Image © Adobe Images

The Pound-to-New Zealand Dollar exchange rate (GBPNZD) is forecast to push higher in a week that will see the Reserve Bank of New Zealand (RBNZ) cut interest rates and the UK deliver inflation data.

Of course, there are risks to this view, but we see GBPNZD as engaged in a phase of consolidation that follows 2024's stellar rally, and at some point, that rally can restart.

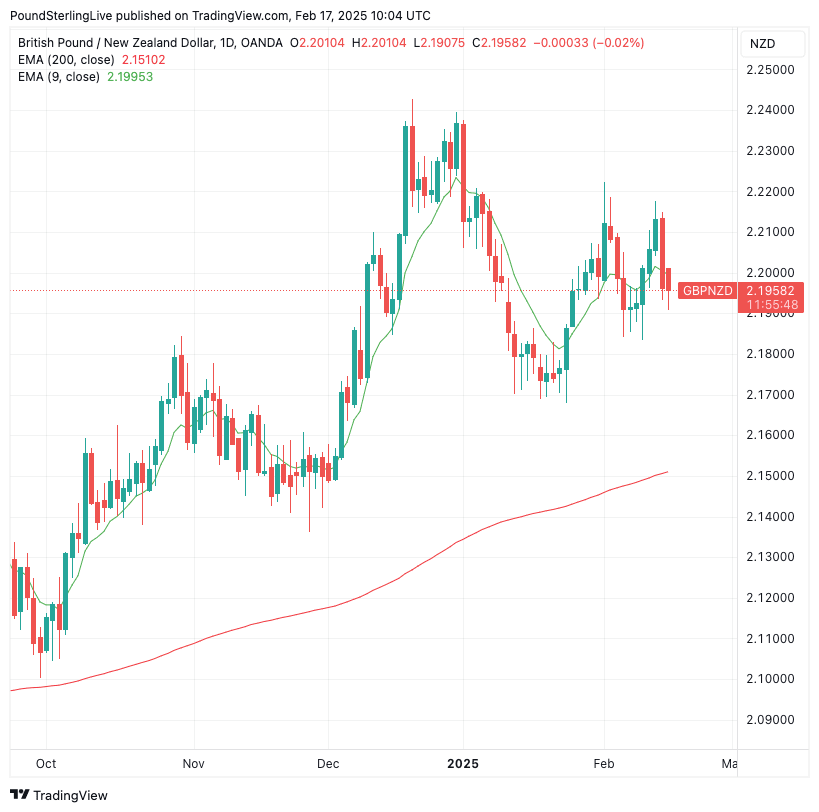

Above: GBPNZD remains in an uptrend. Only a break below the 200-day MA (red line) would turn the market into a downtrend.

A pullback that occurred in January ultimately established support at levels around 2.20, from which a recovery towards the 2024 high at 2.24 can evolve.

However, that's a multi-week story, and we see two-way risks heading into the RBNZ decision due on Wednesday.

Dips on a 'hawkish' RBNZ cut - i.e. one that hints the central bank can afford to pause the cutting cycle - should find buying interest at 2.1836, which represents the previous week's low and illustrates there is decent demand at these levels.

That being said, our Week Ahead Forecast model prefers to anticipate gains to 2.22.

The RBNZ is expected to deliver a third consecutive 50 basis point (bp) cut in its upcoming meeting based on Governor Adrian Orr’s clear signalling in previous statements, which have been unusually explicit for the need to be forceful amidst worsening economic conditions.

The labour market dropped 32,000 jobs in 2024 and inflation is declining, as are inflation expectations, which suggests the decline is durable.

Economists at Kiwibank say that the RBNZ should be even more aggressive and bring the Official Cash Rate (OCR) down to 3% immediately instead of following its current slow-paced trajectory.

Kiwibank explains that the RBNZ's forecast of cutting to 3.5% and then waiting two years before cutting to 3% is inefficient. It suggests the central bank should move decisively rather than "mucking around."

A lower OCR would help economic recovery faster, potentially positioning the RBNZ for future rate hikes in a more stable economy.

The risk of delay is greater than the risk of cutting too much, given that inflation expectations are already anchored at the RBNZ’s 2% target.

The 50bps cut is already priced in, so the immediate downside for NZD is limited, meaning the currency is expected to be more influenced by RBNZ guidance than the rate cut itself.

Attention will be on the RBNZ’s updated OCR track, which, if lowered further, will confirm expectations for deeper easing and may relieve bond markets and weigh on NZD.

More broadly, external factors like U.S. tariffs and global risk sentiment will continue to influence the Kiwi dollar.

Of late, we have seen the impact of President Donald Trump's tariff threats decline, meaning a potential downside risk to NZD is fading.

Also, keep an eye on progress on a Ukraine war peace deal. If a credible plan is agreed, then risk-associated assets like NZD can recover further.

It's also a busy week for the GBP side of the GBPNZD equation:

Week Ahead: GBP

Tuesday, February 18

? Average Weekly Earnings (Dec, YoY)

Inc. Bonuses: 5.9% (expected) vs. 5.6% (previous)

Ex. Bonuses: 5.9% (expected) vs. 5.6% (previous)

? Market Impact: A higher-than-expected figure could reinforce inflationary wage pressures, possibly influencing the Bank of England’s (BoE) policy stance.

? ILO Unemployment Rate (Dec)

Expected: 4.5%

Previous: 4.4%

? Market Impact: If unemployment rises, it could signal labor market softening, potentially weakening GBP.

? Employment Change (Dec, 3m/3m)

Expected: 50K

Previous: 35K

? Market Impact: A strong reading indicates resilient hiring trends, supporting growth and possibly keeping wage growth elevated, which is inflationary. This would underpin the Pound.

? BoE Governor Andrew Bailey Speaks

? Market Impact: If Bailey delivers hawkish remarks, GBP may strengthen as markets price in fewer rate cuts in 2025. A dovish tone could weigh on GBP.

Wednesday, February 19

? Consumer Price Index (CPI) (Jan, YoY & MoM)

MoM Expectation: -0.3% vs. -0.2% (previous)

YoY Expectation: 2.8% vs. 2.8% (previous)

Core CPI (YoY): 3.7% vs. 3.2% (previous)

? Market Impact: A slowdown in inflation would increase the probability of BoE rate cuts later in 2025, weighing on GBP. A stronger print could delay rate cuts and give GBPNZD a boost.

? CBI Industrial Trends Orders (Feb)

Expected: -30

Previous: -34

? Market Impact: A higher-than-expected figure suggests improving UK manufacturing sentiment, but the sector remains weak overall. This doesn't tend to be a big mover for GBP.

Friday, February 21

? GfK Consumer Confidence (Feb)

Expected: -24

Previous: -22

? Market Impact: A lower confidence reading reflects weaker consumer sentiment, possibly dampening future spending and economic growth.

? Retail Sales (Jan, MoM & YoY)

Inc. Automotive Fuel (MoM): 0.5% (expected) vs. -0.3% (previous)

Ex. Automotive Fuel (MoM): 0.9% (expected) vs. -0.6% (previous)

? Market Impact: A rebound in retail sales could support GDP growth and indicate stronger consumer spending, boosting GBP.

? Public Sector Net Borrowing (Jan)

Expected: -£20.3bn

Previous: £17.8bn

? Market Impact: Lower borrowing could ease fiscal pressures, but higher-than-expected borrowing might increase concerns over government debt levels.

? UK Services PMI (Feb, Preliminary)

Expected: 51.0

Previous: 50.8

? Market Impact: A reading above 50 signals expansion, which may support UK economic optimis and boos the Pound.

? UK Manufacturing PMI (Feb, Preliminary)

Expected: 48.5

Previous: 48.3

? Market Impact: Still in contraction (<50), but a slight improvement could signal bottoming out of the UK manufacturing sector.