Image © Adobe Images

The pound-to-New Zealand dollar rate could retrace some recent gains, but NZD headwinds remain significant.

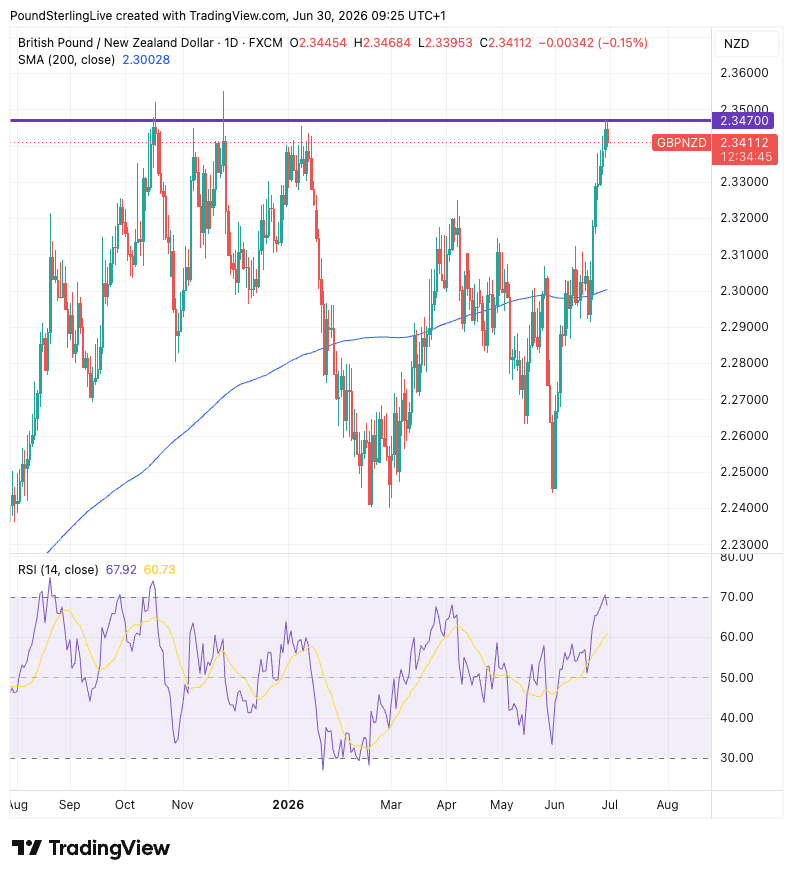

We reported last week that the GBP/NZD was undergoing a decisive breakout that shifts the technical outlook firmly in sterling’s favour.

That call was correct and the pair extended its rally, and although the setup is still constructive, the presence of a significant resistance layer combines with overbought conditions to hint that scope for a pullback is building.

The coming week could see those frictions start to play on GBP/NZD's progress and a retreat to 2.3200-2.3250 is possible as that's where the first area where buyers should emerge.

The balance of probabilities remains tilted in favour of sterling after GBP/NZD’s powerful June rally, but the pair is now testing a significant resistance zone that could slow the advance.

A sustained break above 2.3470 would complete a major bullish breakout and open the way towards 2.36 and potentially higher.

If resistance holds initially, expect consolidation or a modest pullback towards 2.32-2.33, where the technical picture suggests buyers are likely to re-emerge before another attempt higher.

Why NZD is Struggling

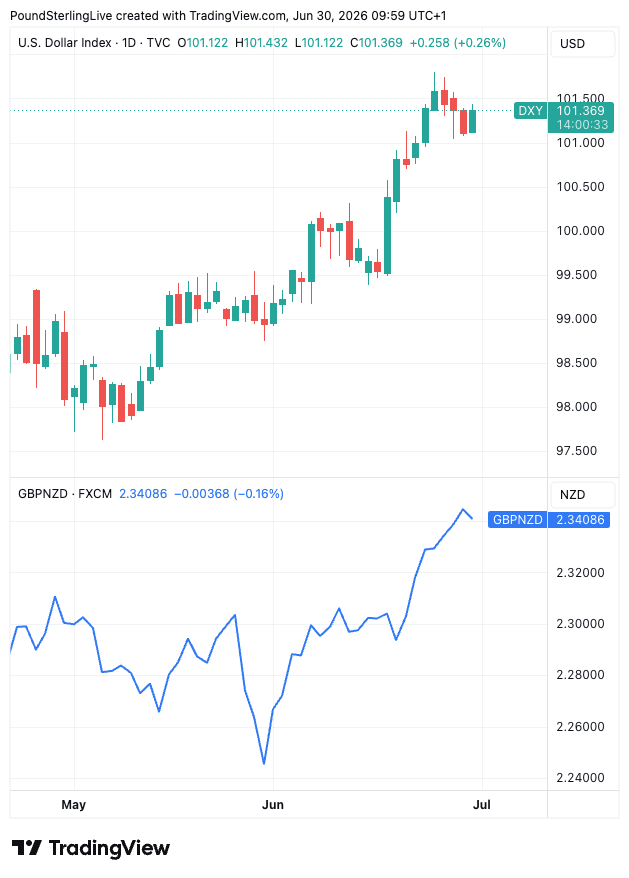

The New Zealand dollar has been penalised by the rise in the U.S. dollar, and we suspect the belief that New Zealand rate hikes are too generously priced.

The New Zealand dollar is one of the world’s classic high-beta currencies, it tends to outperform when investors are optimistic, global growth expectations are improving and financial conditions are loose.

It also tends to underperform disproportionately when those conditions reverse.

Above: The dollar index (top) looks to be leading the GBP/NZD.

June's dollar rally created precisely that headwind: as markets repriced the outlook for the Federal Reserve towards higher-for-longer interest rates, U.S. Treasury yields rose and the dollar strengthened.

Higher U.S. rates tighten global financial conditions by increasing the return available on dollar assets and raising the cost of capital worldwide. Investors respond by reducing exposure to riskier, growth-sensitive assets, including high-beta currencies such as the New Zealand dollar.

The NZD is especially vulnerable because New Zealand is a small, open economy whose currency is closely tied to global risk appetite, commodity demand and international capital flows. When the Fed turns more hawkish and the dollar rallies, investors typically rotate out of currencies like the kiwi and back into the relative safety and higher yields of the U.S. dollar.

Good News on Jobs

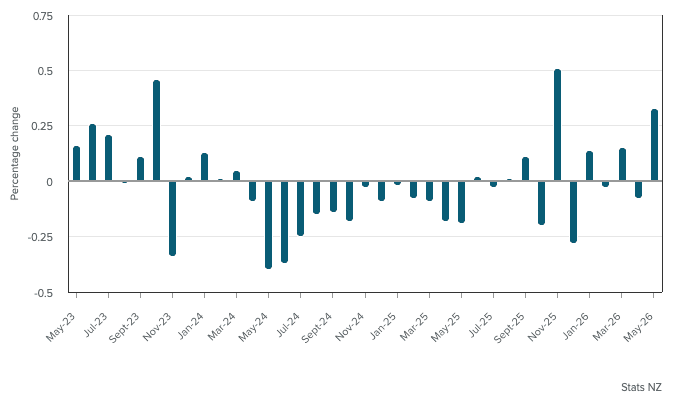

Global forces are clearly in charge; if they weren't, we might have seen a positive currency reaction to New Zealand's latest jobs report.

StatsNZ reported its monthly employment indicator saw a 0.3% increase in jobs filled, up from 0.2% previously.

The annual change stands at 0.3% which is much improved on the previous reading -0.1%.

The data should provide the RBNZ with some confidence that the economy is ticking along.

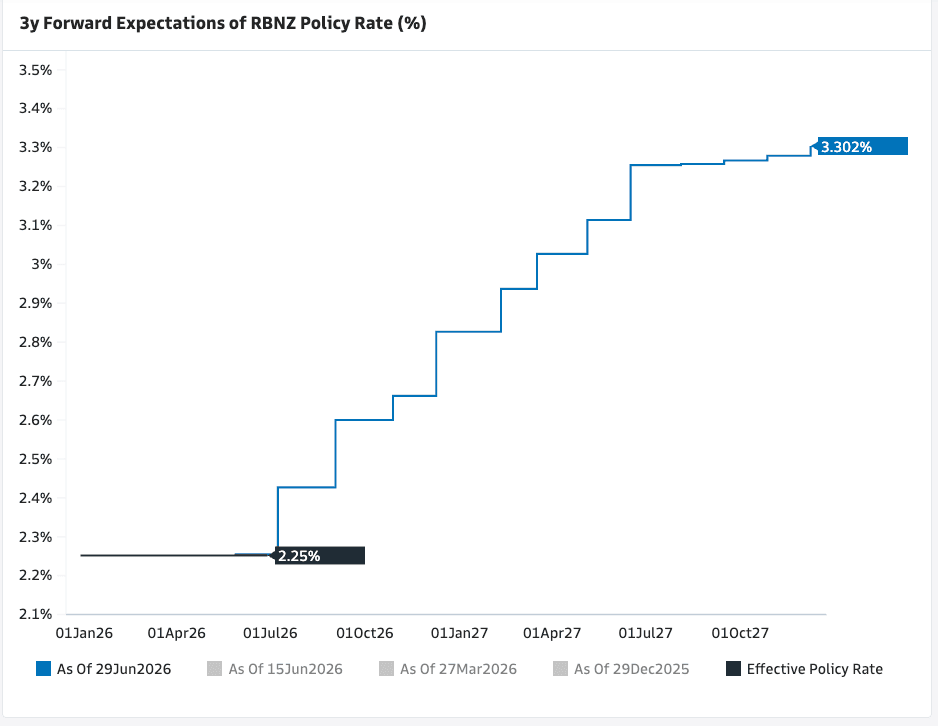

However, RBNZ Rate Hike Bets Look Too Rich

The solid monthly jobs outcome is unlikely to allay suspicions that the market is far too richly priced on the potential for NZ rate hikes.

Currently, the market is priced for two rate hikes from the RBNZ this year; for context, that's more than other G10 central bank, the Fed included.

That should be bullish for NZD as rate hike expectations tend to lead currency outperformance: just look at the AUD's outperformance in H1 as the RBA jacked rates on three occasions.

Above: Market-based expectations for future RBNZ rates.

That the NZD is actually one of the weaker performers tells you that hike expectations are either misplaced or are seen as the 'wrong' type of hikes.

Typically the 'wrong' type of hikes are those that are delivered in stagflationary scenarios; i.e. where inflation is high, but growth is not. If anything, they will tank the economy down the line, which is hardly currency supportive.

An example of a 'good' hike is provided by Australia: the RBA has raised rates three times this year, not in response to the war in the Middle East but in response to a solid domestic economy characterised by strong demand.

Until the NZ economy starts generating solid growth, the NZD will likely struggle.