Image © Adobe Images

The Pound remains a 'buy on dips' against the New Zealand Dollar.

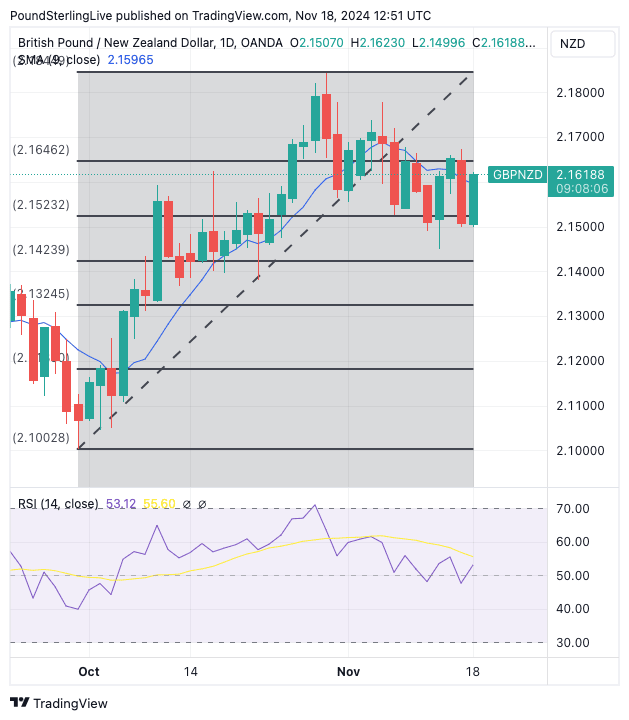

The Pound to New Zealand Dollar exchange rate (GBP/NZD) starts the new week with a solid bid, going to 2.1622 as it looks to reverse the previous Friday's selloff.

Early NZD weakness comes after the October BuisinessNZ Composite PMI came in at 46.2 in November, down from 46.4, confirming the growth outlook in New Zealand remains very weak.

"The country is likely to re-enter a recession when Q3 GDP is released on December 18th. This should keep the RBNZ easing in large steps as we expect 50 bps in November and potentially again in February," says Noah Buffam, an analyst at CIBC Capital Markets.

Buying interest in GBP/NZD is consistently found on any falls to the 2.1523 area, which marks the 38.2% Fibonacci retracement of the October rally.

The chart below shows this area of support, and the Week Ahead Forecast says that this area represents a near-term floor.

However, the chart also shows that buying interest soon fades at 2.1646, another Fibonacci line, the 23.6% retracement.

This leaves us with an exchange rate that is respecting an unusually tight range in the near-term.

But zoom out a bit, and we note that GBP/NZD remains in a long-term rally. This means we view the November sideways trading pattern as a consolidation of this trend.

In short, the coming days can see further trade between the aforementioned barriers, but ultimately, the next directional move can be to the topside.

So, what could trigger a breakout?

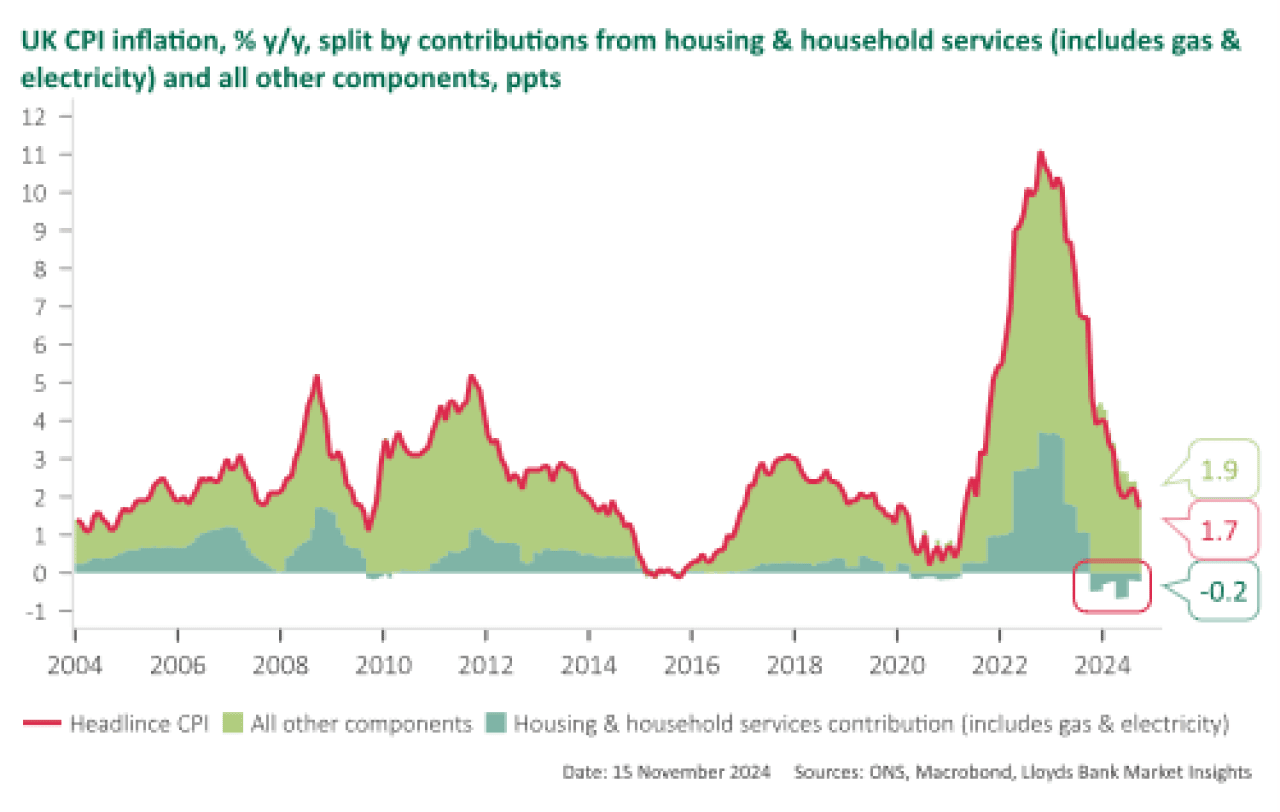

There are a couple of points of interest in the UK this week, with inflation figures due on Wednesday and the November PMI survey due on Friday.

Regarding event risk, UK inflation data is due for release on Wednesday.

UK inflation is expected to have risen to 2.2% year-on-year in October from 1.7% in September, indicating an acceleration in inflation.

Economists at the Bank of England and the Office for Budget Responsibility recently upgraded their forecasts for the near term. This follows the October budget, which saw the government announce a major increase in spending.

Also, household energy prices are rising again, so the easy part of the 2024 deflationary process is now behind us.

Core inflation is expected to remain at a sticky 3.2%, driven by strong services inflation. If these figures come in weaker, the pound could come under pressure, as this would open the door to a potential Bank of England interest rate cut in December.

"The services rate is set to remain hovering close to 5% y/y. A significant downside surprise would be needed to meaningfully boost the likelihood of a December rate cut," says Sam Hill, Head of Market Insights at Lloyds Bank.

Should inflation beat expectations, the Pound-Australian Dollar exchange rate could well rally back to its recent highs as investors reinforce expectations that the Bank of England will only be able to cut at a quarterly pace in 2025, meaning just four further rate cuts are likely.

We are particularly interested in the UK's PMI data, due on Friday, as they should incorporate the fallout from the October budget.

There are reports that business sentiment and hiring intentions took a hit following the budget, and this could be reflected in a poor PMI reading. If this is the case, GBP/NZD could close the week in the red.

"In the two weeks since the budget, various big names in the UK retail and hospitality sector have warned that Reeve’s hike to employers’ national insurance contributions would led to a jump of costs to consumers. Others have indicated that it could lead to job losses," says Jane Foley, Senior FX Strategist at Rabobank.

The Bank of England could well respond to signs of a slowing economy by cutting interest rates again next month, judging that it can cut rates further without stoking inflation. It would suggest that the Bank thinks that if growth is allowed to collapse, then inflation would drastically undershoot current expectations in 2025-2026.

Any signs that it will accelerate the rate cutting process would weigh on the Pound.