It was back in November when the Bank of England last released economic projections and held a press conference. Image Bank of England.

The British Pound's recovery against the Euro, Dollar and other major currencies risks a setback today.

This is because the Bank of England will cut interest rates and indicate it is ready to cut rates on a regular basis in the coming year.

The market expects a 25 basis point cut to Bank Rate and two further cuts in 2025. However, the Bank will try and commit to at least three further cuts to maintain its quarterly pace to the cutting cycle.

"We view a background of lacklustre growth to be consistent with the MPC bringing the Bank rate down four 25bp times in total this year, to 3.75%," says Philip Shaw, an economist at Investec.

A market readjustment towards an additional three cuts will mechanically weigh on UK bond yields and the British Pound.

"While we expect the MPC to maintain its gradual approach to policy easing, we anticipate some language tweaks to reflect growing downside risks, which could weigh on the pound in the short-term," says Jane Foley, Senior Foreign Exchange Strategist at Rabobank.

This would dent a short-term recovery in some key Sterling exchange rates: the Pound to Euro exchange rate is quoted at 1.2020, having been as low as 1.18 in mid-January; the Pound to Dollar exchange rate has recovered from 1.2099 on January 13 to 1.2485.

"If the BoE are a little more dovish than market expectations, GBP/USD can fall towards support at 1.2415," says Carol Kong, a foreign exchange strategist at Commonwealth Bank of Australia.

"While investors have moderated their long GBP positioning, it is still relatively optimistic compared to non-USD peers, leaving it vulnerable to further correction and any dovish lean from the BoE," says James Rossiter, Head of Global Macro Strategy at TD Securities.

TD Securities anticipates an approximate 0.15% decline in Pound Sterling under its base case scenario.

It is anticipated that an easy majority of the Monetary Policy Committee (MPC) will vote to cut Bank Rate, with one, Catherine Mann, instead opting to keep it unchanged at 4.75%. The decision will follow the unexpected news UK CPI inflation rose 2.5% in the 12 months to December 2024, down from 2.6% in November, undershooting a consensus estimate for a rise to 2.7%.

The Bank will release new economic forecasts showing a cut to growth projections and a rise in unemployment forecasts, underpinning its message that it needs to continue cutting interest rates.

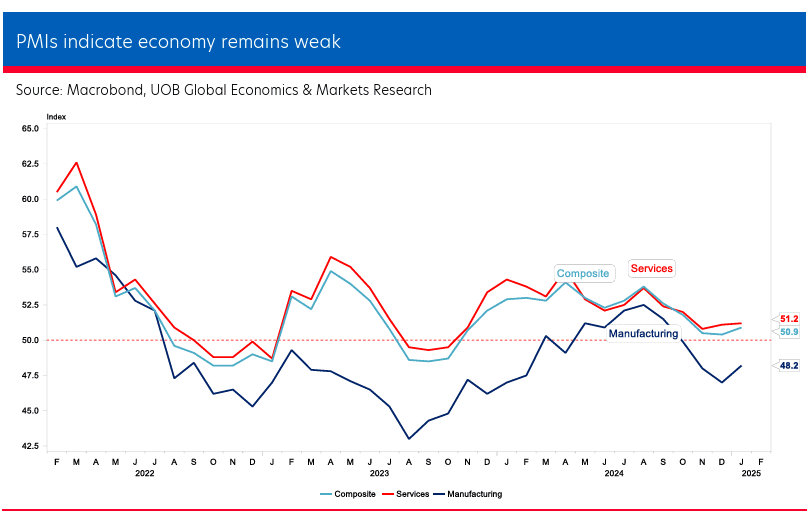

Above: Surveys show UK economic activity has fallen sharply, limiting the Bank's scope to cut interest rates. Image courtesy of UOB.

"Any further shift in focus towards growth rather than inflation could penalise GBP similarly to December," says Patrick R Locke, an analyst at JP Morgan.

However, inflation forecasts are also expected to be lifted, complicating the outlook and limiting the potential for the Bank to be as 'dovish' as it would like, given the growth slowdown. After all, its main objective is to tackle inflation, and cutting interest rates is an inflationary act.

While the labour market is loosening, wage growth also remains high and will rise further in April when minimum wage rates increase, which is a concern for the Bank as wage increases can tend to fuel inflation.

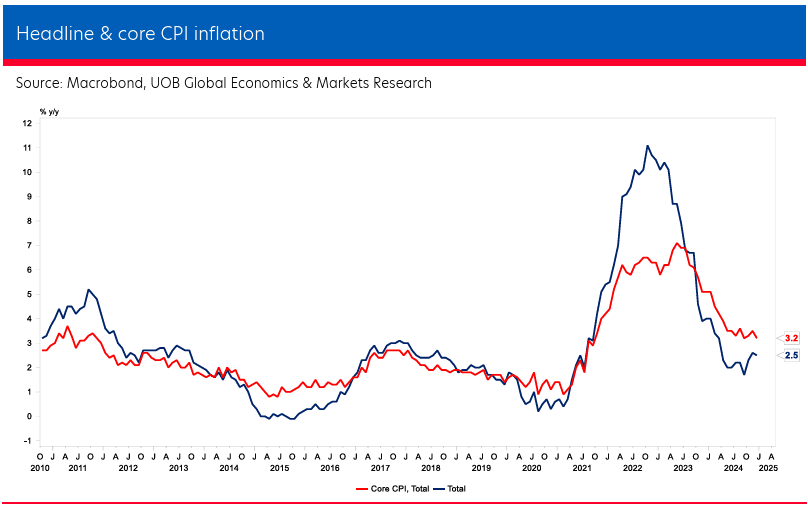

Above: Inflation is above the 2.0% target and the downward trajectory has stopped, limiting the Bank's ability to cut rates. Image courtesy of UOB.

Economists at JP Morgan expect the Bank's economists to revise near-term growth forecast on net (from 1.5% to 1.1% in 2025), with the overall inflation outlook likely to be higher than previously thought, at least in the near term part of the forecast.

The language of the statement will be important.

"If they were to remove the word 'gradual' (not our base case), this would allow rates and FX markets to interpret that they are stepping up the easing pace (the MPC has defined 'gradual' as 100bp this year; the market is pricing 75bp), but they are likely to be wary of sending a dovish message to markets, and current data does not require urgency," says Locke.

Pound Better Protected

The Pound fell notably in the first half of January as financial markets adjusted to the UK's deteriorating economic outlook. This means that some of the negatives in the Bank's forecast downgrades are 'in the price' of the currency.

This adjustment from 2024 highs lowers the downside risks for the currency heading into the event as some excessive positioning will have been cleaned out.

"Volatility should be more muted by dampened GBP sentiment already priced in," says Sarah Ying, Head of FX Strategy at CIBC Capital Markets.

The dovish tones in today's event should dent pound exchange rates in the near term, but the impact won't be lasting, and there is scope for further recovery throughout February amidst an easing in the broader dollar.