London, United Kingdom. Chancellor Rachel Reeves delivers a Budget scene setter speech at No 9 Downing Street. Treasury. Picture by Kirsty O'Connor / Treasury

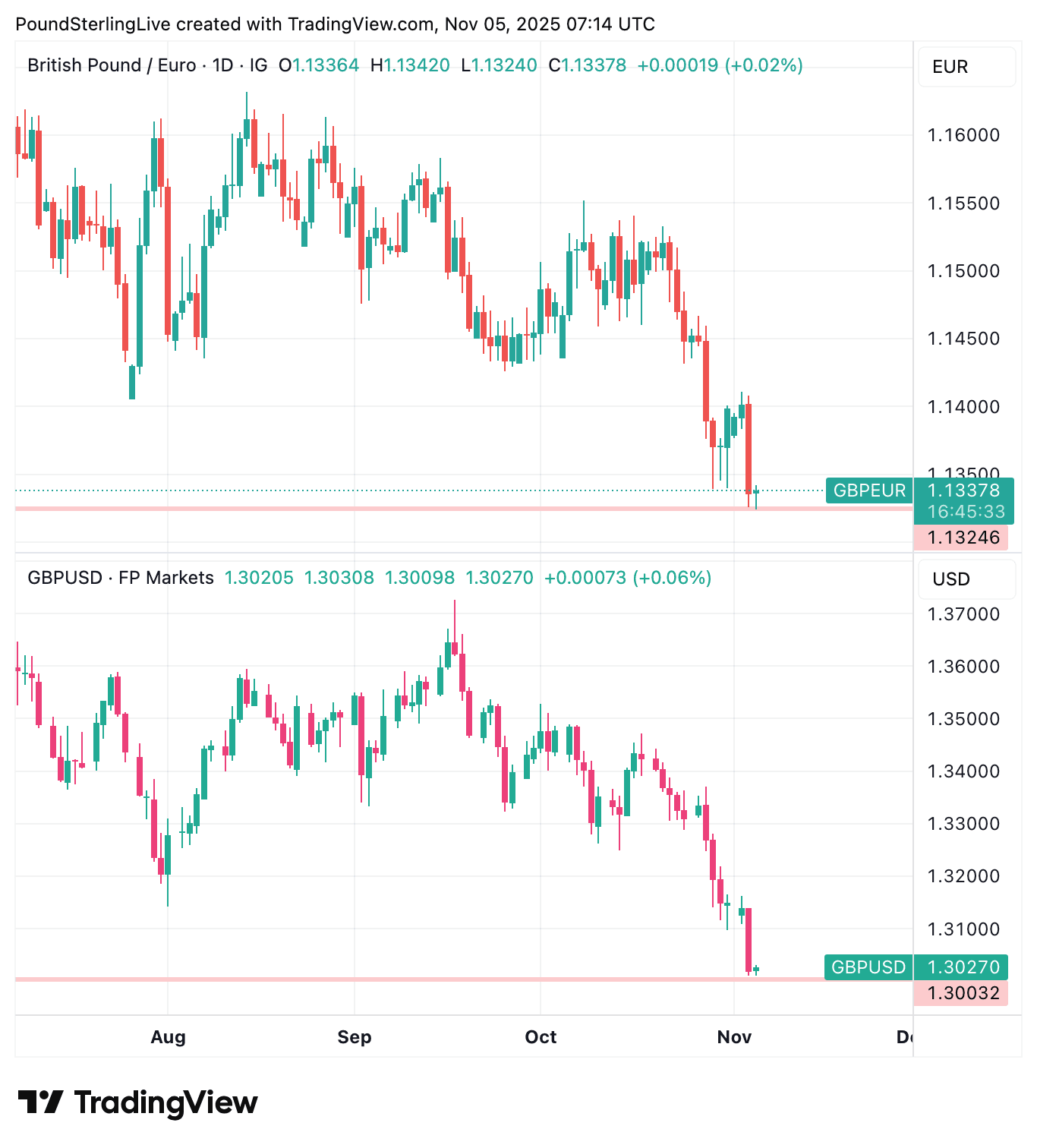

The British Pound teeters at multi-month lows against the euro and dollar.

This is after a new wave of selling pressures followed signs the government is set to announce a significant fiscal squeeze by raising income taxes, which should lower the inflation outlook and open the door for the Bank of England to cut interest rates as soon as Thursday.

Chancellor Rachel Reeves all but confirmed the income tax rise at 11 Downing Street on Tuesday, prompting markets to bet on more rate cuts at the Bank.

UK bond yields fell as a result, mechanically dragging pound sterling lower. "Aside from the UK taxpayer, the biggest victim is the pound," says Kathleen Brooks, an analyst at XTB.

"I must admit I was a little surprised that GBP extended like it did yesterday, there was very little in what Reeves said, maybe it was because of this that the market took it as a bad sign but it is clear to me she will break her manifesto before her fiscal rules," says a note from the trading desk at JP Morgan.

The pound to euro exchange rate (GBP/EUR) fell 0.60% on the day of the Reeves speech and edges to a new two-and-a-half year low of 1.1336 at the time of writing on Wednesday.

The pound to dollar exchange rate (GBP/USD) - also weighed by a stock market selloff - fell nearly a per cent on Tuesday and is little better in midweek trade at 1.3028.

The government is ready to raise income taxes and break its pre-election manifesto pledge that ruled out such a move.

Asked about the promises not to raise income tax, National Insurance or VAT, Reeves said: "as Chancellor, I have to face the world as it is not the world that I want it to be."

News reports suggest the Chancellor will raise the basic rate of tax by 2p, the first such rise since the 1970s.

"A rise in the tax base could make it easier for the Chancellor to build bigger fiscal headroom, the amount that the country has to spare if a crisis hits," explains Brooks.

"The bond market is happy with the government building up the UK’s rainy-day fund, as it makes the debt we need them to buy safer. The question now is, will Gilt yields continue to fall?" she adds.

The question is pertinent to the pound as further falls in gilt yields (UK bond yields) would drag sterling lower.

It's worth pointing out that UK bond yields have been falling faster than in the U.S. and Europe over the course of the past month, which is why the pound has been underperforming the dollar and euro.

This is undoubtedly welcome news to Chancellor Reeves as it means she will be delivering her budget in a far more market friendly environment, which lessens the odds of a disruptive reaction to any mistakes.

However, it appears forex markets are presently more interested in the falling bond yields, and worries about what those tax hikes mean for the economy's growth potential.

Falling short-term bond yields are particularly relevant for the pound. They are a direct reflection on increasing bets that the Bank of England will lower interest rates in response to the government's plan to squeeze workers.

The Bank meets on Thursday and there is 50/50 chance of a cut. But if the Bank decides to hold rates and see what the budget brings, then it will cut in December.

Either way, a cut is coming before the end of the year, and markets are gearing up for it.

"The pound is the UK’s punching bag," says Brooks. "The pound is a harder sell at this point since tax rises could damage the UK’s growth prospects."