Image © Adobe Images

The pound looks to recover from a soft spell against the New Zealand Dollar.

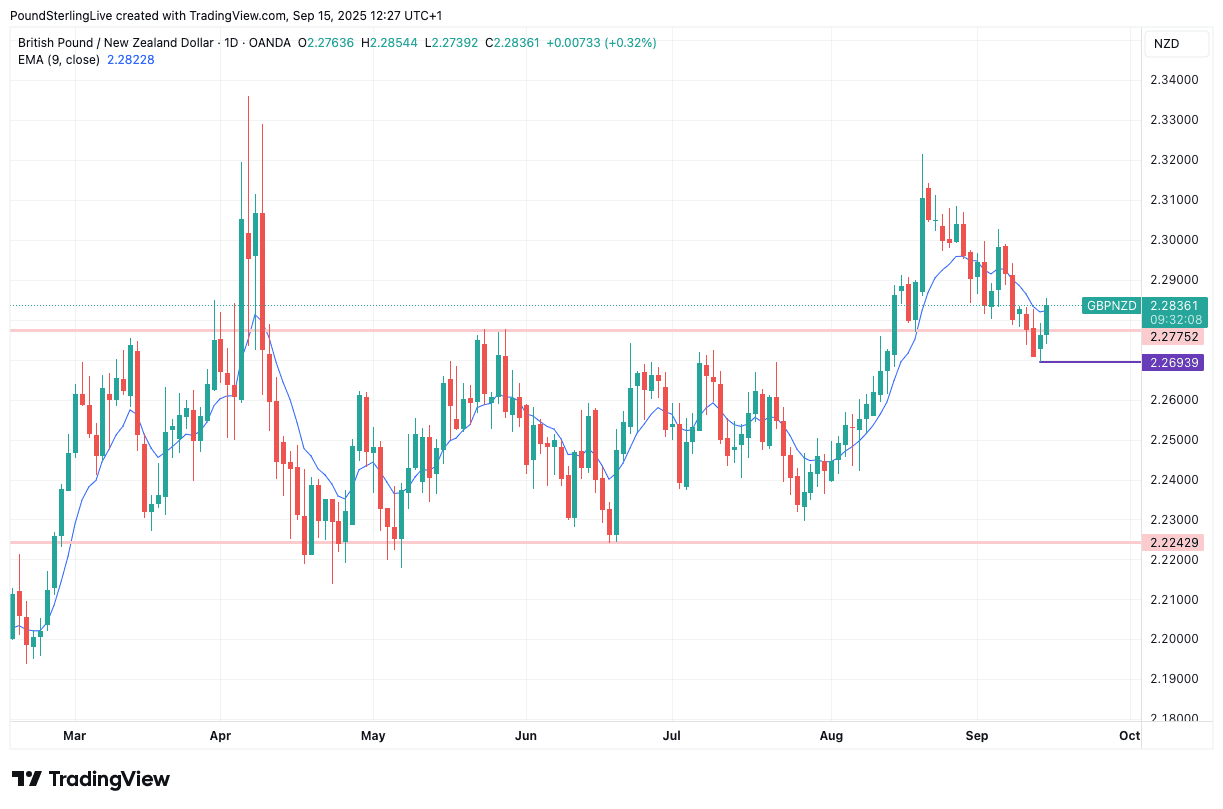

Monday sees the pound to New Zealand Dollar exchange rate (GBP/NZD) rise to 2.2841, having been as low as 2.27 on Friday, in what could be an attempt to arrest the recent selloff.

It's been downhill travel for the pair since mid-August when it topped out at 2.32, with losses being primarily driven by outright NZD strength.

That NZD strength is a combination of technical recalibration following a bruising selloff and a supportive global backdrop: AUD, NZD and other global-facing currencies have had a good spell of late, driven in part by rising expectations that the Federal Reserve will kick off a round of interest rate cuts, starting this Wednesday.

Expectations for a generous spell of cuts in the world's biggest economy could yet deliver further NZD gains, although there is also a strong chance that this trade fades.

After all, pricing for generous cuts is significant and the bar to keep that train rolling forward is now incredibly high. If the Fed cuts rates but urges markets to be more cautious in their expectations for future cuts, then the NZD and other assets that have done well of late could unwind gains.

This opens the door for GBP/NZD to recover further, thereby establishing a decent level of support in the 2.2693-2.2752 zone:

Note the attempted breach of the nine-day exponential moving average (EMA) - the blue line - in the chart; if the level is broken and held the near-term picture turns constructive and we would anticipate gains towards 2.30.

However, a failed break and a reboot of the 'risk on' trade could potentially trigger another round of GBP/NZD weakness that takes us back down into the main 2024 range that exists below 2.275 and above 2.2242.

NZD weakness at the start of the new week also reminds us that China is an important factor in understanding what makes this currency tick.

China on Monday reported a slew of disappointing economic numbers that has weighed on China-focussed assets, such as NZD and AUD.

Authorities reported an above-expectation increase in the unemployment rate of 5.3%. Industrial production disappointed at 5.2% y/y, massively undershooting the conesensus bet for 5.7%. Retail sales missed at 3.4% vs. 3.8% expected and new home prices fell 0.30% m/m in August, after dipping 0.31% in July.

So we have disappointing consumer-facing and industrial numbers, which speaks of a broadly soft summer for the world's second-largest economy.

"China's extended summer slowdown will trigger calls for more stimulus, though the NBS is likely to brush it off by blaming the weather. Note the two monthly indicators closely linked to the NBS’s GDP estimates, industrial output and services output, are still growing above 5%, meaning the official GDP growth could still be above 5% in Q3. Still, we think China will opt for further targeted support to counter downward forces," says Duncan Wrigley, Chief China+ Economist at Pantheon Macroeconomics.

We continue to think that one fundamental development that must occur for the market to turn more constructive on NZD is a decisive turn in China's economy. Until then, the big-picture selloff that has taken it to the lowest levels since 2016 against the pound can continue.

GBP will have an important role to play in NZD direction this week. Tuesday's labour market statistics will likely show a further deterioration in payrolled employment and slowing wage pressures, all of which should lean on the pound as it would encourage the market to raise odds of a future Bank of England interest rate cut.

However, given that the UK's employment data has become highly unreliable, we imagine any GBP reaction will prove limited, with markets storing their gunpowder for the following day's inflation print.

On Wednesday, UK CPI inflation for August is expected to remain steady at 3.8%, in line with the Bank’s forecast, yet still well above the 2% target.

This should mean Thursday's Bank of England interest rate decision offers minimal fuel to fire up rate bets, ensuring UK short-term interest rates remain well supported relative to those in New Zealand, thereby underpinning GBP/NZD.