Image © Adobe Stock

Soft quarter-three inflation keeps the door ajar to further Reserve Bank of New Zealand (RBNZ) interest rate cuts and keeps the NZ Dollar on the back foot.

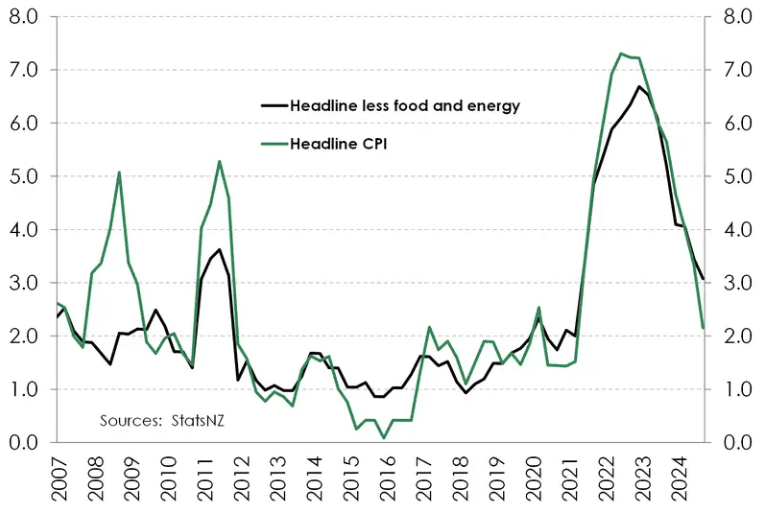

The Pound to New Zealand Dollar exchange rate (GBP/NZD) rallied to a two-and-a-half-month high at 2.1621 after Statistics New Zealand said inflation rose to 0.6% q/q in the third quarter from 0.4% in the second quarter.

Although rising inflation is often associated with currency strength, the number was below the consensus estimate of 0.7%.

New Zealand's preference for quarterly releases can mask the pace of change underway, which was underlined by the drop from 3.3% to 2.2% in the year-on-year figure.

This puts inflation comfortably where the RBNZ wants it, allowing it to focus on other matters, most pressingly the moribund economy that could do with a shot of stimulus that lower interest rates offer.

"The RBNZ can declare victory in the war on inflation," says Jarrod Kerr, Chief Economist at Kiwibank. "There is more disinflationary pressure in the pipeline as the economy continues to operate below its productive capacity."

The NZD's decline tells us that the market agrees that a steady flow of RBNZ rate cuts is incoming.

Image courtesy of Kiwibank.

The NZD has benefited from the highest central bank policy rate in the G10 currency complex, but 75 basis points of cuts in 2024 means the Bank of England now commands the highest base rate at 5.0%.

A loss of support from the interest rate channel and fading excitement from China's economic stimulus measures can keep the Kiwi under pressure.

Economists at Auckland Savings Bank think annual CPI inflation will hover around 2% in future, potentially falling below 2%, within the next 12 months.

"We expect a 50bp cut in November (4.25%), and a 3.25% OCR endpoint, but risks are tilted to more front-loaded policy easing," says Mark Smith, Senior Economist at ASB.

Breaking it Down

The headline decline was driven by the fall in oil prices, which helped cheapen the cost of motoring (transportation prices -2.1% q/q, snipping 0.3ppts off the headline Q3 CPI) rate.

Petrol: -6.5% q/q in Q3, diesel -8.7% q/q).

Vehicles prices: -1.7%.

Education: -7.6% in Q3 as the Family Boost support package contributed to a sharp 22.8% Q3 fall for early childhood education.

Housing: +1.9% q/q in Q3, taking annual inflation to 4.6%. (Local authority charges were up 11.9%).

Rents: +0.9% q/q in Q3, 4.5% y/y.