File image of RBNZ Governor Orr. Image © Pound Sterling Live, Still Courtesy of RBNZ.

Relief is in sight for the New Zealand Dollar, according to one of the world's biggest banks.

A currency market update from JP Morgan says, "further NZD weakness will be harder to come by after RBNZ’s first cut; trim shorts."

The strategic call to "trim shorts" shows JP Morgan thinks the lion's share of weakness related to the August rate cut at the Reserve Bank of New Zealand might have run its course.

Indeed, the Kiwi Dollar has proven resilient in the wake of the cut, helped by a noticeable improvement in global investor sentiment centred on growing expectations that the Federal Reserve is on the cusp of a determined interest rate cutting cycle.

This will have the effect of lowering interest rates in the U.S., boosting investor sentiment. But, lower dollar-linked funding rates will also weigh on interest rates internationally, boosting the global growth cycle which is traditionally supportive of the New Zealand Dollar.

But, JP Morgan thinks the RBNZ's decision to move early on interest rates will also provide NZD with support: the cut could offer the NZD some comfort as the prospect of better economic outturns comes into view now that the pressure of elevated interest rates eases.

"Markets were pricing a lot of easing already, but having started the process, and a bit earlier than expected there is now slightly greater comfort that the economy will stabilise into 2025, allowing

risk premium for a more disorderly downturn to be trimmed to an extent," says Ben K Jarman, an analyst with JP Morgan in Australia.

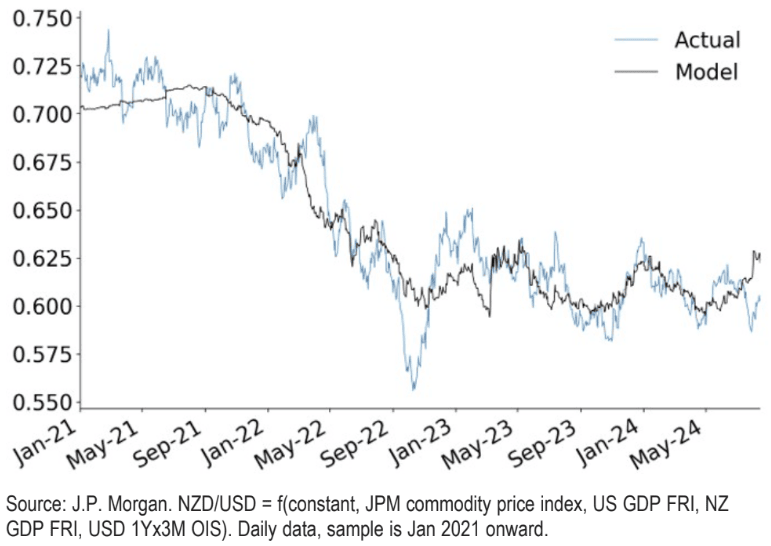

Above: "NZD/USD is starting to look cheap on this cycle’s most reliable drivers (growth and US rates), and lacks local data catalysts near-term to extend the sell-off" - JP Morgan.

"Rates are also not as much of a headwind as one might assume, in that the RBNZ only roughly matched the degree of easing implied in the terminal rate complex. Relatedly, we also see expectations for 50bp moves into 1H25 as somewhat aggressive, and paid these spreads in our Antipodean rates portfolio," he adds.

Put another way; the market might have maxed out its bearishness on the NZ Dollar as any improvement in the economic cycle eases the scale of interest rate cuts required from the RBNZ.

"All said, we think a lot has now been priced into the NZD curve and the RBNZ continues to show quite high Fed sensitivity. NZD/USD is also starting to screen a little cheap relative to this cycle’s most important drivers," says Jarman.