Image © Adobe Images

The New Zealand Dollar outlook remains prone to further interest rate cuts from the Reserve Bank of New Zealand (RBNZ).

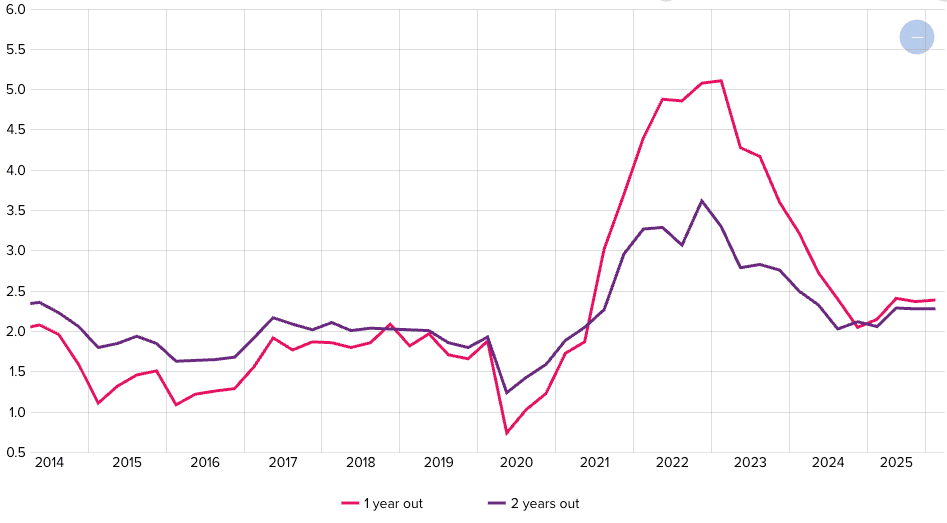

This is the assessment following the release of the latest findings of the RBNZ's inflation expectations survey, which is key to informing its understanding of how the economy's inflation profile will evolve.

One-year-ahead inflation expectations edged up to 2.39% (from 2.37% in Q3), and two-year expectations are holding steady at 2.28%.

Longer-term expectations remained near the midpoint of the RBNZ’s 1–3% target range, with five-year expectations at 2.22% and ten-year at 2.18%.

The headline takeaway is that inflation expectations remain well anchored, which implies limited scope for upside pressures, allowing for further interest rate cuts.

More cuts are, on balance, a headwind to the NZ Dollar, which is already one of the poorer performing of the world's major currencies in 2025.

Economists at ASB say the RBNZ "will be somewhat reassured" that expectations have not risen in step with the latest CPI print of 3.0%.

Money market pricing shows investors are 15% priced for another jumbo-sized 50bp rate cut by the RBNZ on 26 November.

"The RBNZ needs tame inflation expectations to further aggressively cut rates in order to revive growth. So Tuesday’s inflation expectations data will be important for the NZD," explains David Forrester, FX analyst at Crédit Agricole.

“Inflation expectations were little changed despite higher headline inflation and the 50 bp October OCR cut,” wrote Mark Smith, Senior Economist at ASB.

He added that the contained readings “suggest that the RBNZ will be able to ‘look through’ the near-term spike in inflation and focus on medium-term inflation drivers.”

The survey, conducted between 21 and 28 October, found one-year-ahead inflation expectations edging up to 2.39% (from 2.37% in Q3) and two-year expectations holding steady at 2.28%.

Longer-term expectations remained near the midpoint of the RBNZ’s 1–3% target range, with five-year expectations at 2.22% and ten-year at 2.18%.

ASB said the RBNZ “will be somewhat reassured” that expectations have not risen in step with the latest CPI print of 3.0%.

"We are confident that the Q3 lift in headline CPI inflation will be short-lived, with annual inflation approaching 2% by the end of next year. This will provide the RBNZ with scope to lower the OCR and provide economic support to an economy trying to find its mojo,” says Smith.

ASB expects a 25 basis-point cut at the 26 November Monetary Policy Statement, taking the OCR to 2.25%, and perhaps even lower next year:

"Provided inflation expectations remain anchored around the inflation target midpoint, the RBNZ would be well placed to push the OCR lower still in 2026 if there is the need to kick-start the sluggish NZ economy.”

The downward drive in Kiwi interest rates looks set to exert further pressure on the currency.