Image © Adobe Images

Pound Sterling has erased losses against the Euro and Dollar thanks to a recovery in U.S. stock markets.

Although today has the European Central Bank (ECB) interest rate cut pencilled in as the highlight for the Pound to Euro exchange rate, evidence suggests it is the performance of U.S. stock markets that could matter more.

On Wednesday, GBP/EUR experienced a sudden plunge in early afternoon trade, with the culprit for the fall being a dip in U.S. stocks.

We noted that the Pound was the day's second-worst performing major currency, with only the New Zealand Dollar doing worse. We note the common link between the GBP and NZD is they share the highest central bank interest rate in the G10 after the USD.

This makes them receievers in the carry trade, where investors borrow in low interest rate currencies to earn interest in higher interest rate currencies. Often, the carry trade can reverse when market volatility rises, resulting in losses for higher-yielding currencies.

Yesterday's fall in the U.S. market looks to have presented such an episode, and GBP and NZD lost ground. But, a late-session recovery ultimately picked them off the floor. "US equities erased an early fall to finish in the green, buoyed by the usual mega-cap tech names," says Jameson Coombs, an analyst at Westpac.

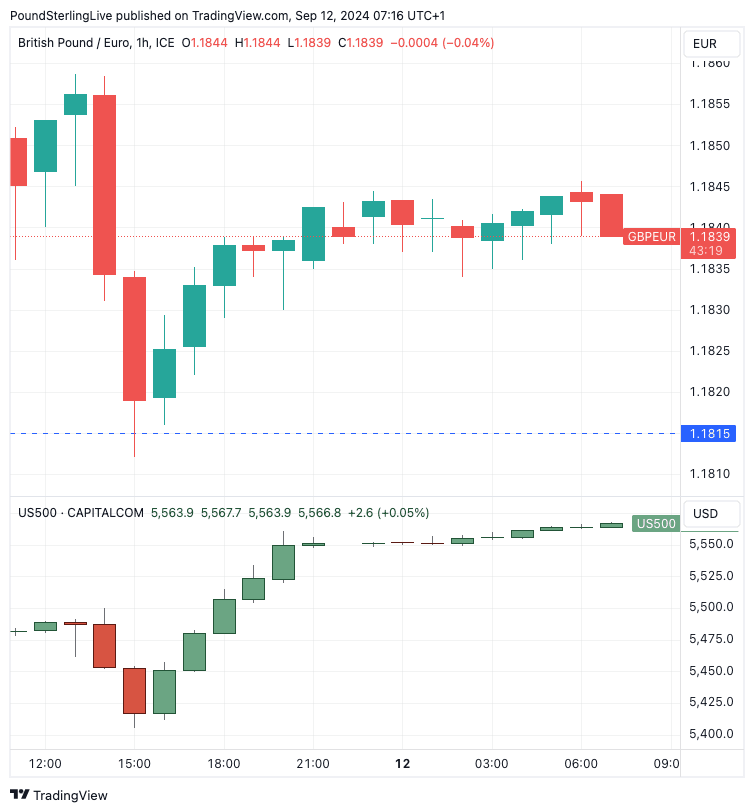

The GBP to EUR exchange rate recovered from a daily low at 1.1812 to close at 1.1840 as the S&P 500 recovered to 5551 from an earlier low of 5405 before:

Above: GBP/EUR (top) and U.S. S&P 500.

The S&P 500's performance, therefore, matters for Sterling via the risk sentiment channel. Some key GBP exchange rates are clearly tracking risk, and we think how the remainder of September pans out for the U.S. market will determine how resilient GBP/EUR is.

With this in mind, there is some constructive news for those wanting a stronger Pound against the Euro: economists at Capital Economics reckon the S&P 500 can put in a decent rally in the coming months.

John Higgins, Chief Markets Economist at Capital Economics, says it's possible that the bubble in Artificial Intelligence (AI) equities has burst and that the U.S. stock market’s broad-based strength will end soon.

"Nonetheless, this isn’t our baseline scenario, partly because demand for AI hardware doesn’t seem to be waning and partly because we continue to forecast a soft landing for the US economy. We are therefore sticking to our forecast for the S&P 500 to end this year at 6,000," he says.

If GBP/EUR continues to track the S&P to such a height, and the Bank of England retains a conservative stance towards cutting interest rates, then the exchange rate can potentially end the year above 1.20.