Image © Adobe Images

The Pound is struggling to reassert itself over the New Zealand Dollar.

The Kiwi currency has found itself well supported amidst a global sigh of relief that U.S. Donald Trump has stepped back from his aggressive tariff agenda and is showing a strong desire to negotiate down the headline tariff rates.

Last week's news that China was ready to start talking about talks to lower tariffs proved particularly supportive of the antipodean currencies that often trade as a proxy for Chinese sentiment.

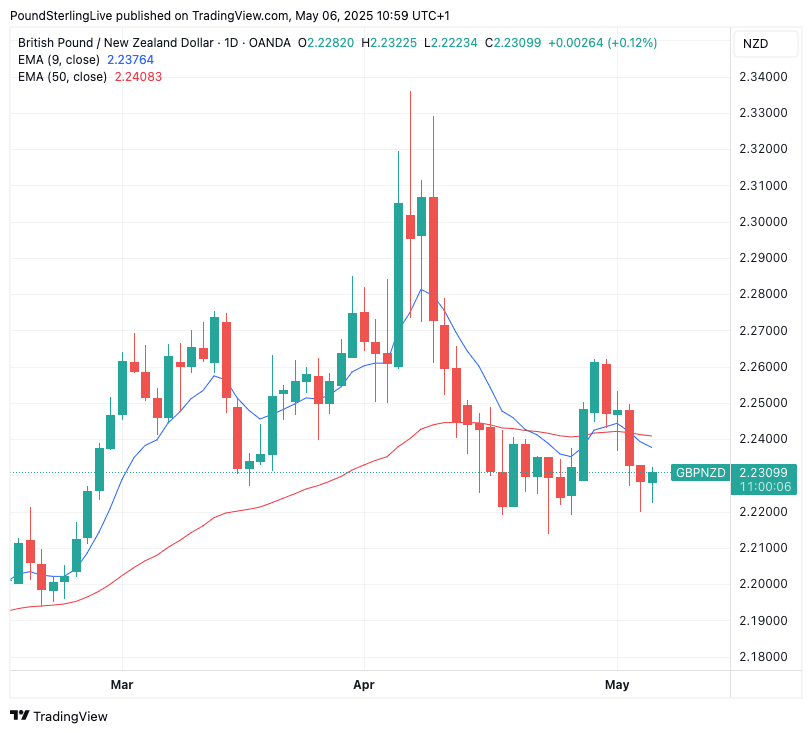

The Pound to New Zealand Dollar exchange rate (GBP/NZD) reflects these developments with a steady decline from multi-year peaks at 2.33 (April 07) to a current spot rate of 2.23.

Last Friday saw a sharp 0.68% drop that followed on from a better-than-expected U.S. jobs report that suggested the U.S. economy is proving particularly robust in the face of Trump's tariff antics. This proved supportive for U.S. stocks and investor sentiment, which naturally benefited the Kiwi Dollar.

Also helping were comments from Chinese authorities that it would consider negotiating with the U.S. to lower tariffs. "With China being New Zealand's main trading partner and Trump recently offering a bit of an olive branch, we see a glimmer of hope that the two economic powerhouses are on a de-escalation path," says Wayne Gordon, Strategist, UBS AG.

NZD strength saw GBP/NZD slide through the 50-day exponential moving average (EMA), which signals a near-term deterioration in momentum that advocates for further weakness.

Above: GBP/NZD at daily intervals.

Our Week Ahead Forecast sees the prospect of a retest of 2.22 ahead of a breakdown to 2.20, which marks an approximation of support levels from February.

Near-term (the coming hours and two days) the prospect of some buying interest is seen that can allow the GBP/NZD to make contact with a descending nine-day EMA. However, for now, strength will prove limited.

Bigger picture, it is still too soon to call an end to the multi-year rally in GBP/NZD and what we could be seeing is a pullback of that trend and a broader consolidative move that eventually gives way to a retest of the 2025 peak at 2.33.

So although near-term weakness is on the cards, at some point in the coming months the uptrend should reassert.

Trade in the coming week will likely rest with the global pulse and how the U.S. and China move towards trade talks. Ultimately, they will, but both sides could frustrate the process if they adopt combative stances to reinforce their positions.

Markets will be watching the midweek Federal Reserve interest rate decision for guidance, as any hint at imminent interest rate cuts would boost stocks and provide the New Zealand Dollar with fresh impetus.

The Fed has reason to deliver some insurance interest rate cuts in the face of tariffs that Chair Jerome Powell recently acknowledged as being more severe than he had envisioned.

However, the official data does not yet reflect tariff uncertainty and fears of a sharp slowdown in imports, meaning the Fed has little concrete data on which to act.

This should ensure the meeting is a wait-and-see one, which should allow the recent depreciation trend in GBP/NZD to extend.