Image © Adobe Images

The Pound to New Zealand Dollar exchange rate (GBP/NZD) is forecast to retain a broadly constructive tone.

The pair lifted sharply last Friday after the New Zealand Dollar proved to be the big loser after Iran and Israel attacked each other, confirming this is one of the more sensitive global currencies to sentiment.

The market mood is much improved on Monday, despite no clear resolution to the conflict, which tells us markets assess that the prospect of a real escalation remains limited.

Oil prices, the ultimate gauge of temperatures in the Middle East, surged on Friday but are falling on Monday, with oil analysts expecting a return to recent levels in the coming days and weeks.

This is good for stock markets and will weigh on the Dollar, which is giving the Kiwi Dollar a helping hand, and justfies our warning in Friday's coverage that the NZD stands to be the biggest winner in any bounceback in sentiment.

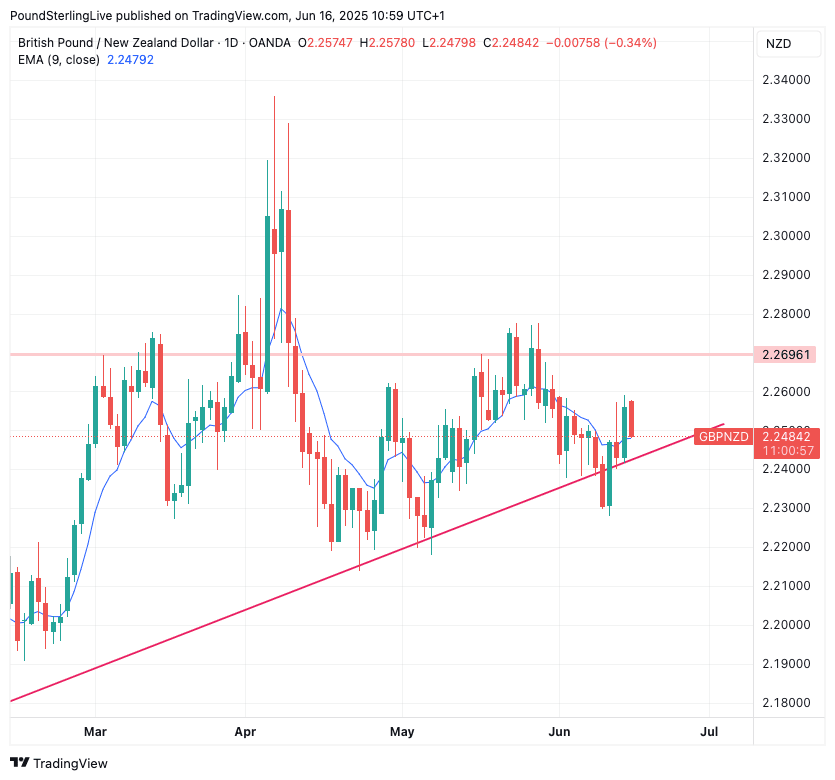

We see this recovery reflected in a big red candle on the daily chart, taking GBP/NZD back to the nine-day exponential moving average:

Above: GBP/NZD at daily intervals showing the intact uptrend. However, the trend risks breaking down and giving way to an irregular sideways move.

This level can offer the GBP/NZD some near-term support, which, if held, would keep a soft drift higher intact. This would also keep the pair above the rising trend line (red line in the chart).

Notably, last week's break below the trend was a false one, confirming there is some predictive utility in keeping an eye on this marker.

If the trend can hold, then a move to 2.2696 is in play for the coming days.

This target would be likely if Iran and Israel continue to hammer away at each other, with Iran offering enough threats to keep risk sentiment in check. We just don't see the NZD excelling under such circumstances, meaning the easiest course for GBP/NZD to take is higher.

In New Zealand, Tuesday sees the release of the Selected Price Indices for May, which should give a snapshot of inflation trends and allow economists to adjust their predictions for the next quarterly release.

April’s update on consumer prices was stronger than expected, with continued large increases in food prices and a sharp rise in airfares. Some of the gains seen in April were seasonal (e.g. international airfares), and some give-back is likely in May.

"However, we’re continuing to see gains in areas like grocery prices, with overall food prices expected to be up another 0.2%. It’ll also be worth watching what happens to rents (the largest component of the CPI), which have recorded relatively small increases in recent months," says a weekly preview note from Westpac.

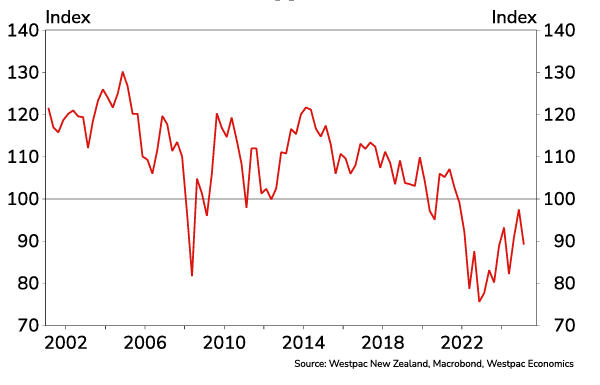

Above: Kiwi consumer confidence is yet to make a material turn for the better.

On Wednesday, the Westpac-McDermott Miller Consumer Confidence Index is updated, and analysts at Westpac say that while consumer confidence has picked up from the lows we saw in recent years, there are a range of concerns that are still worrying New Zealand households, and that’s likely to be a brake on spending for a few more months at least.

The question is to what extent these readings will prompt markets to bet on deeper interest rate cuts at the Reserve Bank of New Zealand? Given these are second-tier data releases, the answer would have to be minimal.

That being said, they will give us a useful insight into whether or not recent interest rate cuts are impacting the economy.

In the UK, the Bank of England will meet on Thursday and maintain interest rates at current levels. However, readers should expect policymakers to address the recent set of soft employment figures and GDP numbers, potentially signposting an August rate cut in the process.

The market raised the odds of an August rate cut following last week's labour market and GDP numbers, which mechanically weighed on domestic bond yields and the Pound.

However, an adjustment in expectations is now arguably fully 'in the price' of the Pound, and for this reason, we don't think the moves in GBP/NZD following Thursday's update will be massive.

Another potential event worth keeping an eye on is the midweek Federal Reserve decision. Like the Bank of England, the Fed won't change rates, but could offer useful guidance.

Don't expect a massive market reaction as this 'place-holder' meeting will see the Fed try to keep expectations unchanged as there is still a lot of uncertainty it would like to ride before committing to further policy action.

That being said, if the Fed can bolster market spirits, then equity markets can rise, and so too can assets that are positively correlated. Of course, this would include the Kiwi.

In short, a good week for global stocks could keep the NZD on the front foot and stymie our expectation for a rally in GBP/NZD.