Image © Giuseppe Milo, CC BY 2.0. Source.

Pound–to-dollar week-ahead forecast: looking for a directional break.

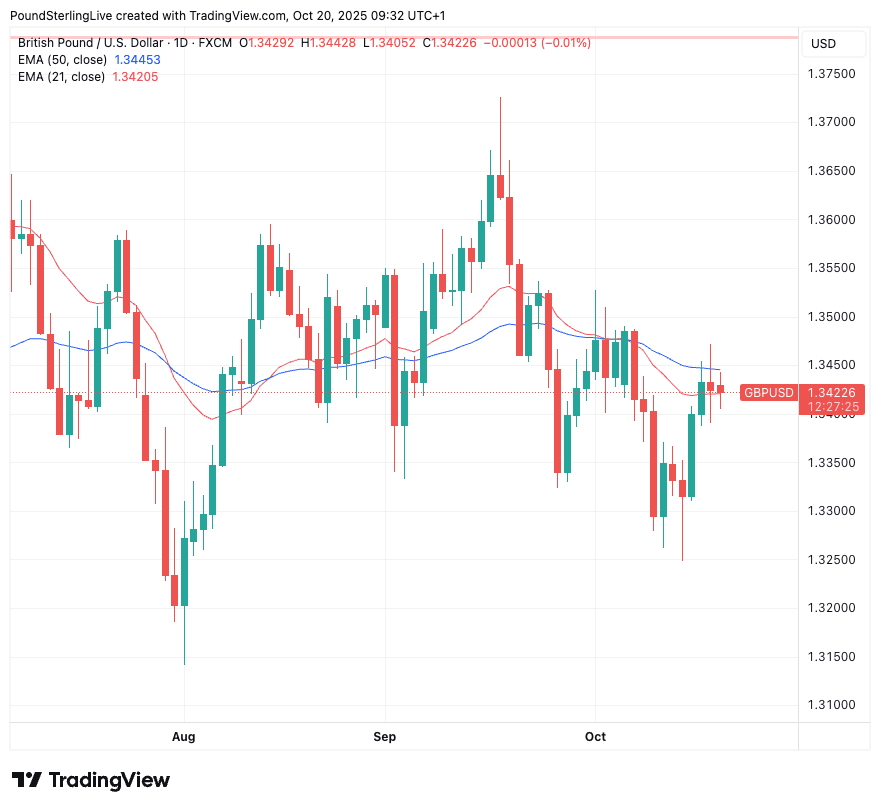

Pound sterling enters the new week trading near 1.3421 against the dollar, trapped beneath its 50-day exponential moving average at 1.3445, a technical ceiling it has failed to close above since September 23.

The longer-term trend signal remains neutral as the 50-day EMA is flat and moving sideways, suggesting the broader market is waiting for a catalyst rather than trending decisively.

Shorter-term gauges, however, offer a subtle positive undertone: the spot exchange rate has crossed above the 21-day and 9-day EMAs, reflecting modest upward momentum that could see GBP/USD probe the 1.3445–1.3480 resistance zone early in the week if sentiment holds.

This fine balance in the chart mirrors a conflicting macro backdrop:

On the one hand, the U.S. government shutdown, now entering another week, adds downside risk to U.S. growth and may begin to erode dollar support if it drags on.

On the other hand, easing trade tensions between Washington and Beijing, with hopes of a Trump-Xi meeting later in the month, offers a stabilising influence on global risk appetite, which is typically dollar-supportive.

The result is a market reluctant to commit either way. The pound’s modest near-term bias higher is countered by a lack of confirmation from the broader trend, keeping traders focused on whether 1.3445 can be reclaimed on a daily close.

A sustained break above there would open scope toward 1.3500–1.3550, while failure and a retreat through 1.3380–1.3350 would reassert range-bound consolidation.

Momentum traders may therefore prefer to fade extremes rather than chase breakouts, buying dips near 1.3350 and trimming longs into 1.3500 until a clear directional catalyst emerges.

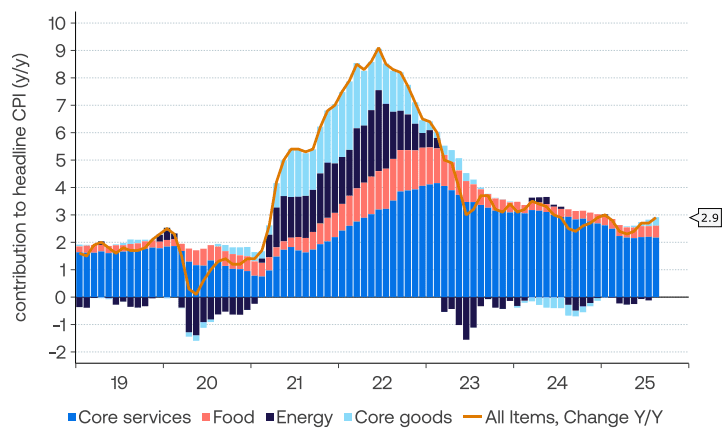

Data-wise, the pair's path will hinge on the release of delayed U.S. CPI inflation figures on Friday.

Above: U.S. inflation and its component parts. Image courtesy of ANZ.

Annual core CPI inflation rose for a third consecutive month in August, with the main driver once again being the services sector rather than tariffs.

Headline CPI inflation is predicted to have lifted to 3.1% in September from 2.9% in August, and core is seen unchanged at 3.1%.

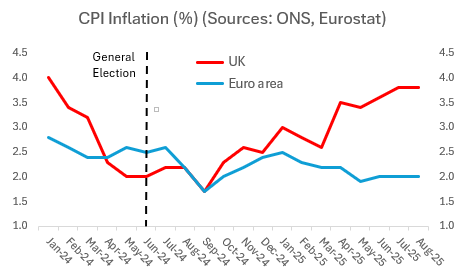

Above: The UK's high inflation relative to comparable economies has not been a boon to the pound in 2025.

The UK's monthly inflation release is also the main calendar event for the British pound this week. Here, a 4.0% reading is expected, putting it at double the Bank of England's target.

The Bank of England will want to cut interest rates at the first given opportunity owing to a deteriorating labour market, and therefore any below-consensus reading will see bets for a December rate cut rise.

This would weigh on the pound.

A reading above 4.0% is, however, unlikely to be positive either. After all, is an economy with high inflation and slowing growth a good bet? Markets will think not: if high inflation was a catalyst for a stronger pound then GBP would straddle the G10's 2025 performance board like a king.

At best, the pound will hope it can muddle along sideways this week, with any up or downside in GBP/USD coming from the USD side of the equation.