Image © Adobe Images

The New Zealand Dollar is firmer at the start of the new month.

Although the Kiwi is making fresh advances against the Pound, we are looking for GBP/NZD upside to resume.

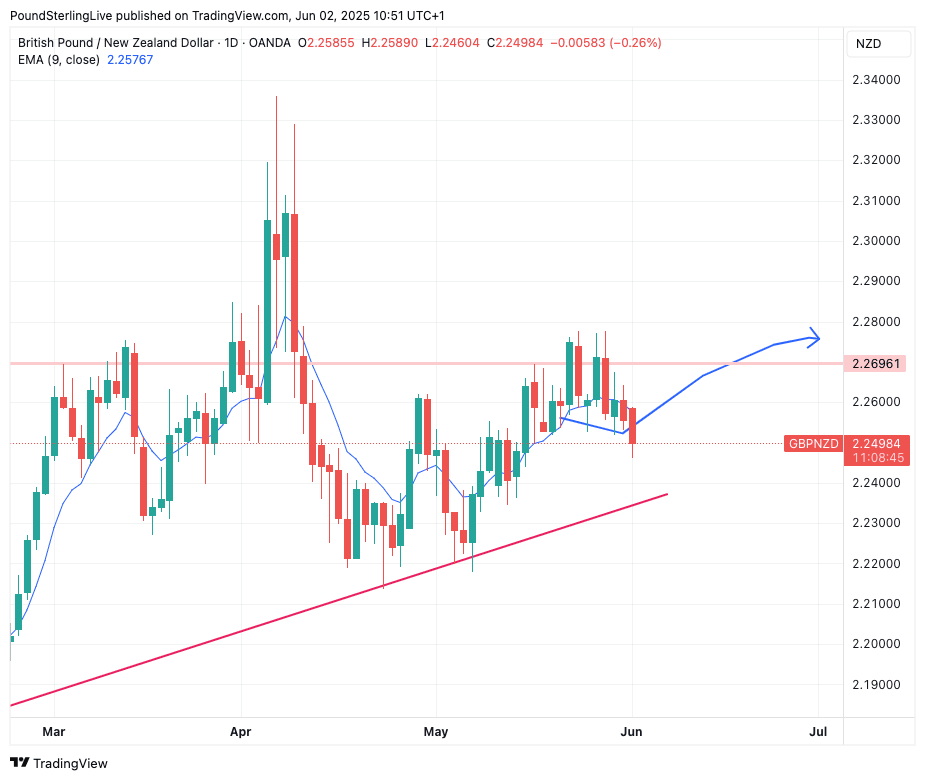

The below chart shows annotations made in our Week Ahead Forecast from two weeks ago. We looked for a pullback and for gains to then resume.

Above: GBP/NZD at daily intervals.

We see little reason to alter that setup at this point, judging that the thesis remains relevant. However, calling a pullback was the easy bit; judging the turnaround is the harder bit!

Monday's setback in the exchange rate is consistent with it being capped by the nine-day exponential moving average (EMA), which is now pointed lower, meaning it will drag on the conversion.

It will take a decent impulse of GBP buying to get GBP/NZD back above this trend line level and into a renewed short-term uptrend.

Will we get that today? Of course, it would be folly to make such a call, and there is the chance that the GBP/NZD pullback extends right back to the rising trendline that defines trade this year (as per the chart, this would allow the pullback to extend towards approximately 2.24.

Should GBP/NZD break below this level, then a deeper decline becomes viable and we would look to question whether the 2025 rally has finally come to an end.

For now, we lean against that notion given the renewed uncertainty pertaining to global trade, which is a natural support for Pound-Kiwi.

Following the market close on Friday, President Trump announced a doubling of tariffs on steel and aluminium imports from 25% to 50%, citing national security and job protection. These tariffs are set to take effect on June 4, 2025.

He then accused China of violating a recent trade agreement by not adhering to commitments, particularly concerning the export of critical minerals. In response, the U.S. reinstated higher tariffs on certain Chinese goods.

"Markets were once again caught in the vicious loop of trade war escalation and de-escalation overnight on the back of worries that trade tensions are on the rise again between the US and China," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole.

Official White House Photo by Carlos Fyfe.

The New Zealand Dollar is particularly sensitive to headwinds facing China, owing to the tight trade linkages between the two countries.

Interestingly, the NZD is gaining despite the current flare-up in trade tensions, which could mean markets are becoming less sensitive to Trump's rhetoric.

"The tariffs theme has peaked and there is clearly less and less reaction to each tariff headline. The tariffs are going up and the tariffs are going down, but people are getting bored of it," says Brent Donnelly, analyst at Spectra Markets.

Under such a development, GBP/NZD might struggle to regain its uptrend.

Our stance is that it's too soon to sound the all-clear for the NZD by way of global tariff risks and a reversion to the 2025 playbook is still likely, opening the door to a resumption in GBP/NZD upside.

This week is devoid of major data releases in both the UK and New Zealand, meaning direction will be influenced by the background mood music concerning trade and the U.S. economy.

Bear in mind we have ISM survey data from the U.S. due on Monday and Wednesday, which could set the tone if it is shown that tariffs are starting to have a meaningful impact on activity.

However, it's Friday's U.S. job report that could prove the biggest event of the week: any disappointments here could hurt stock markets, which would be reflected in a weakening NZD.

"The market is expecting a sharp slowdown in job creation for last month, as the labour market starts to crack under the weight of weak consumer and business confidence as tariff uncertainty weighs on the US’s economic prospects," says Kathleen Brooks, an analyst at XM.com.

The consensus looks for a 125k gain in payrolls for May, with a drop in private sector payrolls, and signs that jobs are being lost in the manufacturing sector. The unemployment rate is expected to remain steady at 4.2%.

"If the unemployment rate ticks up more than expected, we think the market reaction could be swift. The dollar is likely to fall, and the bond yields too, as the market rushes to price in rate cuts from a data-dependent Fed," says Brooks.