Image © Adobe Images

Pound sterling advances against the euro, helped by inflation that's just hot enough to cause too much concern.

The pound-euro exchange rate extends to 1.1530 and takes its daily gain to a quarter of a per cent as London markets close for the day, making this the strongest level for euro buyers since the end of March,

Gains follow news that UK inflation rose to 3.3% in March, as the war in Iran was felt at Britain's fuel stations. That figure met inflation, meaning it hit a sweet spot for the pound: inflation is hot enough to prevent the Bank of England from cutting rates, but not hot enough to signal an ugly period of stagflation is looming.

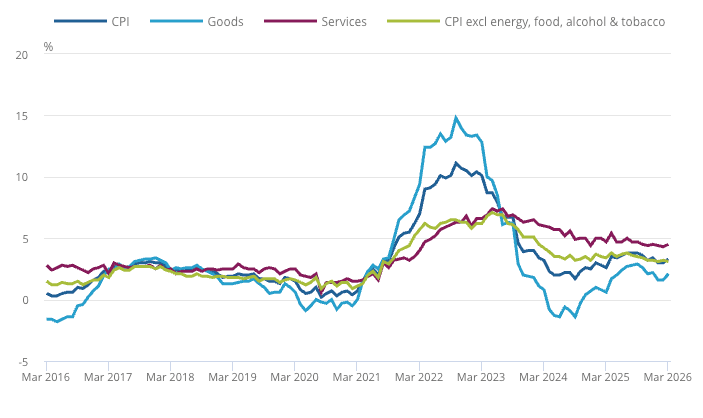

Services CPI rose 4.5% versus 4.3% expected in March, up from 4.3% in February: "The main point of concern will be that services inflation, which is stickier by nature and thus more of a headache for policymakers, rose 0.2ppts to 4.5% y/y," says Sam Hill, Head of Market Insights at LLoyds Bank.

The data will therefore prevent the Bank of England from cutting rates next week and, if anything, increases the prospect of an interest rate rise later in the year.

That's reflected in a tick higher in UK bond yields, which is on balance supportive of pound sterling and helps GBP/EUR exit the very static range of the past three weeks. (By the way, our Q2 GBP/EUR consensus forecasts are out now, offering a solid anchor point for those with upcoming transfers, more info here).

"The Bank of England will stay put when it meets next week. Markets are interested in reaction functions from the ECB and the BoE to help decide on the faith of EUR/GBP," says a note from KBC Bank in Brussels.

Services PMI is arguably the most important figure in today's data batch because it is of particular relevance to the Bank of England.

The Bank knows an inflationary spike will follow the Iran War, which has sent oil and gas prices soaring. But there's little it can do about that.

Instead, it's services and core inflation that will matter for the Bank of England; these are the elements of inflation that are determined by the domestic economy, and changing interest rates can have an impact.

Above: Stubborn services CPI limits headline CPI's ability to fall to the 2.0% target.

That services inflation was hotter than expected will be of concern and will warn the Bank that domestic prices could follow energy prices higher in the coming months. That raises the risks of another embedded inflationary surge.

To be sure, core CPI edged lower to 3.1% from 3.2%, which was softer than consensus estimates for 3.2%.

Bottom line, though, is that these figures are all far too high for the Bank to consider cutting interest rates, particularly given the recent above-consensus GDP and labour market prints.

For the pound, today's numbers are ultimately supportive inasmuch as they suggest UK rates will remain higher for longer.

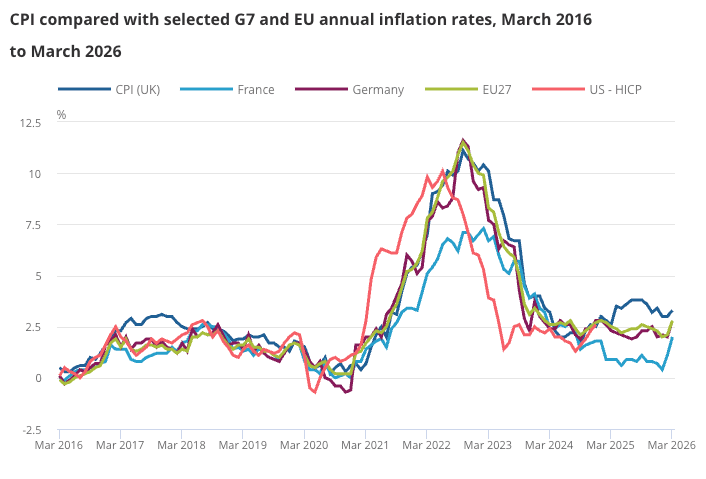

Above: The UK has elevated inflation relative to comparable economies. This implies the Bank of England can't cut faster than peers, and that should ultimately prove supportive for GBP.