Image © Adobe Images

The British pound dropped on the inflation release, before finding its feet again.

The pound to euro exchange rate (GBP/EUR) recovers most of the previous day's losses and is back above 1.15 just 24 hours after it was reported UK headline inflation remained stuck at 3.8% in September, defying expectations for a move to 4.0%.

The pound to dollar exchange rate (GBP/USD) edges higher to 1.3350, a 50% recovery of the previous day's post-inflation fall.

Initial GBP weakness reflected a classic FX reaction to a below-consensus inflation reading.

However, we had reported ahead of the release that a below-consensus reading would be undeniably good for an economy flirting with stagflation.

The subsequent decline in UK bond yields meanwhile eases anxieties about the UK's fiscal position ahead of the budget, and this can only be a good thing for the pound.

The recovery in GBP exchange rates bears testament to the glass-half-full approach to the matter.

"It's far too early to say that the UK is 'out of the woods' on the inflation front, but at long last things do seem to be stabilising somewhat," says Michael Brown, Senior Research Strategist at Pepperstone.

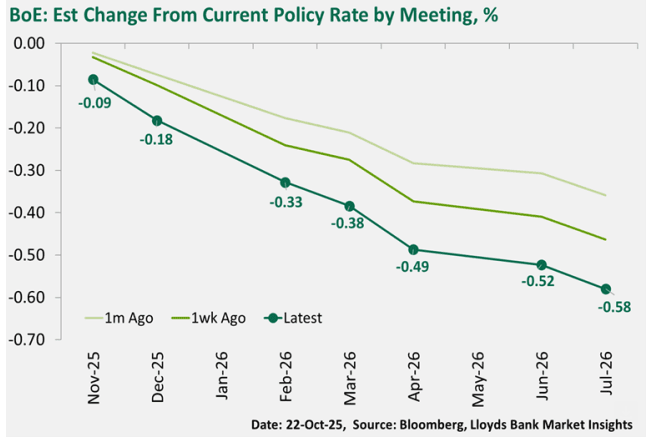

Money market pricing shows investors now see more than a 50/50 chance the Bank of England cuts interest rates by the end of the year.

The rise in bets for a year-end rate cut would traditionally weigh on bond yields and the pound.

However, the prospect of lower interest rates improves the economic outlook and lowers the yield on short-term government bonds, meaning borrowing costs are falling again.

Falling borrowing costs are what the Chancellor of the Exchequer, Rachel Reeves, would like to see ahead of the November 26 budget; not only does it give her more leeway, but it unwinds tension in the market and lessens the odds of a disorderly market reaction to any missteps.

A fading UK risk premium should be evident in a firmer pound.

Another, perhaps contradictory angle to consider is that the scope for the Bank of England to lower rates remains constrained, even if the headline inflation rates undershoot missed expectations.

"Although the September price data was better, we’ve yet to see a sustained turn," says a morning market note from Lloyds Bank.

Crucially, elevated services inflation at 4.7% y/y will mean the headline rate of inflation will struggle to make much progress lower.

It's why some economists think the UK will be encumbered by an inflation rate of above 3.0% well into the middle of next year.

This stubbornness in prices should limit the Bank of England's ambitions as well as the decline in UK bond yields.

"A December cut looks a more reasonable bet, by when changes made by the Budget would be quantifiable. But even then, it would require a further improvement in inflation and continuing tepid demand. It’s hard to see current rate cut pricing extend further from here," says a morning market note from Lloyds Bank.

We would expect the pound to be better supported in an environment in which bond yields remain steady, albeit at levels well below recent peaks.