Image © Adobe Images

The Dollar is outperforming on evidence of building price pressures.

Fears that tariffs are starting to show up more forcefully in U.S. inflation monitors were stoked Thursday by an above-consensus set of Producer Price Index numbers.

Heading PPI inflation rose 0.9% month-on-month in July, having been flat in June, handily exceeding predictions for 0.2%.

Year-on-year, the figure moves to 3.3% in July from 2.4% previously and ahead of consensus expectations of 2.5%. The core measure was equally uncomfortable at 3.7% (previous: 2.6% and consensus: 2.9%).

"Price pressures are building," says Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics. "New tariffs are continuing to generate cost pressures in the supply chain, which consumers will shoulder soon."

"Potential evidence of tariff effects is the key question on investors’ minds, and the notable challenge is predicting how much more tariff impact is likely in the coming months. Our economists are anticipating a notable impact to come, given the nature of frontloading seen in trade during H1," says Clyde Wardle, Senior EM FX Strategist at HSBC.

The data weighed on stock markets and other risk-aligned financial assets, although the Dollar proved to be a winner, as it is now outperforming all G10 peers on the day.

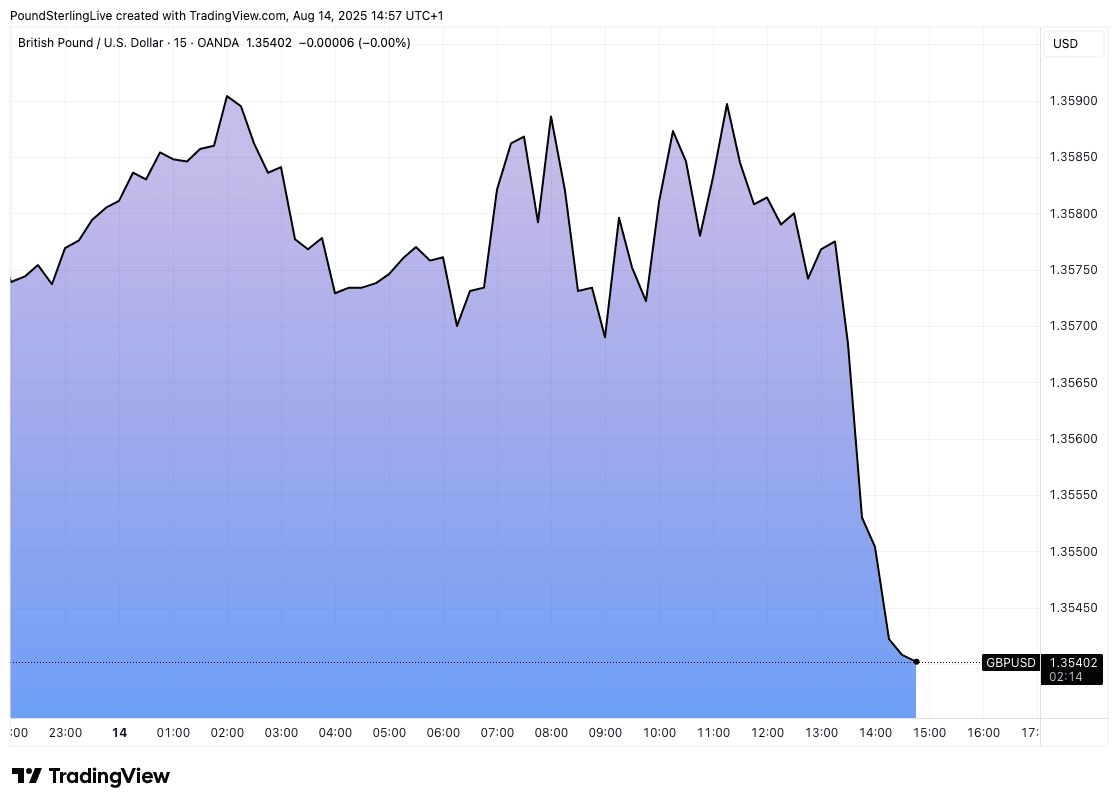

The Pound to Dollar conversion dropped 1.3539 in the minutes following the release, although weakness here is contained by the broader rise in Sterling that follows this morning's domestic GDP release that exceeded estimates.

Dollar strength is more apparent on the crosses, for instance Euro-Dollar is lower by 0.44% on the day at 1.1652.

Above: GBP/USD at 15-minute intervals.

Producer prices are seen as being a leading indicator to the more familiar headline CPI inflation that consumers are exposed to as manufacturers will attempt to pass on their own rising costs.

The impact of import tariffs has been cushioned to a degree by the staggered implementation as well as margin-absorption by exporters and manufacturers. But this cushion is not anticipated to last forever.

For example, economists at Crédit Agricole say on Thursday the price rises should be spread out over the remainder of 2025 and 2026, with the main price thrust coming in H2.

For markets, this makes for nervous times, as any above-consensus inflation readings could cool Federal Reserve enthusiasm for lower interest rates. A September rate cut is fully expected, as is a follow-up cut before year-end.

A reduction in rate cut expectations would potentially underpin the Dollar, which is why were are seeing the currency appreciate in response to Thursday's PPI print.

The PPI figures and market reaction are the opposite of what we saw Tuesday when CPI inflation figures were released. Here, an undershoot in expectations lead investors to think maybe the U.S. would get away with President Donald Trump's tariff assault.

Stocks rose and the Dollar fell after the U.S. reported a headline CPI inflation rate of 2.7% year-on-year in July, unchanged on June and below the 2.8% consensus expectation.

This after the monthly increase from June to July increased 0.2%, undershooting expectations for 0.3% m/m.

"The pass through from tariffs to CPI has turned out to be even weaker than what we expected," says Jean-François Perrin, Senior Inflation Strategist at Crédit Agricole. "That said, many of these mitigation strategies (margin reduction, high inventories) should not last forever, and tariffs still look set to bite this year and next."