Image © Adobe Images

The Pound should see further consolidation against the New Zealand Dollar this week, with risks staying to the upside.

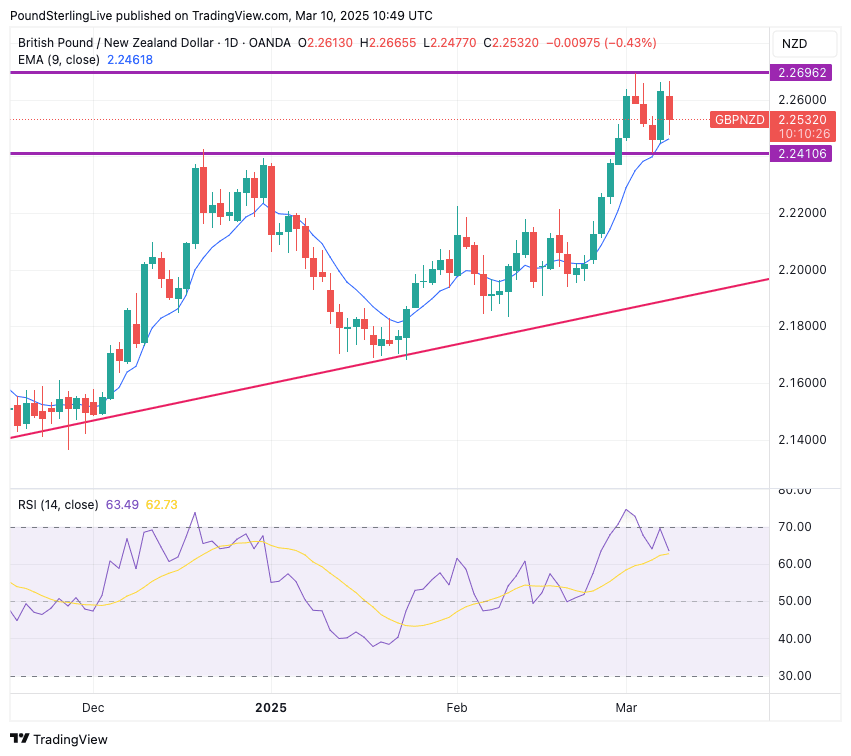

The Pound-to-New Zealand Dollar exchange rate (GBPNZD) is in a long running uptrend, but the coming days should see that uptrend paused, with the potential for further weakness.

This is understandable behaviour, as the final week of February saw the exchange rate tear higher and become significantly overbought.

We said in last week's Week Ahead Forecast that a consolidation was in order to allow overbought conditions to unwind.

This has played out, and the Relative Strength Index (RSI) on the daily chart has unwound as consolidation takes place:

Above: GBP/NZD at daily intervals, showing scope for consolidation.

The outlines of that consolidative zone form the boundaries of the levels we anticipate in the coming days: 2.2696 at the top and 2.2410 at the bottom.

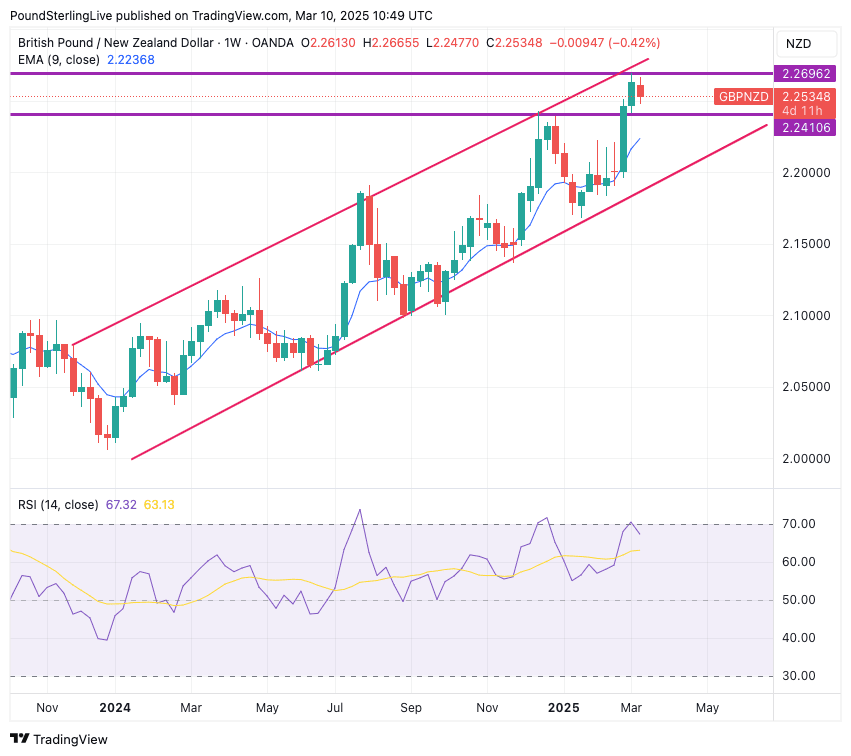

Although consolidation is likely, the direction of travel remains higher, with the weekly chart showing a clear uptrend channel remains intact:

Above: GBP/NZD at weekly intervals, confirming a long-running uptrend is still intact.

Based on this, weakness will tend to be shallow and the broader trend higher.

Global sentiment is proving a major obstacle to NZ Dollar strength at present.

The New Zealand Dollar's trade against the British Pound strongly correlates with the performance of U.S. stock markets, which shouldn't be surprising, as indices such as the S&P 500 are a proxy for global investor sentiment.

The New Zealand Dollar is highly leveraged to broader sentiment, meaning it tends to come under pressure when equities are falling, as has been the case recently:

The above shows that the NZD has fallen against GBP as the S&P 500 comes under pressure.

If the U.S. market continues to struggle, so too will NZD. However, any rebound from here can shore up the Kiwi.

An interesting development in 2025 has been the ending of the U.S. exceptionalism theme, with the U.S. economy and stock markets no longer seen as runaway outliers as investors grapple with Donald Trump's volatile approach to policy making.

"Tariff on / tariff off" is a new trade that is emerging, which explains how investors respond to the daily barrage of contradictory and low-conviction tariff calls coming from the White House.

Economists are meanwhile predicting a slowdown in the economy, which Donald Trump himself admitted was likely in a recent interview.

"Investors are clearly questioning whether the US economy is being steered by a sound financial strategy or by impulsive political manoeuvring. Markets thrive on stability and predictability—two qualities that are in short supply under an erratic approach to global trade," says Dr. Claudio Wewel FX Strategist at J. Safra Sarasin.

New Zealand Week Ahead

The multi-year uptrend in GBP/NZD also has a lot to do with New Zealand's economic underperformance of recent years, which has allowed the Reserve Bank of New Zealand to slash interest rates.

However, there is a suspicion that more cuts will be needed to help the economy, which undermines the persistent bearishness on the currency.

Although there are no tier-one releases due this week, there should, nevertheless, still be some interest from the data calendar.

Based on the Westpac Weekly Report (March 10, 2025), here are the key economic events scheduled for New Zealand next week, along with market expectations and potential implications for NZD:

Wednesday, March 12

? Retail Card Spending (Feb, MoM)

Previous: -1.6%

? Market Impact:

A stronger-than-expected rise in spending could signal consumer resilience, supporting NZD. If spending remains weak, it may reinforce slower domestic demand, increasing pressure for RBNZ rate cuts, weakening NZD.

Thursday, March 13

? Selected Price Indices (Feb, Monthly Update from Stats NZ)

Previous: Higher-than-expected food price increases

? Market Impact:

If price pressures persist, it could indicate sticky inflation, delaying RBNZ rate cuts and supporting NZD.

If inflation slows, markets may increase expectations for RBNZ rate cuts, pressuring NZD.

? BusinessNZ Manufacturing PMI (Feb)

Previous: 51.4

? Market Impact:

If PMI remains above 50, it signals expansion, which could support NZD.

A drop below 50 indicates contraction, raising concerns about economic slowdown, potentially weakening NZD.

? Food Price Index (Feb, MoM)

Previous: +1.9%

? Market Impact:

A sharp decline in food prices could reduce inflation pressures, increasing rate cut speculation, weakening NZD.

Stronger-than-expected food price inflation may delay RBNZ easing, supporting NZD.

? Housing Rents (Feb, MoM)

Previous: +0.1%

? Market Impact:

Rising rents indicate ongoing inflationary pressures, potentially delaying RBNZ cuts, supporting NZD. Flat or declining rents suggest disinflation, reinforcing rate cut bets, weakening NZD.

Britain's Week Ahead

Friday's UK Monthly GDP report will be the data highlight of the coming week.

"As the first month of the quarter and year, January’s GDP outturn will play a big part in setting the tone for growth expectations for both Q1 and the whole of 2025. We expect January GDP to rise by 0.1% m/m," says Hann-Ju Ho, Senior Economist at Lloyds Bank.

If GDP beats expectations, the pound will rise into the weekend, as this would confirm that fears of a material slowdown are exaggerated, taking pressure off the Bank of England to cut interest rates.