Image © Adobe Images

Hopes for Chinese stimulus and numerous Federal Reserve rate cuts boost NZD.

The New Zealand Dollar is outperforming G10 peers thanks to an ongoing rise in risk-sensitive assets linked to developments in China and the U.S.

"The prospect of the Fed cutting rates by 125-150bp over the next nine months can only support leverage and demand that asset managers remain fully invested to earn their fees," says Chris Turner, chief FX analyst at ING Bank N.V.

The New Zealand Dollar is highly sensitive to global sentiment, and the environment of rising stocks, fuelled by the hope for lower U.S. interest rates, proves supportive.

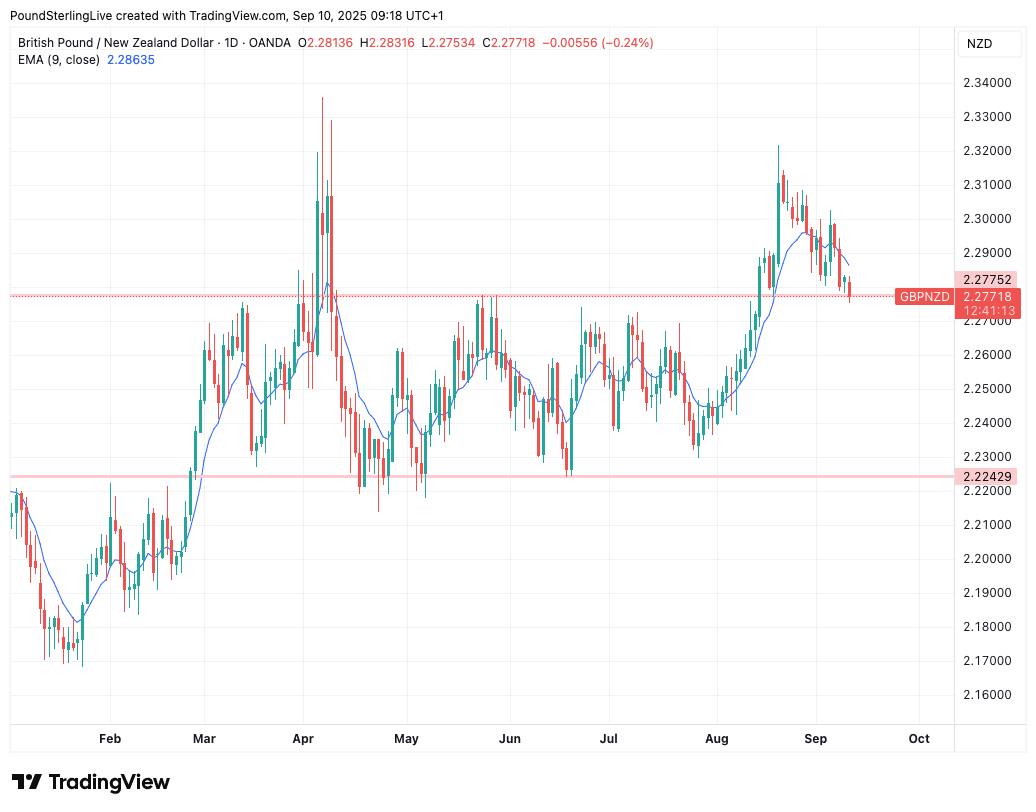

Against the Pound, the Kiwi extends its gain by a quarter of a percent, pushing GBP/NZD down to support at 2.2746. EUR/NZD looks for a fourth consecutive daily decline as it plumbs 1.9695, and NZD/USD rises to 0.5940.

Risks to the NZD's strength come later on Wednesday when U.S. PPI inflation numbers are released, as a strong figure could diminish expectations for future Fed rate cuts. But the real test comes Thursday, when headline inflation figures are released, with analysts looking for CPI to rise to 2.9% y/y.

But it's not just the U.S. that is offering the New Zealand currency support: China's below-expectation inflation figures released midweek raise the prospect of further stimulus measures in the world's second largest economy.

Above: GBP/NZD at daily intervals.

This is undoubtedly supportive of New Zealand, which counts China as its largest export customer.

"China's economy has slowed since the start of 3Q25, prompting calls for the PBOC to cut interest rates as early as this month," says Ho Woei Chen, economist at United Overseas Bank in Singapore.

Hopes for further Chinese stimulus rose after the country reported PPI inflation fell 2.9% y/y in August, after dropping 3.6% in July.

CPI inflation declined 0.4% y/y in August, which was down from 0.0% in July and well below consensus estimates for -0.2%.

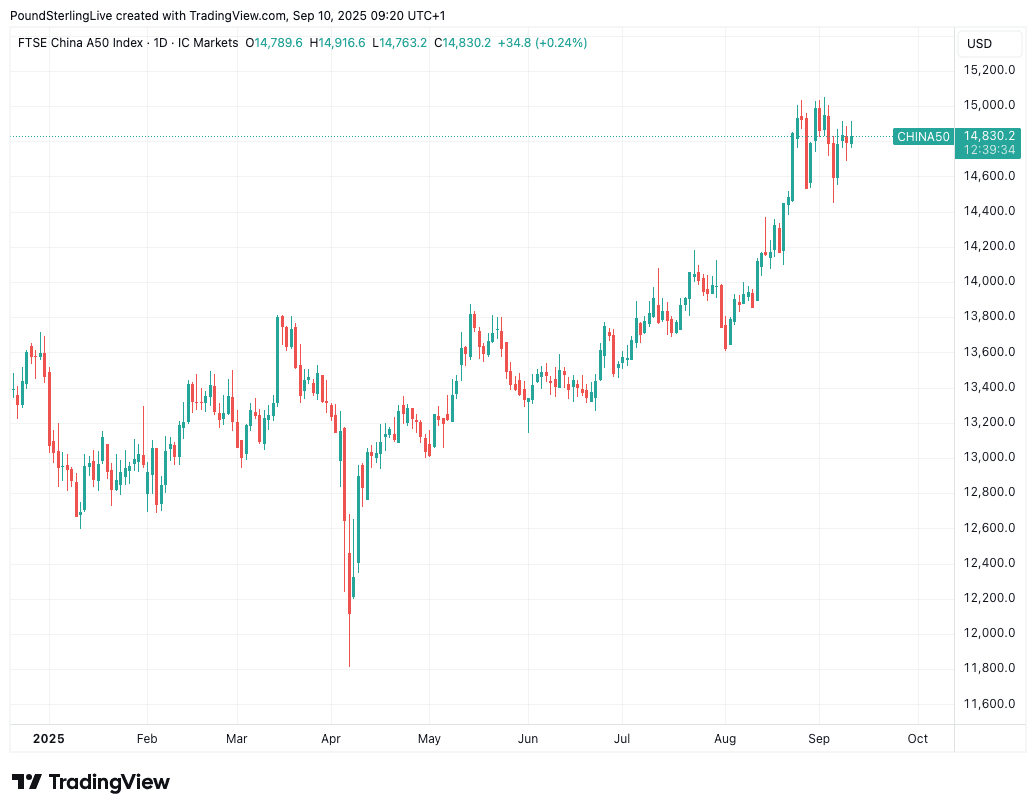

Expectations that a boost to Chinese demand will rev up the economy are driving a surge in Chinese stocks.

Over 90% of companies in the MSCI China index have reported Q2’25 earnings, according to Bloomberg. Q2 earnings per share grew by 8.7% y/y, supported by +3.4% sales growth.

"We are bullish Chinese equities over a 12-month horizon," says Jason Wong, Equity Analyst at Standard Chartered.

The rally in the country's equity market is one of the more surprising aspects of 2025's market landscape, as it speaks of resilience to U.S. import tariffs.

Above: China 50 index.

It also speaks of ongoing measures by authorities to transition China from an export-oriented economy to one that runs on its own demand.

The stock market rally is helping an ongoing recovery in the Chinese Yuan, now at ten-month highs, which itself has often had a supportive bearing on antipodean currencies such as the New Zealand and Australian Dollars.

The only rub for the Kiwi is the domestic economy which continues to disappoint and speaks of a need for further interest rate cuts at the Reserve Bank of New Zealand (RBNZ).

Expectations for further RBNZ rate cuts will prove a limiting factor for NZD upside and should serve to cap the globally-inspired rally we are witnessing this September.