Above: File image of Chancellor Rachel Reeves, with the Governor of the Bank of England Andrew Bailey. Picture by Kirsty O'Connor / Treasury.

Analysts sniff the potential for a surprise this Thursday.

The Bank of England interest rate meeting is widely anticipated to see a 25bp cut to 4.25%. However, some analysts see the prospect of a more aggressive move.

Why? What has caught the eye of Bank of England watchers is an unusual number of Monetary Policy Committee members being wheeled out to give speeches in the aftermath of the decision.

"May be doing 2+2 = 5 here on the BoE, but feels significant that we have Bailey & Pill both speaking on Friday...then on Monday you've got Lombardelli, Greene, Mann & Taylor... for an MPC that never speaks much to have six speeches in two days seems notable," says Michael Brown, Senior Research Strategist at Pepperstone.

Typically, the lineup of speakers would be spread out over the coming weeks. If the Bank were to cut by 50 basis points, then it would need to deliver a strong message and narrative for the move.

This is because the cut would come in an environment of rising inflation that is taking the Bank ever further away from its 2.0% target.

A 50bp move would therefore put its credibility at risk and require some serious 'spin' from policymakers to sell the decision.

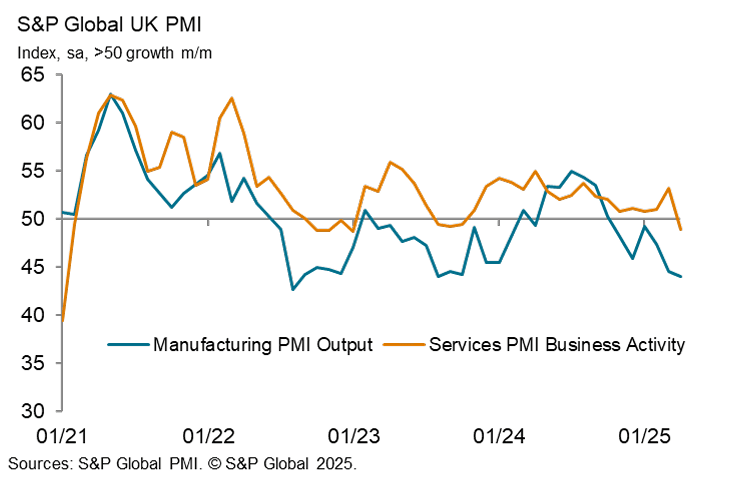

Above: The UK economy showed a sharp decline in April according to the PMIs, which might convince the Bank of England it needs to be more supportive and cut rates deeper and faster.

For the British Pound, a 50bp cut would be a surprise and would lead to an initial sharp downward adjustment.

Pound Sterling could soon recover those losses if the markets read that the 50bp was a preemptive move that lessened the need for additional cuts later on.

Shaun Richards, an independent economist and adviser to pension and investment funds, is a noted Bank of England watcher. He says:

"It looks as though we are being warmed up for a sequence of interest-rate cuts. In my opinion, there are problems with this, such as the relative strength of money supply growth. Plus the reality that the April inflation reading will be above 3% and maybe well above."

A "sequence of rate cuts" suggests that even if the Bank forgoes a 50bp cut on Thursday, it will signal it is ready to quicken the pace at which it cuts from once a quarter to consecutive cuts.

This puts a June cut in scope, and could be why there will be a barrage of messaging from MPC speakers in the following days.

More rate cuts, delivered faster, would weigh on the Pound.

"A more dovish policy update from the BoE could deliver a setback after the recent GBP rebound, although recent dovish repricing should help to dampen any GBP sell-off if there is a moderate change in guidance," says Lee Hardman, FX Strategist at MUFG Bank Ltd.

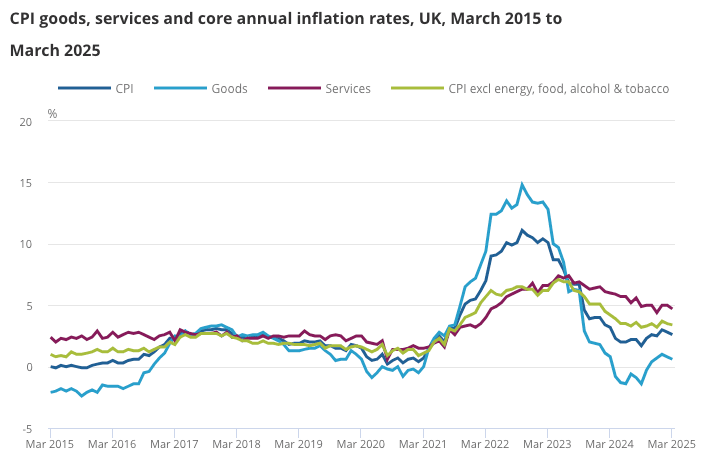

Above: Until services inflation falls more meaningfully it will be difficult to bring headline inflation down to 2.0% sustainably.

However, economists warn the Bank risks its reputation by trying to boost growth by cutting interest rates at the expense of its inflation mandate.

"The Bank of England has shifted its focus to economic growth and will yet again take risks with inflation," says Richards.

Andrew Sentance, former member of the Bank of England's Monetary Policy Committee, thinks now is not the time to be cutting interest rates as he forecasts inflation to rise to 4-5% in the months ahead.

Higher business National Insurance contributions are seen as a significant driver of costs facing businesses, which are anticipated to be passed on to consumers.

Sentance says core and services inflation remain stubbornly high and will be hard to budge. Until services inflation begins to fall meaningfully, the Bank will ultimately fail to bring inflation back to target.

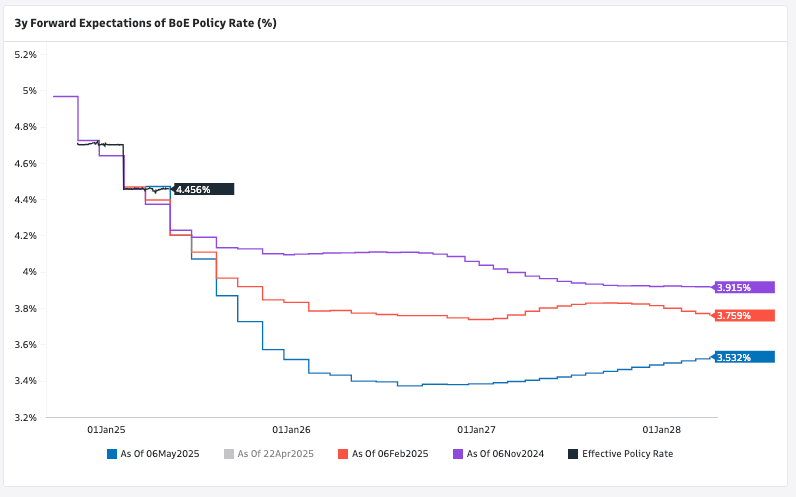

Above: Markets have steadily increased bets for a deeper interest rate cutting path since the end of 2024, which limits the downside potential for the GBP as the adjustment has largely taken place.

Persistent and high wage rises are underpinning this services-side inflation, to a significant degree.

Food prices are meanwhile anticipated to start rising again, bringing to an end a spell of negative food price inflation that has helped the Bank of England of late.

Sentance also notes that public spending and borrowing will stay generous, thus boosting demand.

"MPC should not cut interest rates this week despite Trump’s tariffs," he says.

"Sterling will derive support if the BoE continues to signal that it is content with the current quarterly pace of rate cuts. This comes as financial market volatility continues to ease against a backdrop of stronger investor sentiment around the scope for post-‘Liberation Day’ trade deals," says Hardman.