says Kathleen Brooks, analyst at XTB.

There are two immediate issues for the British pound:

1) It intensely dislikes uncertainty, with one only needing to look back at the troubles of the Brexit years for proof, and

2) Burnham is promising to spend big and ignore the bond markets in the process, which is a significant problem for the UK's debt trajectory. We know the pound is already highly sensitive to developments on this front.

Off the bat, a Burnham Number 10 would raise spending by £43BN on welfare: he explicitly says he will borrow £40BN to fund a new social housing push. Then, £3BN is needed to drop the two-child limit that only allows families to claim universal credit and tax credits for up to two children.

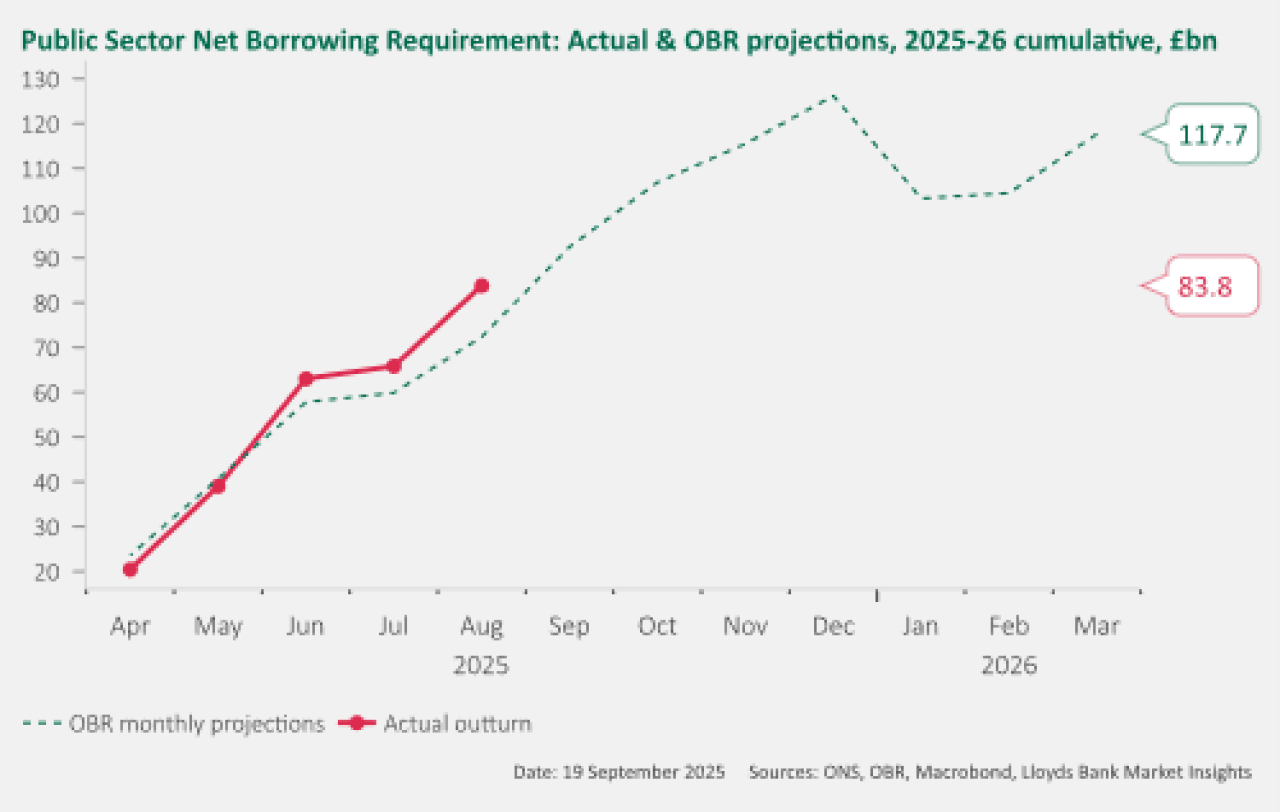

Consider that the pound is already under pressure on concerns Chancellor Rachel Reeves needs to find up to £30BN in savings and extra taxes to plug a black hole that has arisen in the country's finances over the past year:

Above: UK borrowing is higher than predicted, opening up a 'black hole' in the finances that Chancellor Rachel Reeves must fill.

Any hopes of a credible and sustainable fix to the UK's unsustainable fiscal path would simply be blown away by Burnham's plans: he wants to cut income taxes for lower earners and raise the tax on higher earners to 50p in the pound.

However, the elasticity of tax revenue, as well as the shape of the UK's taxbase, means the loss in revenue from the cut in the lower rate will vastly exceed the increased revenues from the increase at the top end.

Most troubling of all is Burnham's message in his New Statesman interview: "we’ve got to get beyond this thing of being in hock to the bond markets."

This statement references a perceived belief in leftwing circles that financial markets are limiting the government's ability to borrow more and spend on welfare projects.

It suggests a fundamental misunderstanding of how the financial world works: where Burnham sees odious figures in the boardrooms of the big banks as being behind the limits on UK borrowing, the reality is the bond market is simply a pool of lenders, with pension funds being particularly prominent.

Governments aren't "in hock" to them; they are completely at their mercy.

If a lender doesn't want to lend to the government because they think the government will struggle to repay, then you get a 'lender's strike' and a potentially explosive problem for the government.

"The bond markets are simply the people and institutions who lend government money. We can avoid being 'in hock' to them by reducing borrowing. We struggle now because our borrowing and debt are extremely high. Mr Burnham wants to increase borrowing," says Paul Johnson, Director of the IFS.

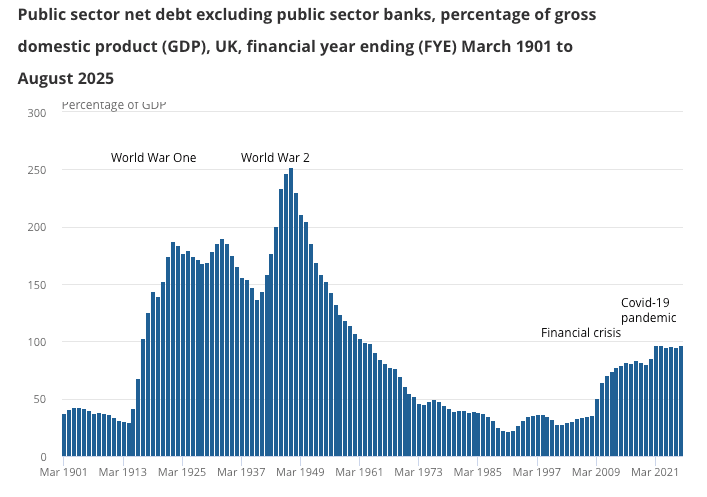

Above: The UK's debt pile is exceptional for a time when the country is not fighting an existential war.

The cavalier attitude to markets by Burnham has swiftly drawn comparisons to former Prime Minister Liz Truss, who tried to pass a budget that would have raised the UK's borrowing significantly without being properly costed.

Following her infamous 'mini budget' UK bonds were dumped, yields surged, the pound cratered and Truss was ejected.

"Is Andy Burnham, Labour's Liz Truss?" asks Kathleen Brooks, an analyst at XTB. "Although Starmer is unpopular and the government’s approval ratings are through the floor, a change of leadership could exacerbate the UK’s fiscal problems even more."

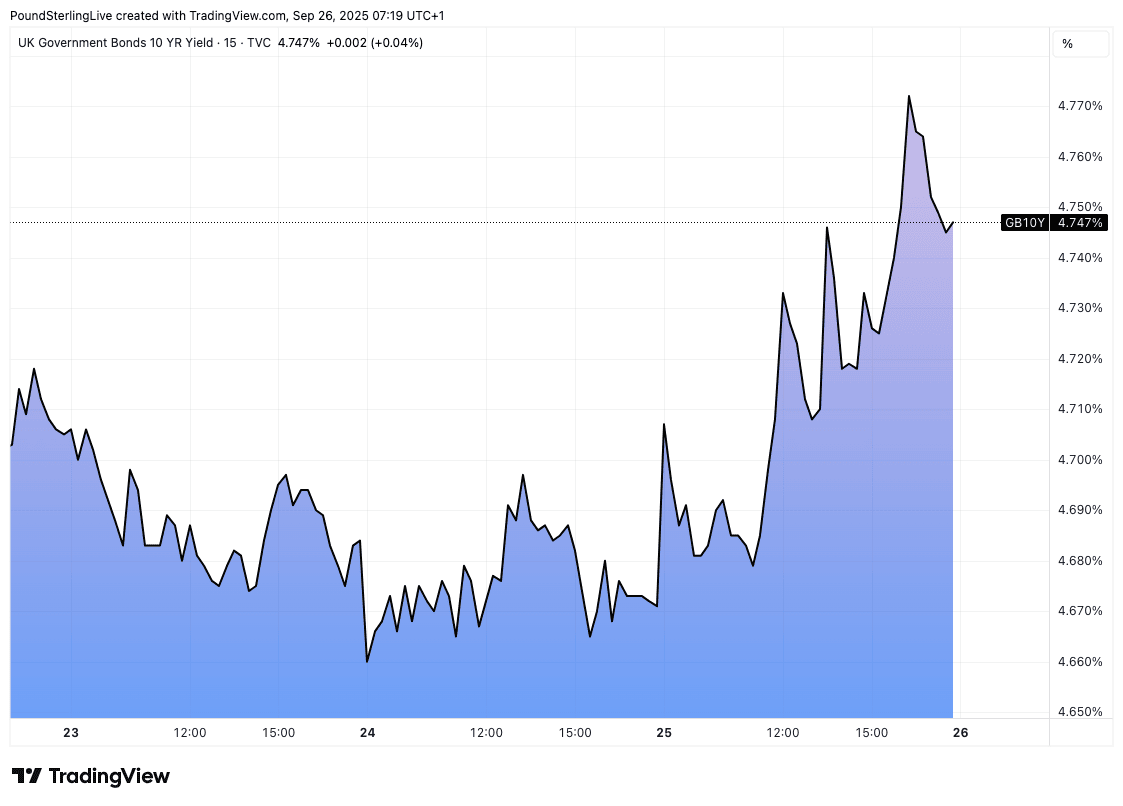

On Thursday, as markets considered the Burnham news, UK 10-year bond yields - a key benchmark of government borrowing costs - went higher by more than 5 basis points.

"Although global bond yields are rising, the UK is the outlier, and is a major underperformer compared to our peers," says Brooks, highlighting UK-specific risks.

Above: The yield on UK ten year bonds over the past 24 hours.

Brooks explains that the comments about the government being in "hock" to the bond market, "has awoken the bond market vigilantes."

Pound sterling's performance also reflects this uncertainty: "the pound is the second weakest performer, as it struggles once more under the weight of political concerns," says Brooks.

Simon French, an economist at Panmure Liberum, warns that the government can choose to ditch its fiscal rules and not be "in hock" to the bond market if there is a path to value for money on additional borrowing.

However, he warns that the UK has a serious credibility deficit on this front.

"The OBR has no pre-ordained reason to exist in the UK’s economic framework. But if you want to abolish it, you do so from a position of strength, not weakness. The bond market is telling the government that it’s in a weak position," says French.

Even if Burnham does not become Prime Minister, the damage is already potentially done as the political pressure is pressing Starmer to veer leftwards.

This means the UK could be prone to more borrowing and spending on welfare, which puts the finances on an unsustainable path.

Already the Times is reporting that a body of ministers and officials set up to tackle child poverty will recommend lifting the cap after concluding it is the best way to alleviate the problem. Lifting the cap would cost an estimated £3BN a year.

A leftward lurch is underway, and this signals trouble ahead for the UK's finances and the pound.